$Apple(AAPL)$ After the US stock market closed in the early morning of July 28, Beijing time, it announced its financial report for the third quarter of fiscal year 2021 (as of June 30, 2021), and the "new season" products represented by iPhone12 continued to harvest in an all-round way.

Financial highlights of this quarter:

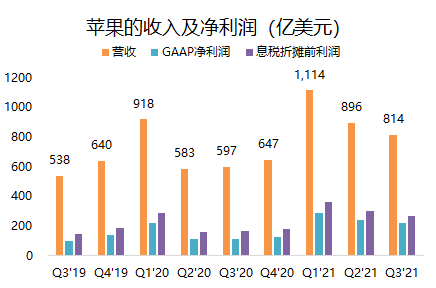

- Total revenue was 81.4 billion US dollars, a year-on-year increase of 36%, higher than Wall Street's consensus expectation of 79.3 billion US dollars, and also set a new high in revenue during the same period;

- GAAP net profit reached 27 billion US dollars, and EPS was 1.3 US dollars, exceeding the expected 0.89 US dollars;

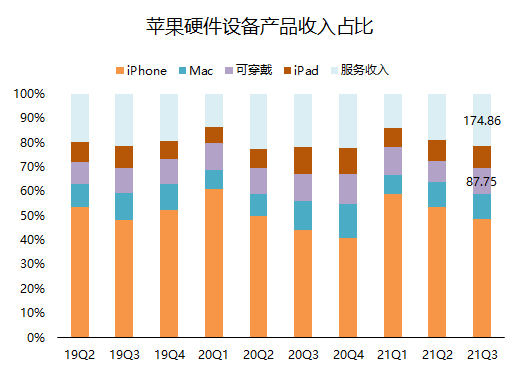

- In terms of products, iPhone sales revenue was 81.4 billion US dollars, higher than the expected 79.3 billion US dollars; Mac sales revenue was 8.24 billion US dollars, higher than the expected 7.99 billion US dollars; IPad sales revenue was 7.37 billion US dollars, higher than the expected 7.13 billion US dollars; Wearable and home equipment revenue of 8.8 billion US dollars was higher than the expected 7.63 billion US dollars; Service revenue was $17.48 billion, higher than the expected $16.32 billion. One of the limiting factors for the growth of product revenue is chip production; The loss of revenue caused by the shortage of chips is at the lower limit of the official forecast range of 3 billion to 4 billion US dollars;

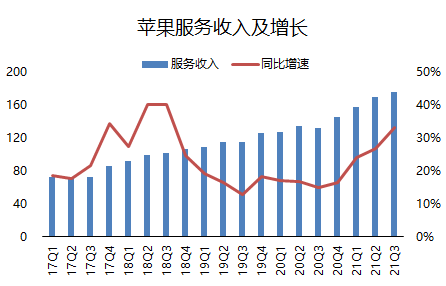

- The gross profit margin of the company was 43.3%, an increase of 80 basis points over the previous quarter. The main boosting factor was the increase in the proportion of service income with higher profit margins, because the gross profit margin of hardware products and service income decreased by 10 basis points respectively. This also shows that service income has a growing impact on Apple;

- From a regional perspective, Apple's equipment installation base has reached the highest level in history in every region, and the trading accounts and paid accounts of digital content stores have reached record highs in every market segment, with double-digit growth. The paid subscriptions of all services on the platform have exceeded 700 million. At the same time, more people began to upgrade their old mobile phones to iPhone12 with 5G functions, including some Android mobile phone users who began to buy the first iPhone;;

- Sales revenue in Greater China reached US $14.76 billion, up 58% year-on-year, although it showed a substantial growth trend as in the first two quarters of fiscal year 2021, and the year-on-year growth rate was weaker than over 87% in the previous fiscal quarter.

Don't give guidance continuously, because Apple can't see through the market?

Apple did not give guidance in its earnings report for the next quarter, but the CFO said in a telephone conference that Q4 will still achieve double-digit year-on-year growth through September. This statement is actually very vague, because everyone knows that Apple is facing several problems at present:

- Although the service business is strong, it will still usher in the ceiling

- Chips and other parts are in short supply, and hardware growth is limited

- Exchange rate fluctuation

In the service business, the growth rate of revenue alone is definitely in full swing. But how much stamina can this growth rate have? Is there any benefit in the post-epidemic era in FY 21? It's hard to say.

However, from another indicator-deferred service income, we can see that the growth rate of short-term deferred income (generally the amount of income recognized within one year) in Apple has begun to decline. Most of the short-term deferred revenue is contributed by Apple Care in insurance business and Arcade in games business.

This also brings the same problems. Hardware growth has also strongly driven Apple Care's insurance business. Is Apple Care's growth a good thing? If you are insured, when Apple's next generation new machine has no core innovative functions, will you choose to update the new machine or replace an old "new machine" with Apple Care?

Therefore, it depends to a great extent on whether Apple has more innovative products.

In addition, the chip shortage cannot be solved well at least in the short term, which not only affects the progress of Apple's asset chip M1, but also makes the revenue in the next few quarters more subject to Qualcomm.

On the display screen, can the expected new series usher in a breakthrough? It is said that the new iPhone 13 series to be launched in September will also use SAMSUNG EL.GDR's 120Hz LTPO OLED panel, but it supports 120Hz adaptive refresh rate and brings intelligent adjustment of screen refresh rate function, which is also regarded as oneA kind of progress.

Stock price depends entirely on repurchase?

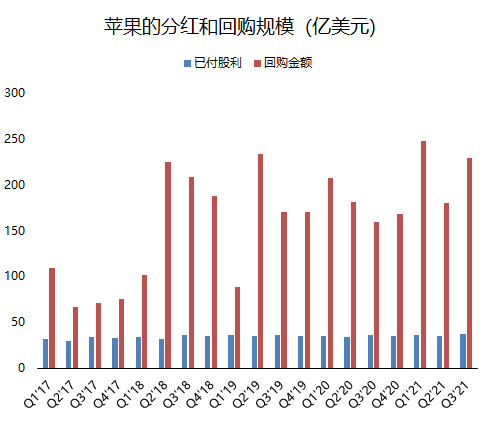

Yes, an important move supporting Apple's share price is that it spent $22 billion on share buybacks this quarter, compared with the previous quarter, including a $5 billion accelerated buyback program launched in May, and wrote off 32 million shares.

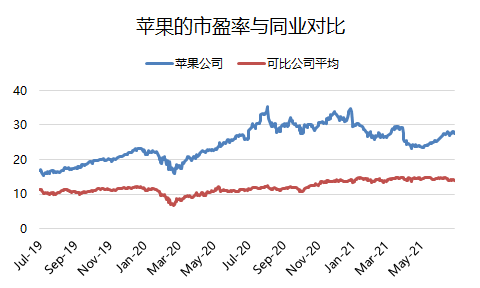

Repurchase can change the company's EPS intuitively, because the total share capital is less, and the earnings per share will naturally increase. This also makes Apple's price-earnings ratio relatively stable at a level, while its stock price has been soaring.

However, there are still some premiums compared with international counterparts. After all, as a global technology leader, its scarcity is irreplaceable. But on the other hand, it is not incomprehensible that the average stock price will return to 20 times PE one day because of the slowdown in growth and other reasons.

However, for Apple, more investors are willing to bet on his continuous upgrading and innovation. After all, this is the strategic plan. If not, the turning point will soon appear.

Comments

1. Share price rally was prices in for the earning calls. Remember that $AAPL was rally unusually

2. Forecasted guidance for the shortage of chips that is going to hit the company