Oriental Patron maintained a BUY as 1H22 earnings beat estimates with strong growth in e-commerce and kids’ wear

· 1H22 net profit rose 37.2% yoy to RMB551mn. Meanwhile, revenue rose 17.6% yoy to RMB 3.65bn. No dividend was declared.

· E-commerce and 361º Kids businesses are the main growth drivers

· More professional products to boost AWP

· Maintain BUY and TP of HK$5.25

1H22 earnings beats.We attribute this to the strong growth in e-commerce and kids’ wear and the lower effective tax rate (21.3% versus 30.7% in 1H21). 361 Degrees managed to increase the average wholesale price (“AWP”) while maintaining the sales volume. It reported a GPM of 41.5% in 1H22, down slightly by 0.3p.p. yoy. Operating profit rose 8.7% yoy to RMB772mn, mainly due to the 30.7% yoy increase in selling and distribution expenses to RMB604mn amid efforts on brand enhancement. 361 Degrees said it maintained mid-to-high-teens retail sales growth between July and Aug. The company plans to increase its footprint in the first and second-tier cities, and it is considering a slight reduction in the discount to wholesalers in the future.

E-commerce leads the growth. Sales of the web-exclusive products increased 60.3% yoy to RMB782mn. The fast-growing e-commerce business offset relatively slow sales growth (+9.6% yoy) in the offline channels. 361 Degrees launches precise product promotion and marketing campaigns to activate the engagement of online members to enhance their stickiness.

Booming contribution from 361ºKids.Revenue from 361 Kid increased 37.1% yoy to RMB 683mn. The company has started to expand 361 Kids’ retail network. In 1H22, 361 Kids’ points-of-sale (“POS”) increased by 201 on a net basis to 2,097. The company plans to increase the POS to 2,200 in the future. 361 Kids’ is the 2 nd largest Chinese kids’ wear brand. The company differentiates through collaboration with youth sports associations and launched more co-branded products with IP such as “Dunhuang”, “Miffy” and “NONOPANDA”.

More professional products to boost AWP.In 1H22, the average wholesale price (“AWP”) of footwear and apparel increased 6.9%/13.8% yoy respectively. Other than the cost-driven price hike, the company has upgraded the product mix by launching a variety of new products with higher AWP. For example, 361 Degrees launched a matrix of professional running shoes, ranging from top-tier carbon plate running shoes for racing, to running shoes for amateur runners, catering to the needs of runners at all levels.

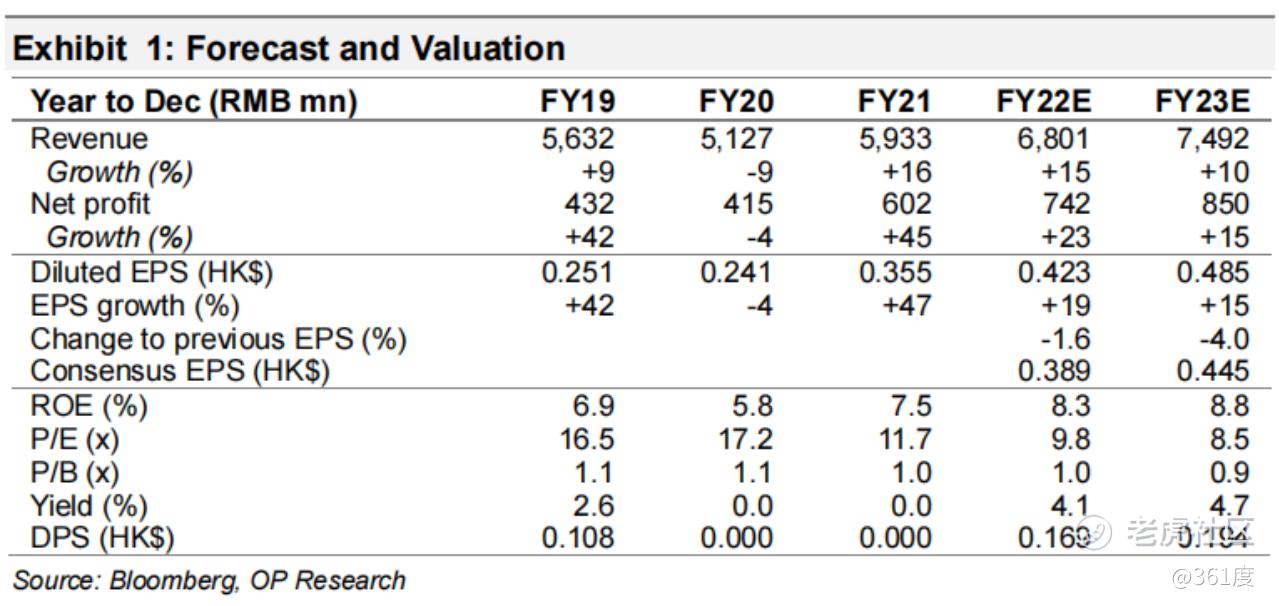

Maintained BUY and TP of HK$5.25. The TP represents 10.8x PER for FY23E, or ~ 50% price discount to its domestic peers. We tune down forecast on 361 Degrees’ EPS by 1.6%/4.0% to HK$0.423/0.485 in FY22E/23E, to reflect the lower profit margins. 361 Degrees could stand strong against headwinds in the retail market thanks to the focus in lower-tier cities and on the mass market. With RMB5.4bn of cash and deposits on hand, 361 Degrees has the financial muscle to reward investors with dividends and/or to make sizable acquisitions. These actions may serve as a re-rating catalyst.

Comments