Thesis

In my opinion, Rivian (NASDAQ:RIVN) is a speculative story-based long-duration asset that is priced to perfection.Valuedat a one-year forward EV/Sales of about x10, the company has arguably little room to misstep.

But on 10 Octobera major misstep happened: Rivian hasannounceda recall ofnearly allof the company's past EV deliveries. The trading day following the news, RIVN shares have lost as much as 11%.

I don't think Rivian's long-term prospects will be severely impacted by the EV vehicle recall. But still, the company's valuation is simply too high for investing with the risks associated to a story-led business case - especially given the current environment with depressed sentiment towards growth stock.

Rivian stock is down some 80% YTD. But there is still excessive risk in the company's valuation. Sell.

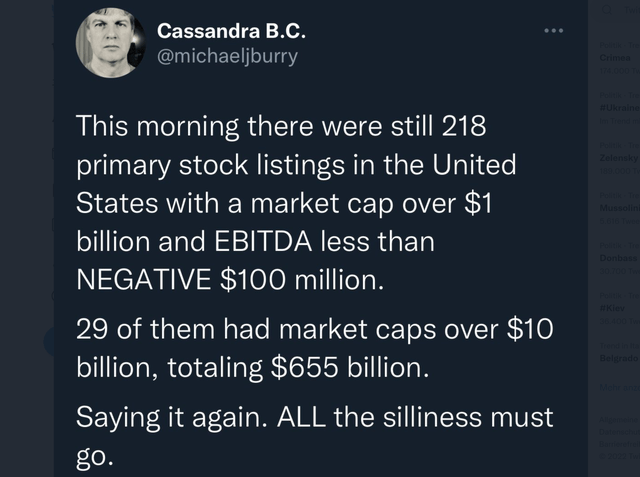

Michael Burry's Warning

Before I present the arguments why I consider RIVN risky, I would like to highlight a recent tweet from Michael Burry.On September 30, Burry highlighted that as of said day, there were still 218 companies trading in the U.S., companies with greater than $1 billion valuation and negative TTM EBITDA of at least $100 million.

Commenting that this 'silliness' in markets must go, Burry implies that those overvalued companies should re-price sharply to the downside.

Following Burry's Tweet Michael Burry Stock Tracker hascompileda list of the most vulnerable companies (highest market cap) that fit Dr. Burry's screening. As you note, RIVN ranks as number six.

Financials Make Little Sense

Rivian's financials make absolutely no sense, in my opinion. For thetrailing twelve months, Rivian generated about $514 million of revenues and a gross profit of negative $1.67 billion. Adding to this number $1.93 billion of selling, general & administrative expenses, $2.26 billion of R&D expenses and an additional $660 million of other expenses, operating income for the period was negative $6.12 billion.

I am not presenting these financials because I believe the company is structurally unprofitable. I am presenting these numbers because I would like to highlight that Rivian is in such early days of business, that the company's fundamentals are - from a financial analyst perspective - almost impossible to analyse.

In my opinion, such a setup would be okay for a startup. But it is unacceptable for publicly-listed businesses valued at more than $30 billion.

On a more positive note, however, I must admit that Rivian's balance sheet is well capitalized.As of June 30, Rivian posted cash and cash equivalents of $14.92 billion, against total debt of only $1.66 billion.

Priced To Perfection...

I strongly believe that every investment opportunity is a function of price. And Rivian is simply not priced attractively. According to datacompiledby Seeking Alpha, Rivian is valued at a one-year EV/Sales of nearly x10. Given non-existent profitability, the respective EV/EBITDA and/or EV/EBIT is not available.

Notably, Rivian is priced at a stretched EV/Sales multiple, despite a 70% sell-off since the company's IPO about a year ago.

...But Disappointments AccumulateLower Production Target

Rivian had originally said to build 50,000 trucks in 2022. But earlier this year, in March, the companyhalvedthe production target to 25,000 vehicles - citing supply chain shortages. But honestly speaking, there could also be some demand issues: Amazon (AMZN), which is Rivian's biggest investor, and expected to be the truckmaker's biggest customer, hasagreed to buy trucks from a rival Stellantis(STLA) (which caused also a 10% share price drop).

EV Recall

On October 10th, Rivian said that the company has become aware of a production issue - a 'loose nut' that could cause the driver to lose control of steering. But the company also affirmed that:

'to date, we are not aware of any injuries that have resulted from this issue.'

As a consequence of the production issue, Rivian announced to recall about 12,200 vehicles, which is nearly everything the company has delivered so far. Although the technical problem should be easy to solve and 'take no more than a few minutes' the announcement highlights.

The trading day following the announcement, Rivian shares lost as much as 11%.

Upside Potential

After Tesla's (TSLA) enormous success, it's much more difficult to argue that next-generation auto manufacturers such as Rivian will not be successful. And of course, I could very well picture a scenario where Rivian is going to be successful. In fact, with Amazon as a partner, Rivian already enjoys a strong commercial and financial sponsorship. And thejoint manufacturing plantrecently announced with Mercedez-Benz could support Rivian's technical and engineering competence.

Scaling up production as an EV manufacturer is notoriously hard. But if Rivian succeeds, while also claiming similar margins as Tesla, then RIVN stock's valuations might not be that silly after all.

Conclusion

As I see it: Rivian is operating like a start-up. Rivian posts financials like a start-up. Rivian stumbles like a start-up. But Rivian is a publicly listed company with a plus $30 billion market capitalization. Will investors allow anything else than perfection? I doubt they will. And in my opinion, they shouldn't.

The issue that I have with RIVN stock is anchored on valuation. In my opinion, the stock should be priced not like a mature automaker, but like a start-up. So that investors may pay a price that allows for a margin of safety - a margin of safety for RIVN to stumble without exposing investors to the pain of a 10% crash.

In the context of such high market capitalization and negative EBITDA, I find Michael Burry's tweet 'ALL the silliness must go' accurately reflects my thesis regarding Rivian's stock valuation.

Comments