Since hitting a high of $370 in October last year, $Sea Ltd(SE)$ has dropped by 60%, and the market value has returned to the level at the beginning of the epidemic in 2020. When the "tide" faded, Sea returned to normal growth from high growth in the past two years. What valuable information did this Q4 financial report reveal?

2021Q4 Highlight

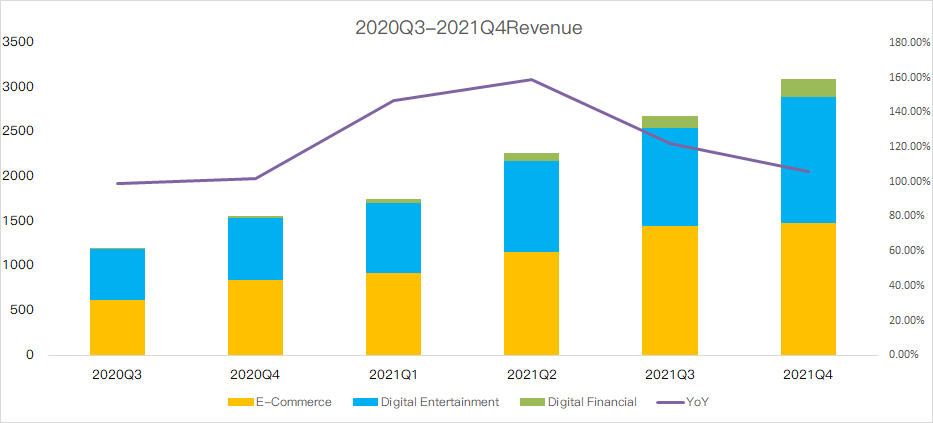

GAAP's total revenue was USD 3.2 billion, up 105.7% year-on-year.

Gross profit was US $1.3 billion, up 145.6% year-on-year.

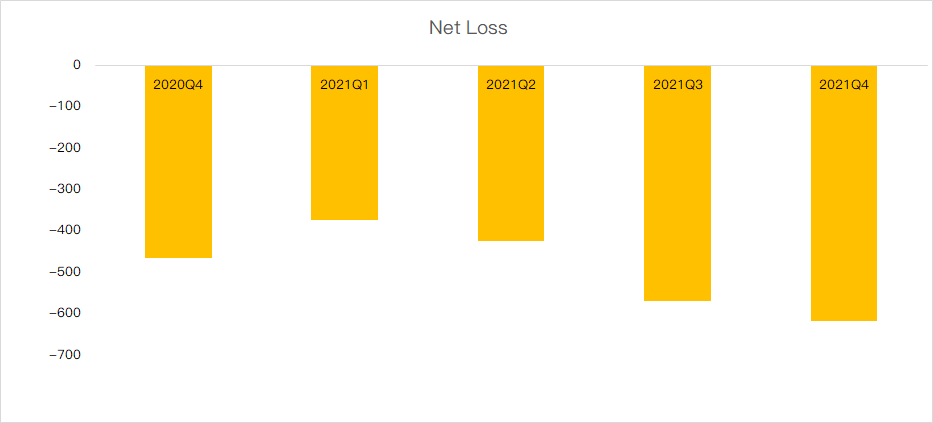

The adjusted EBITDA was-$492.1 million, compared with $48.7 million in the fourth quarter of 2020.

Banned in india, and globalization is blocked

In the fourth quarter, Sea's revenue growth rate was 105%, falling back to the low point of the year; In the past three years, the revenue growth rate was 163%, 101% and 127%, while Bloomberg's growth forecast for 2022 has been revised down to 45%, so it is necessary for investors to re-examine the growth path of Sea.

The income growth rate of various departments has declined to varying degrees. E-commerce has become the largest source of income for the second consecutive quarter, but the year-on-year growth rate has dropped to 89.4%; Revenue from digital finance business surged seven times year-on-year to US $797 million, mainly due to the low base in the same period.

