Trump's statement on imposing tariffs stimulated panic in the U.S. stock market. The three major stock indexes of the U.S. stock market fell sharply at the end of the day, with a drop of more than 2% at one point. Among them, the share price of leading AI stocks fell nearly 9% on Monday to $114.06, with the highest intraday drop of more than 10% at one point.

Currently, Nvidia's stock price has fallen back to the level of last September, the price before the U.S. presidential election.The company's market value has shrunk to $2.78 trillion, and Monday's decline once again wiped $265 billion off Nvidia's market value. According to Dow Jones Market Data, Nvidia's current market value has shrunk by about $900 billion from its peak of $3.66 trillion on January 6.

Jordan Klein, a trading desk analyst at Mizuho Securities (Mizuho), said in an interview with the media that this is "a continuation of last week's market trend" and described this round of decline as a "cooling" of artificial intelligence trading.

CEO Jensen Huang said the company has solved problems related to its latest chip, Blackwell.

"Our performance next quarter will be good. The market demand pipeline for Blackwell chips is quite stable."

For investors who want to go long while controlling risk, consider using the ratio spread strategy.

What is a ratio spread?

A ratio spread is an options strategy in which a trader buys a call or put option on an at-the-money ATM or an out-of-the-money OTM and then sells at least two or more identical OTM options. A trader can buy or sell a call option (call ratio spread) or a put option (put ratio spread).

If a trader is slightly bearish, they will use a put ratio spread. If they are slightly bullish, they will use a bullish ratio spread. The ratio is typically two put options per long option, but traders can change the ratio. The maximum profit on a trade is the difference between the long and short strike prices, plus the net credit received (if any).

However, the disadvantage of the traditional spread method is that the upward profit is limited, and this problem can be solved by using the bullish ratio reverse spread.

A call ratio inverse spread is a call option strategy that involves buying a call option and then selling a call option with a different strike price but the same expiration date, using a ratio of 1: 2, 1: 3, or 2: 3. Since traders hold more long calls than short calls, this strategy may have unlimited upside profits. An investor using a call ratio contrarian spread investing strategy will sell fewer calls at a lower strike price and buy more calls at a higher strike price. A call option inverse spread is a bullish spread strategy designed to profit from a rising market while limiting potential losses from a downside.

Example of Nvidia Call Spread

Investors build a bullish spread strategy with the goal of reaping greater potential gains when the stock price rises. The implementation steps of the policy are as follows:

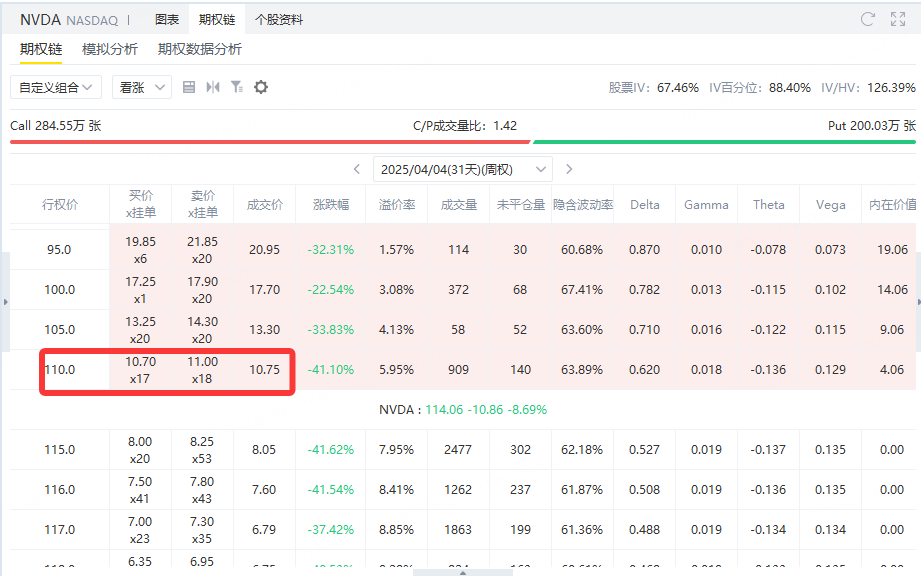

1. Buy a call option: Investors buy a call option with an exercise price of $110, and the option expiration date is April 4, 2024. The value of each option is $1,075. The purpose of this part of the call option is to capture higher upside profits when the stock price exceeds $110.

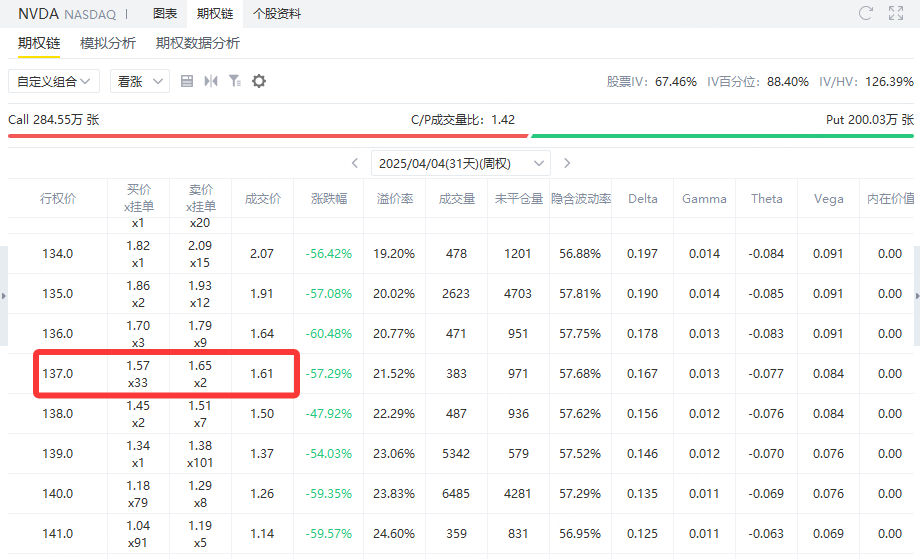

2. Sell call options: In order to offset part of the cost of buying a call option, the investor sells a call option with an exercise price of $137. The value of each option is $161 on the same expiration date. Call options sold can generate initial income when the stock price does not rise, but may lead to certain losses when the stock price rises.

Investors reduce costs by buying low-strike calls and selling high-strike calls while limiting maximum gains.

PROFIT AND LOSS

Transaction costs

Buy 110 strike price call option, pay$1,075

Sell 137 strike price call option, income$161

Net cost = $1,075-$161 =$914(i.e. maximum risk)

Profit and loss calculation

Maximum loss: $914 (neither option is worthless when Nvidia stock price ≤ $110)

Break-even point:$110 + ($914/100) =$119.14

Maximum profit:

Spread = $137-$110 =$27

Maximum profit = spread × 100-initial cost =$2,700-$914 = $1,786

Occurs when the stock price is ≥ $137

Summary

This strategy applies toBullish but not extremely bullishMarket expectations.

Advantages: The cost is lower than buying a call option outright, and the risk of loss is reduced.

Disadvantages: Limits upward income. If the stock price rises sharply, the profit is limited to $1,786.

If investors feel that the stock price may well exceed $137, it may be more appropriate to hold the call option directly. Otherwise, this bull spread strategy is a robust choice.

Comments

Great article, would you like to share it?