$Oracle(ORCL)$ will release its Q1 FY2025 earnings after hours on Monday. Investors are likely to focus on cloud infrastructure growth. According to Visible Alpha, analysts expect the software giant to report revenue of $13.23 billion, up over 6% year-over-year. EPS is expected to be $0.91, compared to $0.86 last year; net income is anticipated to be $2.57 billion.

In June, Oracle announced cloud infrastructure deals with $Microsoft(MSFT)$ , OpenAI, and $Alphabet(GOOG)$ $Alphabet(GOOGL)$ while reporting Q4 earnings, pushing its stock to a record high. Oracle’s stock dipped slightly last Friday but has risen about 35% this year.

Oracle Cloud Infrastructure (OCI) generated $2 billion in revenue last quarter, and the company expects more than 50% year-over-year growth by FY2025. Analysts predict OCI will bring in $2.18 billion this quarter, up 44% year-over-year. Morgan Stanley analysts noted that AI hardware shortages are driving business demand for OCI.

Jefferies analysts said that for Oracle to achieve double-digit revenue growth, it needs to see sustained OCI demand and increased OCI capacity.

Current options market outlook

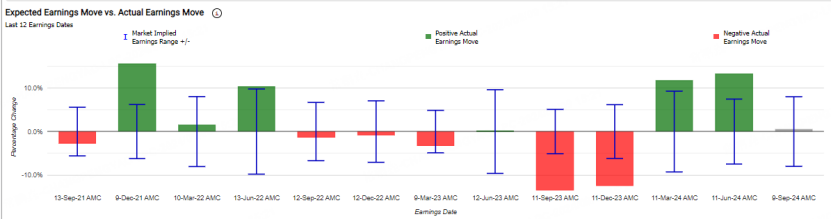

Oracle will report earnings after the close on September 9, 2024. Over the past 12 quarters, the options market has overestimated Oracle’s earnings volatility 50% of the time. The average post-earnings forecast volatility is ±7.1%, while the actual average has been 7.3% (absolute). This suggests Oracle’s stock often moves more than the options market predicts.

In the last six quarters, Oracle’s post-earnings price changes were +3.2%, +0.2%, -13.5%, -12.4%, +11.7%, and +13.3%.

The implied volatility (IV30) before the last earnings report was 36.4. After the report, it dropped to 21.1, a massive 42% decline. Five days after the earnings release, the 30-day implied volatility was 21.1.

The current options market expects a ±8% move post-earnings. Considering this, one might bet on a volatility decline with a short volatility position for Oracle’s earnings.

What is a Strangle Strategy?

In a long strangle strategy, investors buy out-of-the-money call and put options. The call option has a strike price above the current market price of the asset, while the put option has a strike price below it. This strategy has significant profit potential. If the asset price rises, the call option can theoretically go up infinitely, and if it falls, the put option can gain. The risk is limited to the premiums paid for these options.

In a short strangle strategy, investors sell an out-of-the-money call and put option. This is a neutral strategy with limited profit potential. It profits when the underlying stock trades within a narrow range between the breakeven points. The maximum profit is the total premiums received from selling the options minus the transaction costs.

Oracle Short Strangle Example

Oracle is currently trading around $141.80. Here’s how you can set up a short strangle strategy:

Step 1: Sell a call option that expires Sept. 13 with a strike price of $167.50, earning a premium of $67.

1. Maximum Profit

The maximum profit is the total premiums received, which is $82.

If Oracle’s stock price is between $116 and $167.50 on September 13, both options expire worthless, and you keep the entire premium of $82.

2. Maximum Risk

The maximum risk is unlimited because:

- Upside Risk: If Oracle’s stock price is above $167.50 at expiration, the call option will be exercised. You’ll need to sell the stock at $167.50. If the price rises significantly, potential losses can be infinite.

- Downside Risk: If Oracle’s stock price is below $116 at expiration, the put option will be exercised. You’ll need to buy the stock at $116. If the price falls sharply, potential losses can also be infinite.

3. Breakeven Points

- Upside Breakeven Point

When Oracle’s price exceeds $167.50, losses from the sold call option will surpass the premium received.

Upside Breakeven Point = Call Strike Price + Total Premium Received

Upside Breakeven Point = $167.50 + $0.82 = $168.32.

- Downside Breakeven Point

When Oracle’s stock price falls below $116, losses from the sold put option will exceed the total premium received.

Downside Breakeven Point = Put Strike Price - Total Premium Received

Downside Breakeven Point = $116 - $0.82 = $115.18.

Summary

- Maximum Profit: $82 (when Oracle’s price stays between $116 and $167.50).

- Maximum Risk: Unlimited (if the stock price goes above $167.50 or below $116).

Breakeven Points

- Upside Breakeven: $168.32

- Downside Breakeven: $115.18

This strategy is suitable for investors who expect Oracle’s price to stay within the $116 to $167.50 range in the short term. However, it carries unlimited risk, especially if the stock price moves significantly outside this range.

Best for markets where the investor anticipates the stock price will remain within a narrow range but is unsure of the direction. The income comes from selling options premiums, but the potential risk is high, requiring a solid understanding and tolerance for price fluctuations.

Currently, with the stock priced at $141.80 and total premiums received at $82, the return is 0.58%. With four days remaining until expiration, the annualized return is 52.85%. Overall, the short strangle strategy is ideal for traders who expect minimal market movement but are uncertain about the direction.

Comments