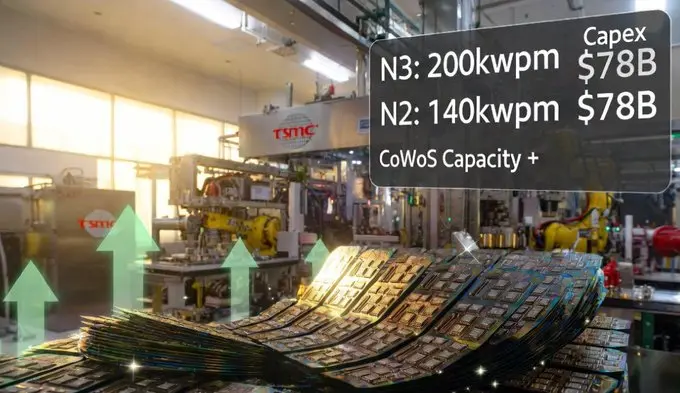

$Taiwan Semiconductor Manufacturing(TSM)$ They just raised the bar again on 3nm/2nm and CoWoS capacity through 2027, with higher capex directly tied to AI demand expansion.

The N2 ramp is particularly notable—faster early output than N3, which signals how aggressive AI-driven wafer demand has become.

Margins are still holding strong in the high-60% range, which shows pricing power isn't fading even as supply expands.

The big picture is, this remains the core bottleneck name in the entire AI supply chain.

The question now seems simple: does demand keep outrunning capacity, or do we eventually see some digestion after this multi-year ramp?

What's your read here—early cycle, or late-stage expansion?

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

Comments