In the past two quarters, Sea faced a series of headwinds, such as slower growth, increased losses, Tencent's reduction of holdings and regulatory risks. In fact, Q4 financial report itself is weaker than India's ban, and investors are most worried about a series of subsequent effects that India's ban may bring.

India's ban on Free Fire occurred in February this year and has no relationship with the fourth quarter. According to Sensor Tower, gaming revenue in India currently accounts for only about 3% of total revenue. However, the significance of the blockage in the Indian market is that the global expansion may slow down in 2022.

India is definitely the market that Sea wants to win and values most. Especially, after more than two years of epidemic dividends, the penetration of game users in Southeast Asia is relatively saturated, while "Free Fire" ranks first in the best-selling list of mobile games in India for several consecutive quarters, and more than 30% of new downloads come from India. India's natural demographic dividend is very important to maintain the expansion of users. If the Indian market is difficult to unseal, the impact on users will be enormous.

Hematopoietic capacity is weakened,losses are expanded

After Sea returns to the normal growth stage, the valuation is more matched with the profit. Unfortunately, the net loss of Q4 is still expanding year-on-year, and exceeds market expectations. Investors obviously don't want to see it when liquidity is tightened, even if the company shows its determination to realize profits faster by drawing efficiency in 2022.

Concerns about losses mainly come from three aspects:

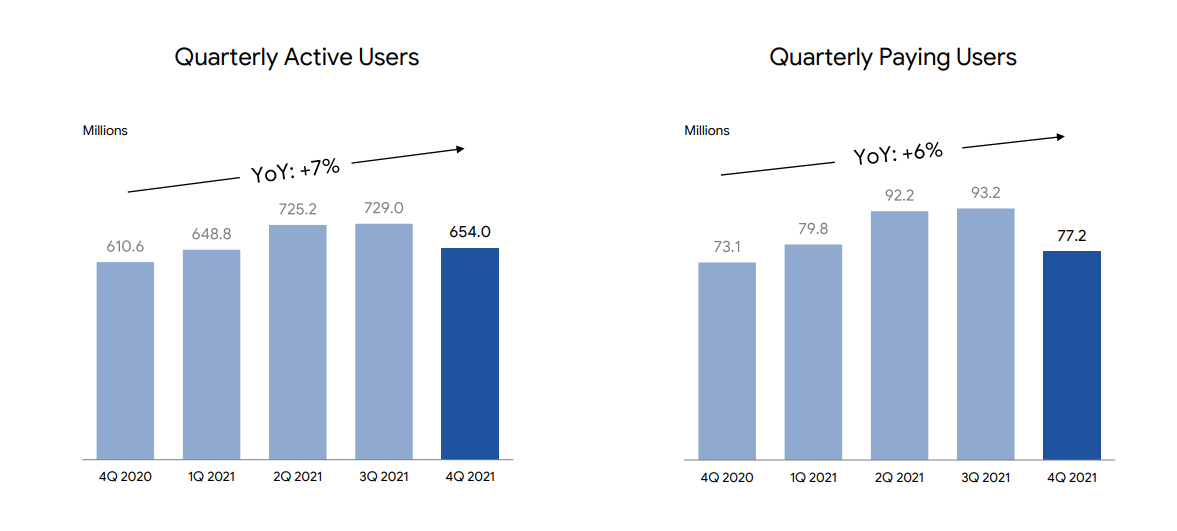

1) The profit of the game department dropped sharply. The bookings of Q4 and DE departments, the number of paying users and the growth rate of DAU all dropped sharply to single digits.

