The software sector, particularly in areas such as SaaS, cloud computing, cybersecurity, and AI integration platforms, will see divergent performance by 2025. While some companies will experience robust growth fueled by AI adoption, others will face declining demand as AI replaces their services.

The acceleration of corporate digital transformation, the widespread adoption of AI applications, and the robust demand for efficient tools—coupled with macroeconomic factors like government shutdowns and concerns over AI profitability—have intensified market volatility, causing stock prices to fluctuate wildly. Many stocks have become overly sensitive to AI news (which has also created favorable buying opportunities).

According to industry research, high-growth software companies are projected to achieve revenue growth of 13-25% this year, with generative AI capabilities emerging as a core competitive advantage.

Detailed Analysis of Recent Trends in Key Companies

Trend data is based on year-to-date (YTD) performance through late October/early November 2025, focusing on stock prices, revenue, and forecasts. AI demand is the primary driver, but volatility makes investing feel like a rollercoaster ride.

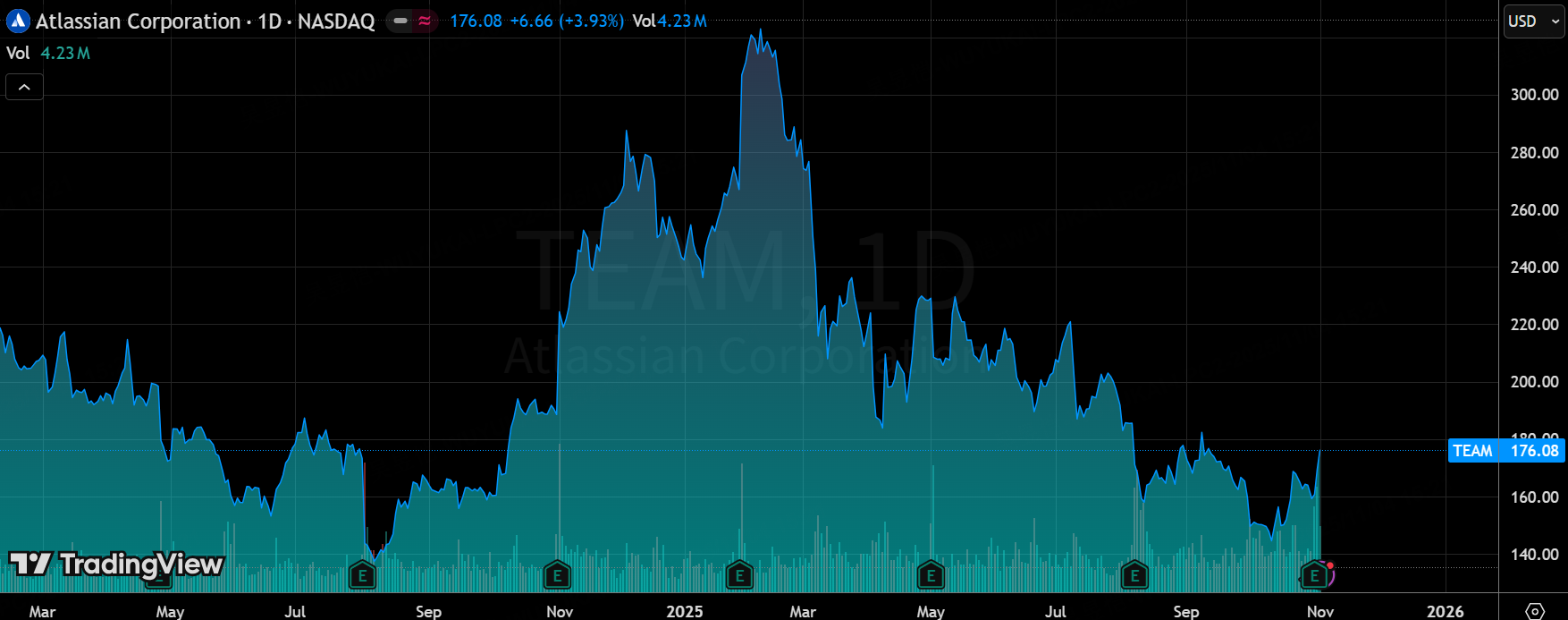

1. $Atlassian Corporation PLC(TEAM)$: Cloud business exceeds expectations + AI-driven growth, reiterating Buy rating. On November 4, the stock rose 3.93% in a single day, but long-term volatility persists. Over the past six months, it has cumulatively declined 29.63%, with the share price currently in a "short-term rebound, mid-term correction" phase. The company's core logic is "cloud business growth exceeding expectations + AI-empowered customer paid expansion." Q1 FY26 cloud revenue grew 26%, exceeding investor expectations (24%). Key drivers included: Paid seat expansion: Customers using AI code generation tools exhibited a 5% higher paid Jira seat expansion rate than non-users, demonstrating AI's significant impact on customer retention; Data center migration: Enterprises accelerated shifts from on-premises to cloud-native deployments, boosting cloud migration-related revenue growth; Cross-selling: Products like the Teamwork Collection drove higher ARPU (average revenue per user), with cloud ARR (annual recurring revenue) excluding migration growing 35% year-over-year.

Financial Guidance and Long-Term Outlook

Guidance Upgrade: FY2026 cloud revenue growth guidance raised from 21% to 22.5% (+150 basis points), total revenue growth raised from 19% to 20.8% (+180 basis points), non-GAAP EBIT margin raised from 24% to 25.5% (+150 basis points), with continued profitability improvement.

Long-term goals: Achieve a compound annual growth rate (CAGR) exceeding 20% for total revenue in fiscal year 2027, non-GAAP EBIT margin exceeding 25%, and a free cash flow margin 500 basis points higher than EBIT margin (projected to exceed 30%). Financial health score of 59 points (neutral), gross margin maintained at high levels (82.84% over the past 12 months), and fiscal year 2026 EPS forecast of $4.31 (first-ever profitable outlook).

