$Netflix(NFLX)$ Netflix ( NFLX -1.61% ) shares are having a tough winter this year. The stock is trading 44% below the all-time highs of late October 2021, including a 34% drop in the first two months of 2022. In particular, many Netflix investors flinched when the company reported so-so results for the holiday quarter with projections of a subscriber slowdown in the next reporting period.

Did Netflix deserve the stalled stock charts of recent months or is the media-streaming veteran a no-brainer buy today? Let's find out.

The bear case against Netflix

A couple of details jump out when Netflix is viewed through a pessimistic lens:

Subscriber growth is slowing down in the company's older and more established markets. This could be a sign of total customer counts peaking someday soon.

The video-streaming sector is jam-packed with competitors nowadays, and many of them undercut Netflix's premium subscription prices by a wide margin. A basic subscription to Walt Disney's ( DIS 1.13% ) Disney+, for example, costs $8 per month while the cheapest Netflix option will run you $10 per month. Moreover, Netflix is raising prices on higher-end plans in North America this spring, which could scare away customers.

Netflix reported negative free cash flows again in the fourth quarter of 2021. At the same time, the stock trades at a lofty 35 times trailing earnings. Shouldn't the constant cash burn motivate a sharp share price correction?

The bull case for Netflix

Netflix bulls must grapple with the risks listed by their bearish colleagues. Here's how:

The subscriber growth can be lumpy from time to time, and the effects of temporary slowdowns or growth spurts are magnified by Netflix's increasingly massive scale. The company has 222 million paid subscribers now, and that's a 9% increase over the last four quarters. And management likes to point out that Netflix gets less than one-tenth the screen time of old-school linear TV in the U.S. market. The opportunity for deeper engagement and continued customer growth is still massive.

If Netflix slashed its subscription prices to a flat $8 per month in an effort to compete with the House of Mouse from a different angle, that would be a catastrophic move. Quarterly revenues from the U.S. and Canadian market would plunge from $3.3 billion to $1.8 billion, wiping out the bottom line and kicking the improved cash flows back to the stone age. The company's ability to create award-winning and audience-grabbing content would evaporate immediately. I don't see how cut-rate original productions for a bargain-basement monthly fee can compete with top-notch content for a premium price.

Management made it clear that 2021 would produce roughly breakeven free cash flows, followed by sustainable cash profits in 2022 and beyond. That hasn't changed. Netflix consumed $159 million on the free cash flow line in 2021, which works out to a cash margin of negative 0.5% -- pretty close to breakeven. Netflix still expects to deliver positive annual cash flows from now on, promising to return excess profits to shareholders through stock buybacks.

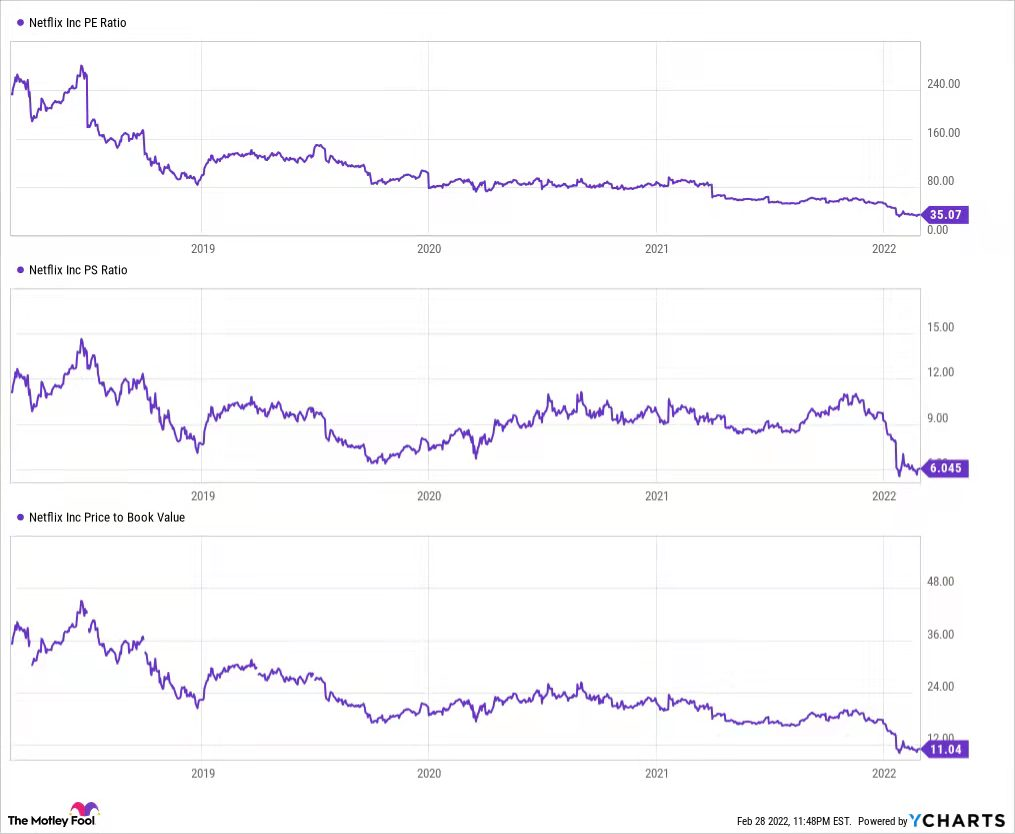

Regarding the rich valuation levels, Netflix shares don't look terribly expensive from a historical point of view. Here's how Netflix's valuation has fared in recent years, as measured by three popular metrics:

Should you buy, hold, or sell Netflix today?

Over the four-year period seen in the chart above, Netflix's revenues increased by an average annual rate of 23.5% while share prices only gained 7.9% per year. The S&P 500 market index rose by an average rate of 12.4% across the same period. That's an unmistakable sign of a misunderstood and undervalued stock.

In light of the bearish side's best arguments and the relative ease of refuting them, I can barely contain myself from pounding the table over the unique buying opportunity Netflix offers right now.

Comments