KEY POINTS

- Amazon's online sales are slowing down.

- Cloud infrastructure is being built by Amazon Web Services worldwide.

The e-commerce giant has a more important division than its consumer-facing one.

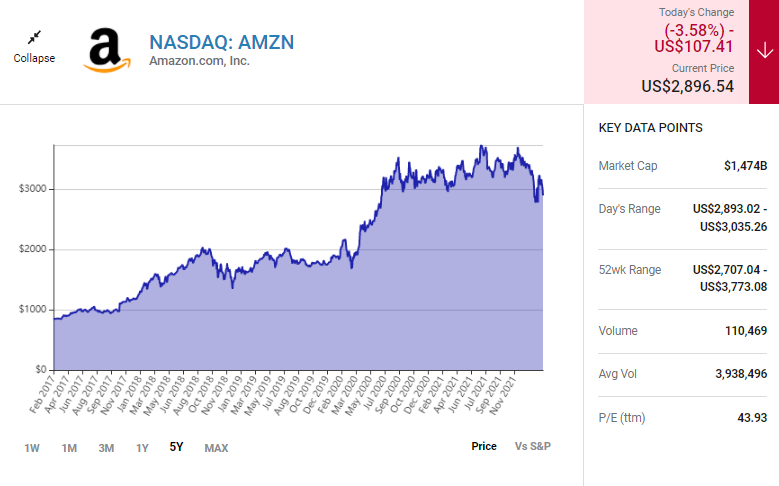

Since the turn of the century, few stocks have provided returns likeAmazon. From Jan. 1, 2000, the stock has returned an impressive 4,050%, easily outpacing the market. However, since July 2020, Amazon's stock has been relatively flat, only returning 10%, whereas theS&P 500is up around 50%.

As we move further into 2022, Amazon's stock will need to outperform to catch up to the market average. A closer look at Amazon's 2021 earnings reveals both good and bad news about its potential to do this. With the stock price currently down around 15% from its all-time highs, does it have what it takes to get back to those levels, or even exceed them? Let's look at the potential and the problems that Amazon management is encountering.

The red flag: Online sales growth is slowing

Much of Amazon's stock success was built on its e-commerce platform's growth. Using Amazon Prime, consumers could buy from a list of millions of products and have the product arrive at their doorstep within two days of the shipment's start. During the height of the COVID-19 pandemic, Amazon saw outsized growth as more people turned to the service to get what they needed while so many stores were forced to temporarily close. Amazon fulfilled orders for both necessary supplies and luxuries, paid for by consumers sometimes armed with extra stimulus check money.

After all that growth, Amazon's online sales have plateaued in comparison to 2020 levels. In both the third and fourth quarters of fiscal 2021, Amazon's online sales only grew at a 3% and 1% clip, respectively. Granted, these are being compared with COVID-accelerated quarters, but even so, Amazon should have reported growth at least in line with e-commerce growth in general. Digital Commerce 360 estimates overall third-quarter and fourth-quarter e-commerce growth at 6.8% and 9.4%, respectively. That means Amazon is growing slower than the e-commerce space as a whole.

Offsetting this slowdown in revenue growth was Amazon's announcement it would increase the price of its Amazon Prime subscription service from $119 to $139 annually. With more than 200 million Prime members worldwide, the $20 yearly increase will generate more than $4 billion in additional revenue annually --ifall its customers renew.

That's a big "if," unfortunately. With competitors likeWalmartoffering its subscription variant, Walmart+, consumers may decide to test out their options outside of Amazon Prime. Additionally, if consumers are committed to finding the cheapest-priced product -- something becoming more common with inflation's impact -- taking an additional five minutes to price-check on Walmart oreBaycould save consumers money.

Amazon's slowing online sales growth is concerning. Couple that with it trying to flex its pricing power with its Prime subscription service in an inflationary environment, and this could signal more serious problems.

The green flag: Amazon Web Services is a monster

Fortunately, Amazon has a saving grace. With 32% of theglobal cloud infrastructuremarket share in Q3, according to Statista, Amazon Web Services (AWS) is the leader in an important space. Huge companies likeMeta Platformsand Pfizerare powering their operations with AWS. Switching cloud providers isn't an easy task, so companies ensure they select the proper provider before making this monumental business decision. With Amazon's commanding lead, it will be hard to unseat it from its position.

AWS's growth is speeding up with each ensuing quarter, as seen in the chart, showcasing the impact cloud computing is having on businesses.

| AWS Year-Over-Year Growth | ||||

|---|---|---|---|---|

| Q4 2021 | Q3 2021 | Q2 2021 | Q1 2021 | Q4 2020 |

| 40% | 39% | 37% | 32% | 28% |

Data source: Amazon.

In 2021, AWS brought in $62.2 billion in sales and had anoperating marginof 30%. AWS is an incredible business and far outpaces Amazon's retail business, which doesn't make the company much money, as the chart shows.

| Region | 2021 Sales | Operating Expenses | Operating Margin |

|---|---|---|---|

| U.S. | $279.8 billion | $272.6 billion | 2.6% |

| International | $127.8 billion | $128.7 billion | (0.7%) |

Data source: Amazon.

Keep in mind that the AWS numbers only include that segment, where the retail business also includes inherently high margin business like subscription and advertising services, meaning Amazon likely loses money on the items it sells.

Even though AWS is the crown jewel in Amazon's empire, it still only makes up 13% of total sales. If AWS can keep up its growth, it will become a larger part of the revenue stream and increase Amazon's overall profitability with its higher margins.

Investor takeaway

Until AWS becomes a larger part of the revenue stream, Amazon's stock offers too much uncertainty. When you add in the potential negative impact of pending antitrust lawsuits for the company, Amazon should consider doing something crazy, like spin off its AWS segment. I would be a buyer in that spinoff, at nearly any price.

Amazon isn't going away anytime soon. It's way too big for that. Amazon has a place in this world for consumers and businesses alike, but with dwindling online sales, I'm unsure if it belongs in my portfolio as a growth stock.

Comments