Summary

The widely-followed Ark Invest funds, led by Cathie Wood, have sold out of Palantir.

Share sales occurred just a month after big-ticket buys.

I believe Cathie Wood is wrong in selling Palantir as the firm is ramping up its free cash flow and has huge revaluation potential.

Michael Vi/iStock Editorial via Getty Images

In February, Cathie Wood's actively-managed investment funds have sold millions of shares of the software and analytics firm Palantir (PLTR), raising questions as to what the motivation for the trades might have been. While Ark Invest funds are selling out of Palantir, PLTR is one stock that I am buying now hand over fist. Palantir's free cash flow growth is underestimated, and I will bet that Cathie Wood will be proven wrong on its decision to offload PLTR!

Ark Invest funds have eliminated Palantir from the stock roster

Over the last two weeks, Cathie Wood, head of the Ark family of actively-managed ETFs, sold almost all shares of Palantir which were chiefly held in the firm's two largest investment funds: the Ark Innovation ETF (ARKK) and Ark Autonomous Technology & Robotics ETF (ARKQ). Both funds are classified as "active equity ETFs", meaning investment decisions and trades are executed on a daily basis. The Ark Innovation ETF had reported net assets of $12.97B and the Ark Autonomous Technology & Robotics ETF had net assets of $1.64B at the end of January.

In the last week, Ark Invest funds sold more than11M shares of Palantir in what can only be described as a massive post-earnings dump. Share sales began after the software and analytics firm submitted its earnings card for Q4'21 which caused the stock to gain downward momentum. However, Palantir's post-earnings stock crash must be seen in connection with other tech stocks which also cratered after submission of quarterly results. In both of Cathie Wood's flagship funds, Palantir now no longer has a representation.

The sale of shares of Palantir is surprising because Cathie Wood added substantially to this investment all throughout 2021. Ark Invest ETFs even bought Palantir just a month ago, in January 2022, due to skidding valuations in the tech sector. In January, Ark Invest funds bought hundreds of thousands of shares in Palantir for$10.5M. The implied price for trades made in January was around $17 per-share.

Significant losses have resulted for Ark Invest from closing out the PLTR holding

Since Ark Invest closed out its Palantir investment after the firm's earnings-related price drop, the funds sold at the worst possible time. The majority of trades will have likely occurred between $10.50 and $12.50 which is the trading range that shares of Palantir dropped into after earnings submission. This means that, only on the latest purchases from January, Ark Invest's estimated realized losses are between 25-40%. Cathie Wood's investment funds also bought millions of shares of Palantir in thefourth-quarter of 2021 when PLTR traded way above $20. On these trades, losses were significantly higher. It has been said that Cathie Wood's losses on the Palantir trade could be as high as$380M.

A possible explanation for Ark Invest's Palantir stock sales

The burning question, however, is why Cathie Wood chose to sell almost all of Ark Invest's holdings in the software and analytics firm. After all, Palantir submitted a decent earnings card for the fourth-quarter that showed considerable business promise, especially in the commercial segment where the firm is crushing it with growing average revenue per customer, higher margins and soaring customer acquisition.

The reason behind the sales can likely be explained by Cathie Wood looking to invest in higher-conviction, pure-play names that have a higher chance of rebounding once the market digests the current onslaught of bad news. Cathie Wood likely monetized the Palantir position not over concerns over Palantir's business performance but rather because Ark Invest needed additional cash resources to double down on names the investment firm believes have stronger recovery potential. Tax loss selling may also be a reason why the Ark Invest funds ditched Palantir just a month after adding significantly to their investments. The sales do suggest, however, that Palantir was a low-conviction play all along.

Investors should focus on Palantir's material free cash flow ramp, not Ark Invest's trading activity

I understand that many investors like to follow other popular investors for investment ideas. But I believe it was a mistake for Cathie Wood to sell Palantir because of the firm's significant free cash flow ramp that the market continues to underestimate. Palantir's commercial business is on fire and customer acquisition is accelerating, which will translate into massively improving free cash flow prospects for the firm and its shareholders in FY 2022 and FY 2023.

