$Upstart Holdings, Inc.(UPST)$ , has gained a lot of attention from shareholders based on the high growth forecasts and the FinTech disruption model that is taking on the traditional consumer loan sector. Since the stock dropped some 70% from the highs, we will analyze the fundamental standing in order to see if there is an opportunity for investors.

Growth Expectations

Upstart has made some significant strides and entered a high-growth stage as the company's revenues increased by 286.6%, which is more than the 3-year average growth rate of 207.3%.

For the future, we can estimate a fundamental revenue growth rate. We start by looking at how much Upstart has reinvested into the business based on Net CapEx.

Last year, Upstart invested some $7.5m as Net CapEx. We add this on top of the current invested capital of $451m and compare it to how much revenue the company is expected to get from its total invested capital. We utilize the Sales to Capital ratio of 1.9 as a proxy for quality of investment.

This results in a long term fundamental growth rate of about 82% for revenues, and -5.1% for EBIT. Indicating that the top line will grow, but profits aren't catching up yet.

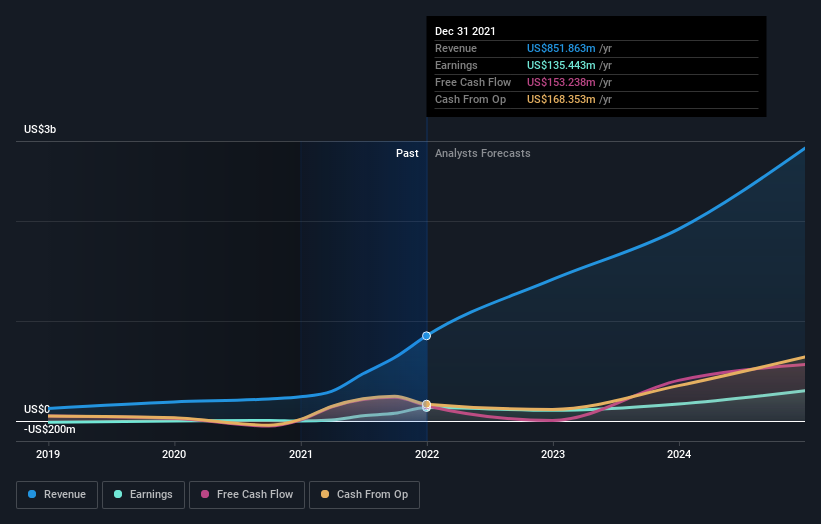

This is close to what we see as analyst projections in the chart below.

Analysts seem to have a similar picture for the future of the company. For FY 2023, they estimate $1.4b revenues, a growth rate of 66% compared to 2022. They also expect profit to drop, and go from $135m to $106m in 2023, a 27% decline.

As we can see from our analysis and from the estimates of analysts, the company is expected to post high top line growth and earnings should decline in the short term.These forecasts seem to be fundamentally justifiedbased on the amount of reinvestment management does into the business.

Growth Sailing

Theappealand competitive advantage of a disruptor platform that is aiming to take on traditional financial services, is that theironline application can conduct business with a fraction of the costs. In that regard, we should expect to see high revenue growth, with a lower gross margin, or efficient scaling.

Currently, that is what Upstart is successfully doing, as revenues grew 286% more than the costs associated with delivering the services (COGS). This stems from the high 86% gross margin.

This is great, because the company is scaling revenues while keeping costs low, also known as unit good economics.

We can also dig a layer down and see if business expenses are keeping up with growth. This is important because some companies spend too much in marketing or other items in order to drive "cheap" growth, which is unsustainable in the long run.

However,Upstart seems to be positively scaling revenues in relation to total costsby 127.8%. This means that the company is successfully growing without sacrificing profitability.

At the end of the day, everything we analyze ties into the final valuation, and investors want to know if the numbers above make Upstart a potential investment.

Final Thoughts - Valuation

Upstart Holdings appears to be overvalued by 26% at the moment, based on our discounted cash flow valuation.

The stock is currently priced at US$100 on the market, compared to ourintrinsic value of $93.

Many investors look at per share prices, but the full market capitalization puts things into better context. In the case of Upstart, investors are buying a $9.8b business. This can potentially change our thinking, from buying a stock that dropped some 70% from its highs, to buying a FinTech company for $9.8b - A 70% drop may seem like an opportunity, but a $9.8b valuation is a very serious number.

There is one very positive aspect that needs highlighting. Upstart has a return on capital employed of 8.5%, which increased from 3.2% 3 years ago. Given that the return is exceeds the 6.5% cost of capital, Upstart is creating value for shareholders. This means that even if you buy the company at a premium, it will increase its value while growing and has good potential to surpass the current value in the medium to long term.

So while earnings quality is important, it's equally important to consider the risks facing Upstart Holdings at this point in time.Case in point: We've spotted2 warning signs for Upstart Holdingsyou should be aware of.

Source: Simply Wall St.

Comments