$微软(MSFT)$

Microsoft’s 3QFY26 report is not only about strong cloud growth.

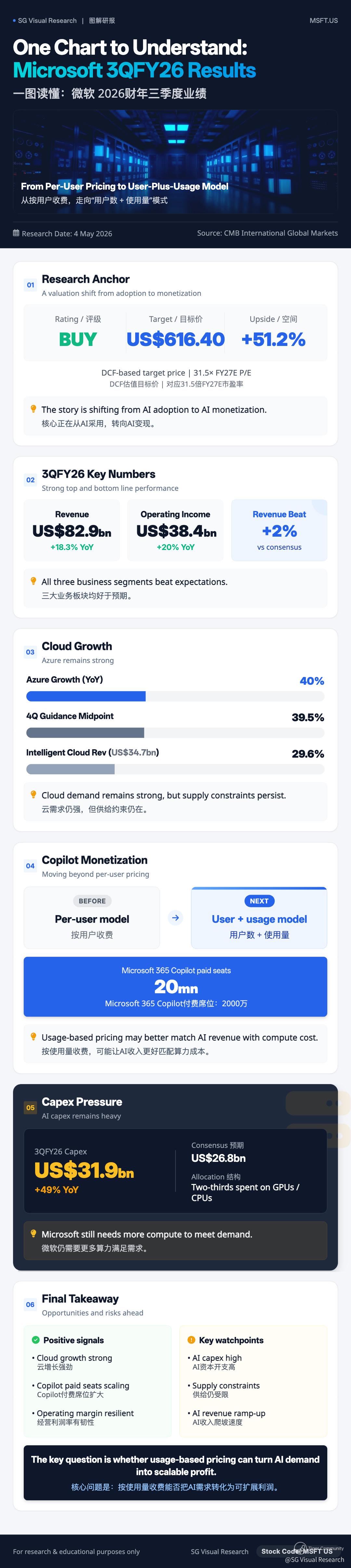

The more interesting point is the pricing shift:

from a per-user model

to a user-plus-usage model.

That could matter for how AI products are monetized over time.

Key numbers:

Revenue: US$82.9bn, +18.3% YoY

Operating income: US$38.4bn, +20% YoY

Azure growth: +40% YoY

Microsoft 365 Copilot paid seats: 20mn

At the same time, AI capex remains heavy.

3QFY26 capex reached US$31.9bn, with around two-thirds spent on GPUs and CPUs.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Comments