With more customers signing on to Palantir's platform, the firm is facing a long runway of free cash flow growth. Palantir's commercial customer count increased 200% in FY 2021 to 147 paying clients and monetization in the commercial segment, as Idetailed here, is improving considerably.

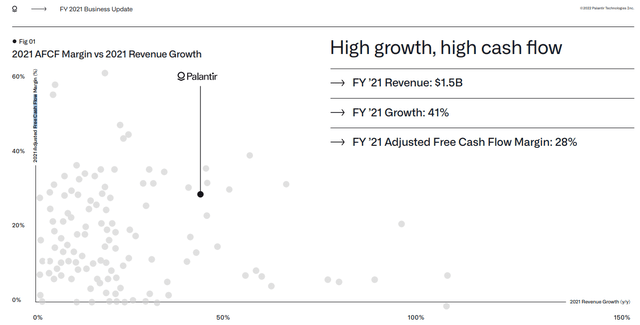

Because the firm is making inroads in the commercial market, Palantir's free cash flow improved from $(272)M in FY 2020 to $424.1M in FY 2021, so the last year was truly a breakthrough year for Palantir. The free cash flow margin, an indicator of profitability, increased from (25)% in FY 2020 to 28% in FY 2021.

Palantir

The increase in free cash flow profitability in FY 2021 also made Palantir one of the fastest growing and most profitable companies in the software and service sector.

Palantir

FY 2022: Look for free cash flow growth and margin improvements

If Palantir can sustain free cash flow margins of around 30% in FY 2022, the software firm is looking at free cash flow of at least $600M this year. Revenues for FY 2022 are expected to be around $2.0B and even without material increases in average revenue per customer, Palantir could see a 50% year over year increase in free cash flow this year.

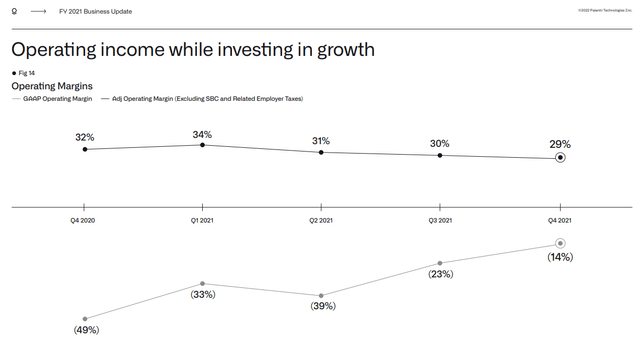

What will also change in FY 2022, if the business keeps expanding in the commercial segment, is Palantir's operating margins. Palantir regularly exceeded its own guidance for adjusted operating margins, in part because the firm doesn't want to disappoint. In FY 2022, Palantir could see a boost to its free cash flow margins and its operating margins as more (commercial) clients take up paid service offers and move into the scale phase. For that reason, I expect Palantir's operating margins to approach 35% by year-end 2022.

Palantir

Palantir's sales growth has become too cheap

Palantir's market-capitalization-to-sales-ratio (FY 2023) dropped to just 9.5 X after a significant drop in pricing in Q4'21 and Q1'22. Palantir's revenues are expected to increase at least 30% this year and I believe Palantir could actually deliver top line growth of 35-40% due to momentum in its commercial business. For this reason, I believe Palantir's growth remains significantly undervalued.

Final thoughts

Investors should not jump to hasty conclusions about the massive sale of Palantir shares in the Ark Invest funds. While it may be true that Palantir has been less of a high-conviction investment for Cathie Wood than other names, managing liquidity and harvesting tax losses likely played a large role in determining which stock position would get the boot from the Ark Invest portfolio. Palantir's business continues to show a lot of promise and I believe free cash flow could ramp up 50% this year while operating margins are also set for improvement. Palantir's growth is cheap, and the stock is a buy!$Palantir Technologies Inc.(PLTR)$

Comments