After a nearly two-month hiatus, the famous retail trader "Roaring Kitty," aka Keith Gill, made a comeback.

His first post in a while on X was a cryptic image from the 1999 film “Toy Story 2”. The image, altered to show a dog's face on Woody, the cowboy toy, quickly caught the attention of retail investors.

$550,000 in 40 minutes

According to LSEG data, about 18 minutes before Gill’s post, a trader bought roughly 10,000 GameStop call options expiring on September 13 with a strike price of $22.5, totaling about $1.74 million. Shortly after Gill's tweet, two batches of these options (5,000 contracts each) were sold for about $2.29 million.

This mysterious trader made around $550,000 in just a few minutes, netting a 30% profit.

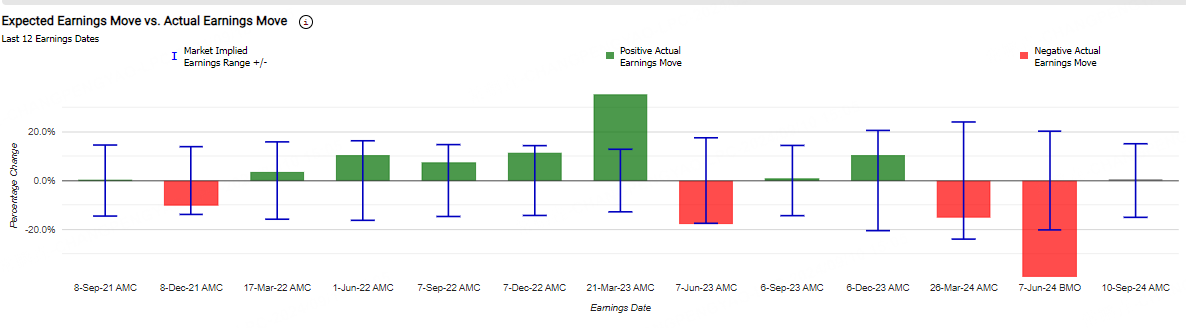

GameStop is set to release its Q2 earnings after the market close on Tuesday. Analysts expect a loss of $0.09 per share on revenue of $895.67 million. Historically, GameStop’s stock has been volatile around earnings reports, and Tuesday’s release could influence the stock’s price and trading volume.

Over the past 12 quarters, the options market has typically overestimated the stock's earnings volatility 75% of the time. The average forecasted volatility post-earnings is ±16.6%, compared to the actual average of 13.5%.

In the last six earnings seasons, GME’s post-earnings stock movements were +35.2%, -17.9%, +0.7%, +10.2%, -15%, and -39.4%.

Ahead of this report, the options market expects a volatility of ±15.1%. Investors might consider a straddle strategy to trade GameStop from a volatility perspective.

What is a Straddle Option?

A straddle is a neutral options strategy that involves buying both a call option and a put option on the same underlying asset, with the same strike price and expiration date.

Traders profit from a long straddle when the asset’s price moves significantly up or down relative to the strike price, enough to cover the total premium paid. The potential for profit is almost limitless as long as the asset experiences high volatility.

On the flip side, a short straddle involves selling both a call and a put option with the same strike price and expiration date. This strategy is used when traders believe the asset will not move significantly in either direction. The maximum profit is the premium received from selling the options, but the potential losses can be unlimited.

Straddle strategies provide valuable insights into the market's expectations. They reveal anticipated volatility and the expected trading range of the stock before expiration.

Typically used before major events like earnings reports, straddles are best suited for highly volatile periods. They are not effective in stable markets, where they tend to underperform.

GameStop Straddle Case Study

In this case, investors are using a strategy called a "Sell Straddle." This involves selling both a call option and a put option with the same strike price and expiration date to collect premiums from both.