2. $MongoDB Inc.(MDB)$ : AI-driven data demand + new CEO boost drive earnings above expectations. The company appointed CJ Desai as its new CEO (formerly of NOW and NET, with industry experience rated "all-star caliber"). The company forecasted "FY2026 performance exceeding the upper end of guidance," with its core Atlas business (cloud database) performing strongly. Customer demand is concentrated on AI data storage and processing. The company is positioned as a "data infrastructure winner" in the AI era. As a leading document database platform, MDB directly benefits from AI-driven "explosive data growth"—AI model training and inference require vast amounts of unstructured data, and Atlas's flexibility precisely matches this demand. This aligns with trends in "Software Development Technology Trends" such as "the rise of multi-model databases" and "edge computing data processing." Real-time data generated by edge devices requires efficient storage, and MDB's distributed architecture meets the demands for low latency and high scalability.

3. $ServiceNow(NOW)$ : Short-term pullback + long-term AI transformation, positive outlook under optimistic scenarios. Previous gains driven by AI transformation expectations have led to short-term profit-taking. The business focuses on enterprise IT operations and process automation, positioning it as "back-office SaaS." Its client base primarily consists of large enterprises with highly stable demand. Optimistically, NOW is recognized as an "AI Innovation Leader." Successfully transitioning to an "outcome/usage-based pricing model" (replacing traditional per-seat billing) could offset AI-driven pressures from "reduced knowledge worker headcount," accelerating revenue growth. This makes it a "second-growth candidate empowered by AI."

4. $Snowflake(SNOW)$ : Catalyzed by developer conference + AI data demand, hits 52-week high. Short-term catalyst is the "Snowflake BUILD 2025 Developer Conference" (online, Nov. 4-7, 2025), where the market anticipates new AI data processing offerings (e.g., LLM and data cloud integration tools). Active $320 call option trading reflects investor bets on further post-conference stock gains, signaling confidence in its AI data infrastructure leadership. The core concept is the "deep integration of AI and data processing"—AI model training requires accessing vast amounts of dispersed data. Snowflake's data cloud platform enables cross-enterprise, cross-scenario data integration, positioning it as the "data hub" of the AI era. Regardless of Citigroup's base/pessimistic/optimistic scenarios, it maintains competitiveness (even in the pessimistic scenario, hyperscale cloud providers still require its data integration capabilities).

