In 2024,$Broadcom (AVGO) $It can be described as the "last dark horse" in AI chip stocks! Its stock price will rise by more than 110% in 2024, and it will soar by more than 24% on the financial report day on December 12, setting the largest single-day increase in history. Its market value directly exceeded one trillion US dollars, becoming the 12th in the world and the 9th in the United States. A listed company with a market value of US $1 trillion.

However, after entering 2025, Broadcom's stock price has shown an adjustment trend with the general market trend, falling nearly 14% year-to-date, and its overall market value has fallen back to above US $900 billion.

On March 6, 2025 (after-hours Eastern Time), Broadcom will soon release its financial report for the first quarter of fiscal year 2025. The agency expects FY2025Q1 to achieve revenue of US $14.59 billion, a year-on-year increase of 21.98%; Earnings per share are expected to be $0.845, a year-on-year increase of 197.36%.

Focusing on this financial report, according to Bloomberg's consensus forecast, the semiconductor business is expected to grow by 10.31% year-on-year to US $8.152 billion, of whichASIC business increased by 62.09% year-on-year to US $3.728 billion.The basic software business is expected to grow by 41.69% year-on-year to US $6.477 billion.New business VMware increased 102.35% year-over-year to $4.249 billion.

Currently, the market is mainly focused on the development of ASIC business, new business VMware software business, and the impact of the Deepseek incident.

What's happening with Broadcom in the options market

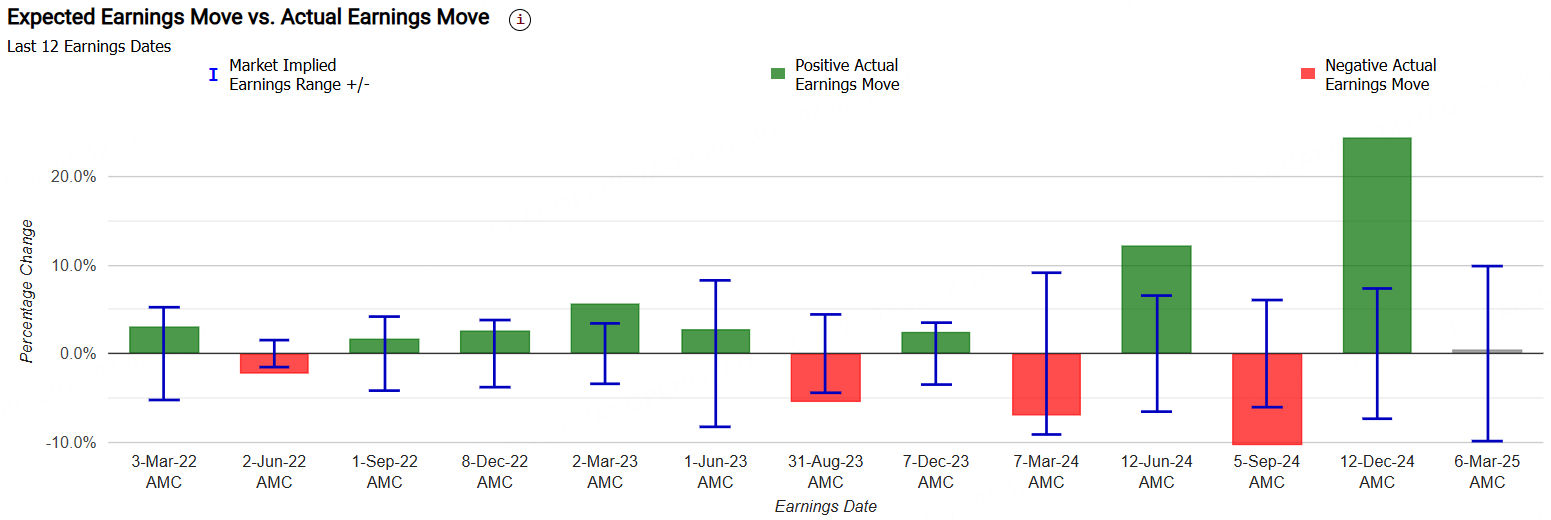

Currently, Broadcom's implied changes are±9.5%, indicating that the options market bet on its single-day rise and fall of 9.5% after its performance; In comparison, Broadcom's post-performance average stock price change in the first four quarters was±13.5%, showing that the current option value of the stock isUnderestimate。

The post-earnings gains and losses of AVGO in the last six quarters were +2.8%,-5.5%, +2.4%,-7%, +12.3%,-10.4%, and +24.4%, respectively.

The current options market expects AVGO to fluctuate by ± 9. 5% after the financial report. We can bet on AVGO's financial report by shorting the volatility.

What is the Wide Straddle Strategy?

In long wide straddle options, investors buy both out-of-the-money call options and out-of-the-money put options. The strike price of a call option is higher than the current market price of the underlying asset, while the strike price of a put option is lower than the market price of the underlying asset. This strategy has significant profit potential because the call option theoretically has unlimited upside if the price of the underlying asset rises, while the put option can make a profit if the price of the underlying asset falls. The risk of the trade is limited to the premium paid for these two options.

An investor shorting a wide straddle sells an out-of-the-money put and an out-of-the-money call at the same time. This approach is a neutral strategy with limited profit potential. Shorting a wide straddle option is profitable when the underlying stock price is trading within a narrow range between break-even points. The maximum profit is equal to the premium obtained by selling two options minus the transaction cost.

