Summary

- Nubank is already the largest bank in Brazil, with licenses incoming for other countries with large unbanked populations and still long growth horizons.

- The credit card business is a great way to start in markets unregulated and start developing presence among the unbanked with great APRs.

- The ecosystem model makes sense and the open field will mean massive ROI on low industry customer acquisition costs.

- Being Buffett backed, share price is likely to at least hold, and the business benefits from reflexivity with cash burn and equity raises likely to return money faster than dilution.

- Main risk is market sentiment towards unprofitable and growth style businesses, where sentiment needs to drive the reflexivity effects and keep reinvestment rates so high.

- Looking for a helping hand in the market? Members of The Value Lab get exclusive ideas and guidance to navigate any climate.

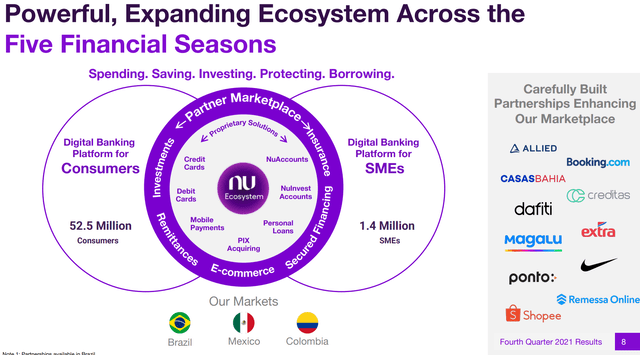

Q4 Proves the Ecosystem

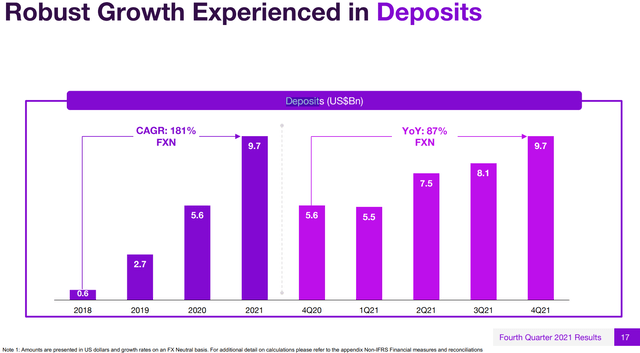

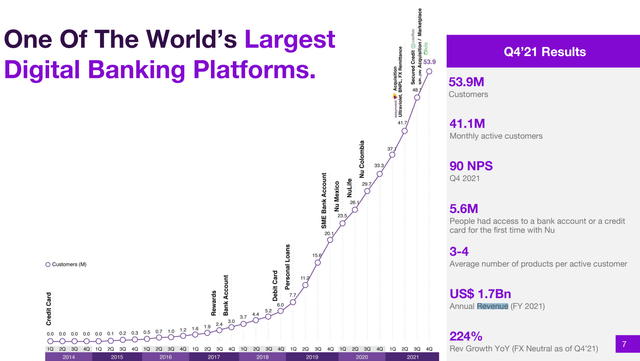

The Q4 is looking attractive.The maturities are short on the credit card and bank loans, and the high APRs mean that together there is rapid and substantial payback of the loans given out to these otherwise unbanked customers. This open field means that Nubank is the first mover in digital retail banking and has become the largest bank in Brazil with users engaging with the several products that Nubank offers, including mobile payments, personal loans, credit cards and even investment accounts. Opportunities are also abound in short-term consumer finance, with partnering with merchants going well and having a part of the business imitate the well-received Klarna concept.

Reflexivity and Valuation

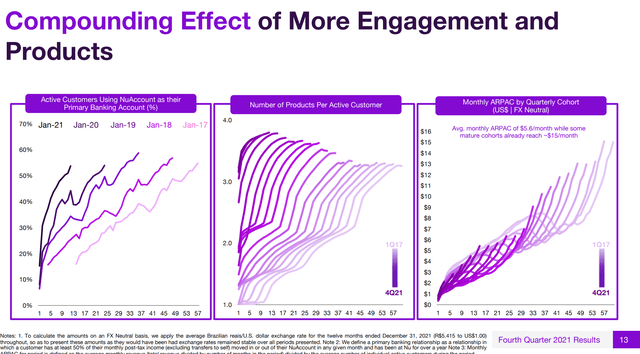

While Nu's markets are pretty large, so are its already existing active users. 41 million people is a lot, with current markets containing realistically around 500 million people depending on how Nu expands into other markets. 10% is already a decent penetration, so the sustained and long-term growth here on will have to come from the ecosystem and from greater cross-selling. Since growth is as recent as this quarter, maturity of the customers in recent cohorts into becoming more involved with the ecosystem has yet to be observed, and indeed 10% penetration is still quite low, so revenue growth should continue, but we expect that in the next 2 years we will see some diminishing marginal returns. Mexico and Colombia are still only 1% penetrated, with almost all the users being Brazilian, so we don't want to understate the meaningful growth that is coming ahead.

With Mexico and Colombia advances having barely started, marketing expenses are just going to rise, and financed by the stock backed by strong institutional presence with Buffett has traditional playersscared and even abandoning ship. With the mature customer providing an average revenue per quarter of $15, a 3x ROI at least if not 12x assuming that customers stay on for a year, a conservative assumption, the reinvestment rates are superb right now. Flywheel models mean a winner-take-all dynamic, and Nubank being an early mover can justify a high multiple, with growth rates above 200% likely to compress that 30x P/S multiple pretty quickly to more reasonable levels.

Although with consumer finance businesses likeKlarna -which face customers with similar credit profiles and services of which Nubank is beginning to offer itself in partnership with merchants -valued at around 45x, the multiple is already looking interesting. With operating leverage incoming and profitability only a couple of years away, and growth rates likely to hold a while longer with the big Colombian and Mexican populations still barely reached, you can start being optimistic about a SPY listing, and that'll only increase liquidity. We are bullish on Nubank, to be sure. The main risks are that it is a growth style company, and jitters in the market could turn favour away from them to more value names; and with reflexivity cutting both ways, the business' reinvestment rates would suffer due to worsening financing terms. But with growth already having taken a recent hit, we think Nubank has the wind at its back.

Comments