5. $CrowdStrike Holdings, Inc.(CRWD)$ : Security as a core need + AI empowerment drive stock to new highs. No clear near-term downside risks; growth logic stems from "cybersecurity necessity + AI technology integration." As "cybersecurity remains a high-priority budget area for enterprises"—regardless of AI advancements—risks of data breaches and ransomware attacks persist, ensuring stable demand for CRWD's endpoint security and threat detection products. Concurrently, its AI-driven threat prediction capabilities (e.g., real-time identification of novel attack patterns) further enhance product competitiveness, maintaining customer renewal rates above 90%.

6. $Twilio Inc(TWLO)$ : Short-term pullback after earnings validation, no clear negative catalysts. As a cloud communications SaaS provider (SMS, voice APIs), it benefits from the trend of "customer engagement digitization" among enterprises. Its Q3 2025 earnings report confirmed revenue growth (15%-18%) in line with expectations. Its client base primarily consists of e-commerce and internet companies, demonstrating moderate demand resilience.

Overall Trend in the Software Sector: AI-Driven Differentiation, Cloud Services + Business Model Transformation Emerge as Key Factors

1. Core Trend 1: AI Drives "Winner-Take-All" Dynamics, Intensifying Valuation Polarization

Current Market Segmentation: As of August 2025, the median expected EV/Revenue NTM for high-growth software companies (growth rate >20%) stands at 11.7x (doubled from 2022 lows), while low-growth companies (<10% growth) averaged only 3.5x (approaching the 2016 "SaaS bloodbath" trough). Free cash flow valuations similarly diverged (high-growth: 56.2x vs. low-growth: 16.0x).

Differentiation Logic: AI Doesn't Disrupt SaaS—It Filters Winners —Data infrastructure providers (MDB, SNOW), AI-empowered customer teams (TEAM), and essential domains (CRWD) emerge victorious, while companies reliant on traditional per-seat pricing models and lacking AI innovation face marginalization.

Pessimistic Scenario: AI replacing traditional SaaS providers (such as $Adobe(ADBE)$ and $Workday(WDAY)$), benefiting hyperscale cloud providers + data infrastructure ( $MongoDB Inc.(MDB)$ , $Snowflake(SNOW)$);

Base Scenario: Industry giants (Atlassian Corporation PLC (TEAM), ServiceNow (NOW)) offset per-seat pressure through AI innovation to sustain growth;

Optimistic Scenario: Leading companies (NOW, MSFT) transition to "pay-for-performance" models, achieving accelerated growth and increased M&A activity.

2. Core Trend 2: Cloud Business as the "Growth Anchor," Rating Upgrade Keyed to Guidance

Cloud growth rate determines valuation: TEAM's cloud business surged 26% → rating upgraded; MDB Atlas business remains robust → earnings beat expectations; SNOW Data Cloud benefits from AI → hits 52-week high. Cloud business growth has become the core metric for institutions to assess the value of software companies.

Cloud Acceleration: Enterprise "Data Center Migration" Continues (TEAM Cloud Migration Drives 35% ARR Growth), with Global Enterprise Cloud Adoption Rate Projected to Exceed 60% by 2025. Small and Medium-Sized Software Companies That Fail to Complete Cloud Transformation Will Gradually Lose Competitiveness.

3. Core Trend 3: Business Models Shift from "Per Seat" to "Per Value," Mitigating AI Disruption

Transition Direction: Traditional per-seat pricing (vulnerable to impacts from AI-driven "knowledge worker reduction") → Outcome/usage-based pricing (e.g., NOW's "pay-per-process-automation-outcome" model, SNOW's "pay-per-data-call" model).

Transformation Outcomes: TEAM increased seat expansion rate by 5% through AI tools. Under an optimistic scenario, NOW can sustain revenue growth through transformation, demonstrating that "AI + business model transformation" effectively hedges risks.

4. Core Trend 4: Technological Trends (Low-Code, Microservices, Edge Computing) Strengthen Leading Positions

Low-Code + AI: Lowering Development Barriers TEAM and MDB launch "AI Code Generation Tools" to boost customer development efficiency, indirectly driving paid conversions.

Microservices + Cloud-Native: MDB and SNOW's distributed architecture aligns with enterprises' demand for "flexible scaling," while edge computing (supported by 5G) further drives real-time data storage requirements (benefiting MDB and SNOW).

Security and Compliance: CRWD and SNOW integrate "Data Security Compliance" features, aligning with the global trend toward stricter data privacy policies (such as the EU GDPR and China's Data Security Law) to enhance customer retention.

Comments