AVGO Short Wide Straddle Strategy Case

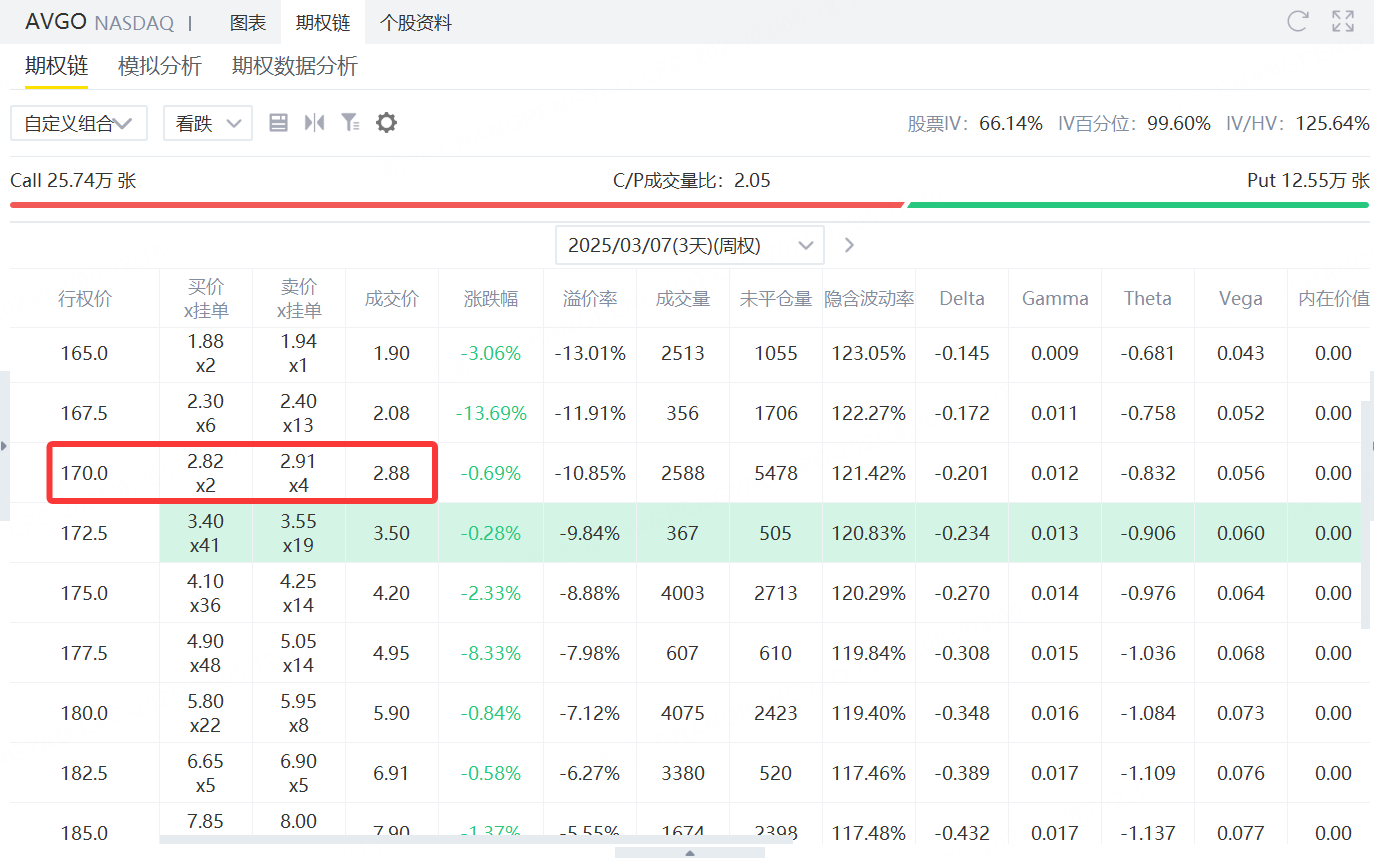

Stock AVGO is currently trading at around $190. Investors can implement the short wide straddle strategy by:

In the upside direction, investors can sell a call option with an exercise price of $210 expiring on March 7 and get a premium of $202.

In the downside direction, investors can sell a put option with an expiration on March 7 and an exercise price of $170, and get a premium of $288.

Strategy composition

SellExpires March 7$210Of exercise priceCall Options, obtained premium rights$202

SellExpires March 7$170Of exercise pricePut Options, obtained premium rights$288

Total premium Revenue: 202 + 288 = $490

PROFIT AND LOSS

Maximum profit

$490 (total premium revenue)

Occurred on March 7 when AVGO stock price was at$170 ~ $210Between, neither option is executed.

Break-even point

Upward direction:210 + 4.90 =$214.90

When the AVGO price is higher than $214.90, the loss begins to widen.

Downward direction:170-4.90 =$165.10

When the AVGO price fell below $165.10, the losses began to widen.

Loss potential

Unlimited risk of loss: If AVGO rises sharply, the call option sold could bringInfinite loss。

Limited but high losses: If AVGO falls sharply, the maximum loss of put options sold is(170-0) × 100 = $17,000。

Strategic risk

High risk and high return: suitable for expectationsLimited short-term volatilityBut there is still a certain amplitude of market environment.

Gamma Risk: Close to the expiration date, if AVGO price quickly approaches or breaks through 170 or 210, the losses could widen sharply.

Comments