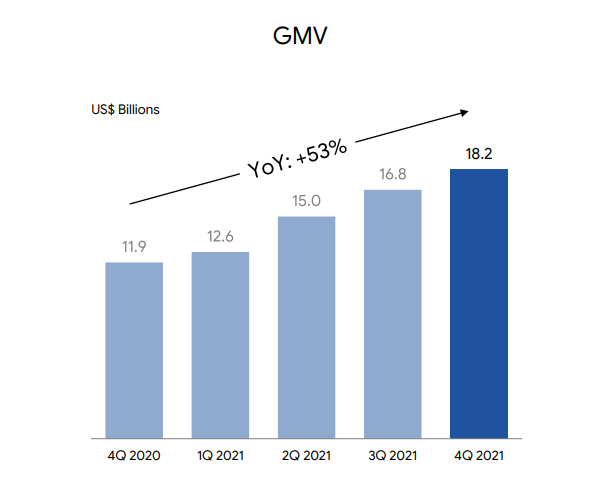

2) The loss of the e-commerce sector expanded, and Shopee was constrained by the weakening of the hematopoietic capacity of the game sector. Q4, the growth rate of e-commerce GMV was 52.7%, compared with 113% in the same period last year; GAAP's revenue growth rate was 89.4%, and the adjusted EBITDA was-877 million US dollars. The loss doubled year-on-year, and the input and output were not proportional.

3) The loss of the digital finance sector increased from US $511 million in 2020 to US $616 million.

Overall, Sea's adjusted EBITDA for this quarter was-$492 million, compared with $48 million a year earlier. In exchange for high investment, the income stalls and the losses expand. Only the 10 billion cash on the account can give investors a little comfort.

There are differences in institutional investor

From November 2001, we saw that the turnover of Sea in the secondary market began to enlarge obviously. Near the end of the year, due to tax planning, listed companies often choose to sell stocks to cash out, and the fourth quarter is often a high-frequency period for institutions or executives to adjust positions; On the other hand, risk aversion warmed up, money piled into TMMNG, the leading technology stock, and second-tier growth stocks were abandoned.

In the fourth quarter, institutions also had obvious differences on Sea.

Looking through the latest 13F document, the top three holding institutions (Puxin Group, Sands Capital Management and Capital World Investors) all reduced their holdings of Sea in Q4, and the reduction continued until 2022Q1. The first thing that bears the brunt is that Tencent, the major shareholder, reduced its shareholding ratio from 21.3% to 18.7% under regulatory pressure, and its voting rights fell below 10%. The company's share price plummeted by 11% that day.

The guidance is not optimistic

Of course, in the fourth quarter, there were many bulls who increased their holdings of Sea, such as Gaoling, Jinglin and Tiger Global, and Ark just increased its holdings by 140,000 shares. Judging from the stock price trend, these institutions are also likely to be locked up.

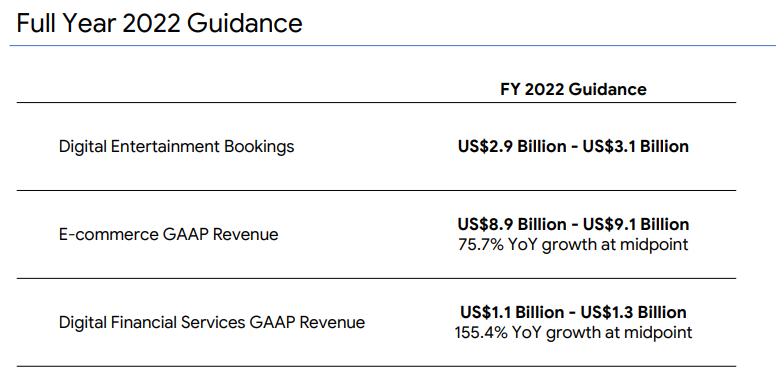

Looking ahead, Sea expects the booking amount of digital entertainment in 2022 to range from US $2.9 billion to US $3.1 billion, and says that with the opening of COVID-19 pandemic's post-economy, online activities will slow down, and considering the uncertainty, it is expected that the booking amount in 2022 will be close to the level in 2020. That compares with $4.6 billion booked last year.

Sea predicted the GAAP standard revenue of financial service institution SeaMoney for the first time, and it is estimated that the revenue in 2022 will be between 1.1 billion US dollars and 1.3 billion US dollars; Sea expects e-commerce revenues to be between $8.9 billion and $9.1 billion.

Comments