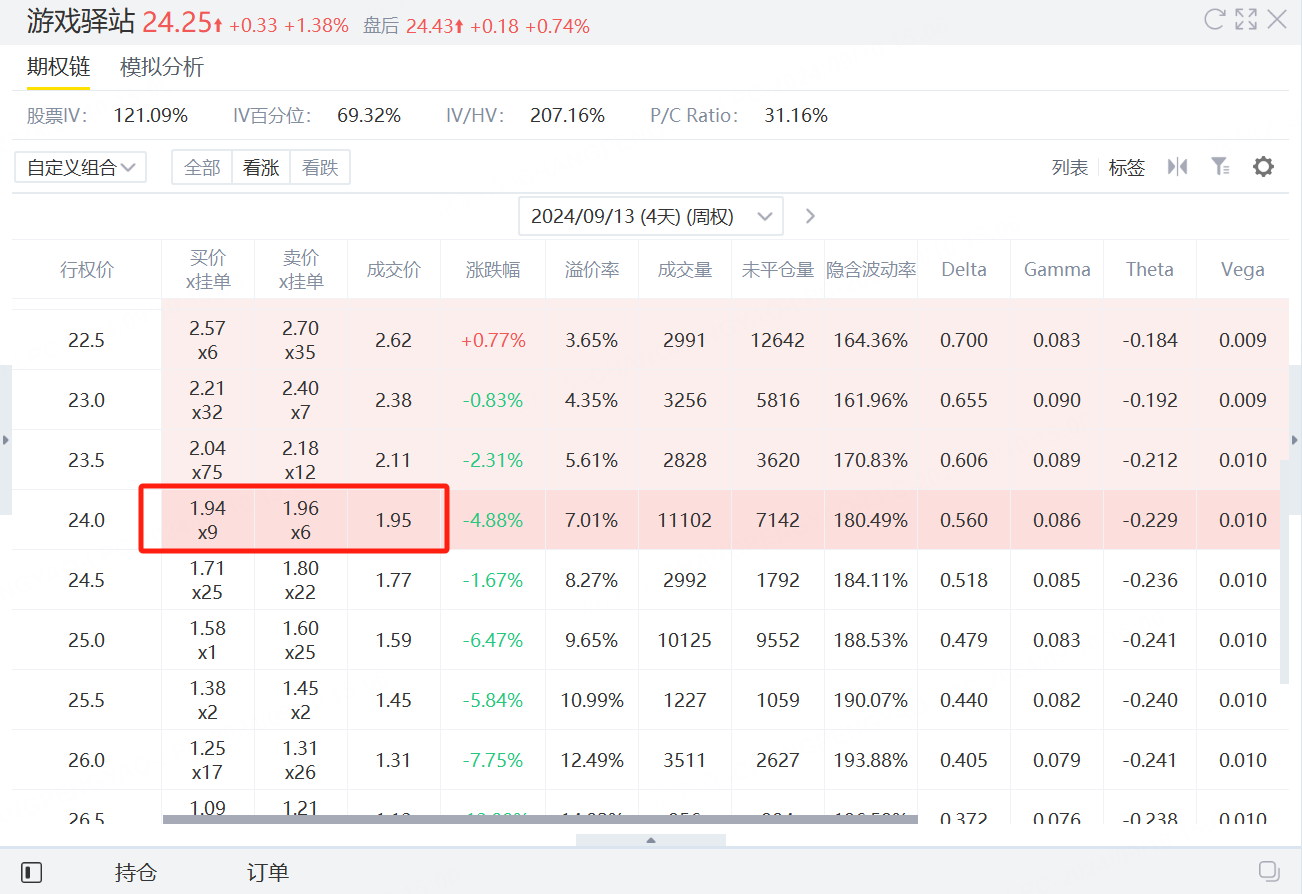

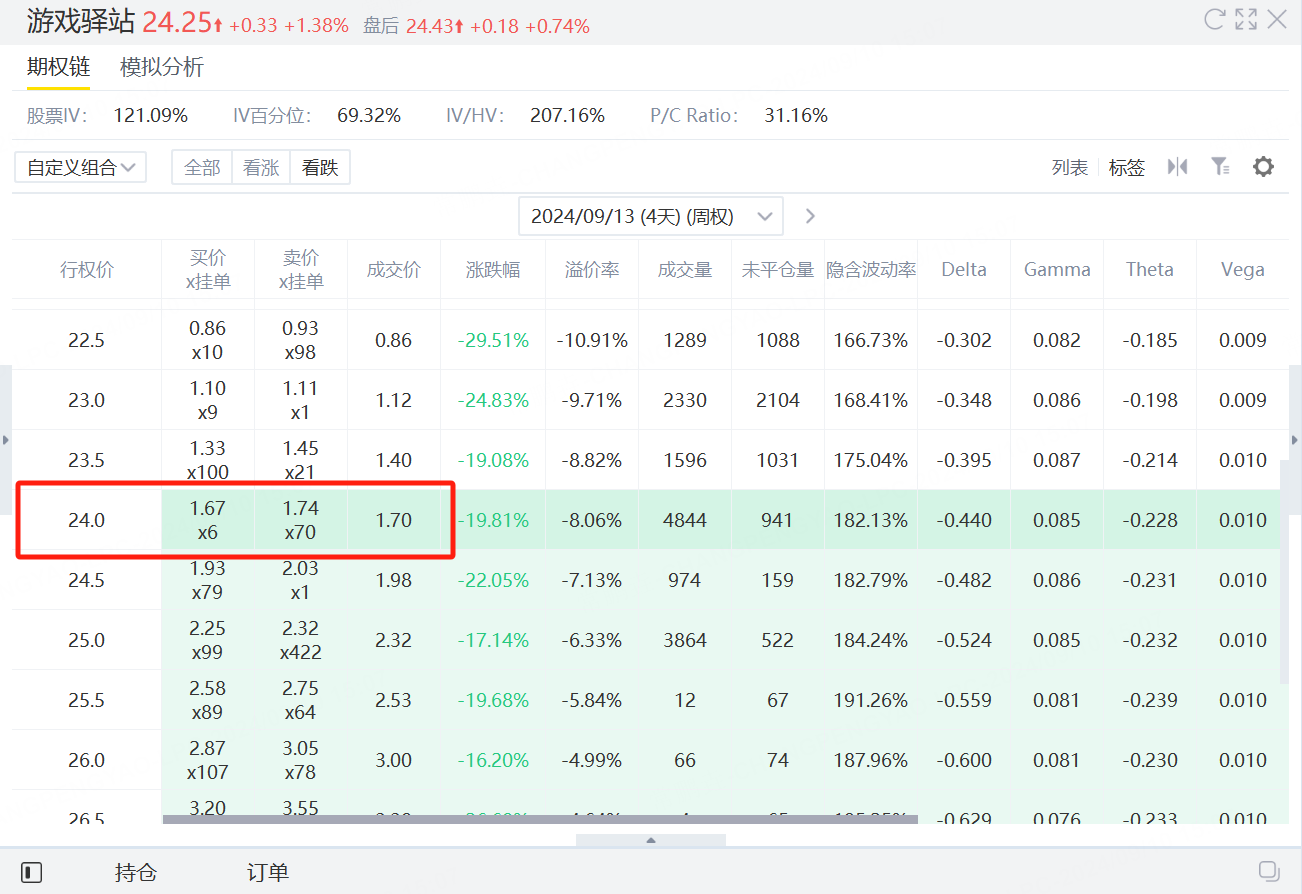

Current Stock Price: GameStop (GME) is trading at $24.25.

-Call Option: Strike price of $24, expiring on September 13, premium received $195.

-Put Option: Strike price of $24, expiring on September 13, premium received $170.1.

1.Total Premium

By selling these two options, the total premium collected is: $195 + $170 = $365

Maximum Profit: If GameStop's stock price is exactly $24 at expiration on September 13, both options expire worthless, and the investor keeps the entire premium of $365 as the maximum profit.

Risk of Loss: If the stock price moves significantly above or below $24, the investor faces potentially unlimited losses since the sold options can lead to substantial losses. Selling a straddle bets on low market volatility. If the stock price fluctuates less than expected, the investor profits; if it fluctuates more, losses occur.

2.Break-Even Points:

-Upside Break-Even: $24 + $3.65 = $27.65.

-Downside Break-Even: $24 - $3.65 = $20.35.

If the stock price is between these break-even points at expiration, the investor profits. If it moves beyond these points, losses begin.

By selling both call and put options, investors earn significant premiums but take on the risk of large price swings. This strategy works best if the investor expects minimal short-term volatility. If they anticipate substantial post-earnings movement, buying corresponding options to implement a long straddle might be a better approach.

Comments