Visa(V) has a strong position in the digital payment industry, but its competitive advantage to peers is increasingly being challenged by competitors and the recent dispute with Amazon in the U.K shows that in online shopping its moat may be questionable.

Background and Competition

As I've analyzed in aprevious article, Visa is a company that is well positioned to benefit from the secular growth trend of payments gradually moving to digital channels. As the second-largest payment technology company in the world, only behind China's UnionPay, Visa is present throughout the world, has a very well recognized brand, and a vast network effect that is not easy to challenge.

This business profile has allowed the company to charge relatively high fees to merchants, which don't want to lose revenues by not accepting one of the most widely accepted networks for making payments. This explains why Visa has very good levels of profitability and despite higher competition in the payments sector, its business margin has been quite stable over the past four years.

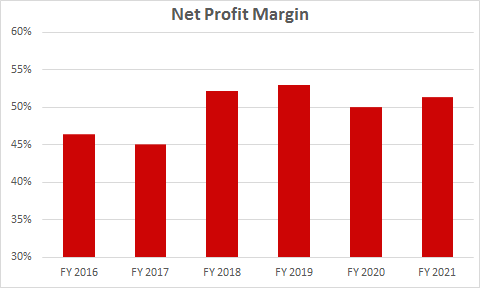

Indeed, its net profit margin has been quite good over recent years, ranging from 45%-53% over the past six fiscal years. This is also higher than its closest competitorMasterCard(MA), which had a net profit margin of 42% in 2020. This superior profitability is only possible because Visa has some competitive advantages over its peers, namely a strong network effect and brand awareness that is difficult to challenge.

This strong position is also visible on client incentives, which are lower for Visa compared to MasterCard. These client incentives are paid by Visa and MasterCard to financial institutions that issue credit and debit cards, merchants, and other partners, as a way to grow payments volume and increase the networks acceptance. For consumers, these are usually seen as 'rewards' for using credit cards, which can be funded in part by the network's payments to the credit card companies.

Paying lower client incentives is also a sign that Visa has an advantage over its competitors, which makes sense because it is the most widely used network and therefore has less need to pay for volumes.

This shows that Visa has a leading position in the 'physical' payments area, but over recent years the growth of online payments has been quite strong and this is a space where Visa faces more competition and its position is not as strong.

While debit and credit cards are usually the best alternative to cash or check payments in physical stores, for online purchases there are other alternatives to processing payments, namelyPayPal(PYPL) that is nowadays a leading company in this field.

Indeed, PayPal has grown more rapidly than Visa over recent years, showing that its business is more adapted to the digital economy while Visa is still much exposed to physical payments. This explains why PayPal generated revenues of about $10 billion in 2016 (vs. $15 billion for Visa in the same year), while in 2021 PayPal's revenues were $25 billion, compared to Visa's $24.1 billion revenues in fiscal year 2021.

While Visa and MasterCard are still dominant in the physical payment market that merchants cannot avoid to use their networks, even though competition from PayPal orBlock(SQ) is increasing in in-store payments, in online payments there are more alternatives and the recent rise of buy now, pay later (BNPL) options is another threat to Visa's position in the digital payments industry.

A growing segment in the digital payments/fintech industry is BNPL, a payment solution that lets consumers break up their purchases into installment payments, without racking up interest or fees. The popularity of BNPL has increased a lot in the past couple of years, boosted by the pandemic, especially among younger generations that are less willing to use credit cards for online purchases.

This happens because BNPL is often much cheaper than putting large purchases on a credit card. Most credit card companies and banks charge very high interest rates that can be 20% or even higher, while on the other hand, most BNPL options don't charge any interest as long consumers adhere to the payment schedule. Usually, payments are done in three or four installments, over a short period of time that usually is no longer than 3-6 months.

BNPL is mostly used for online shopping and its rising popularity is only expected to continue over the next few years, as many BNPL companies have established partnerships with retailers in recent months, including the giant player in this field that isAmazon.com(AMZN). For instance,Affirm(AFRM) has reached an agreement a few months ago to be Amazon's exclusive BNPL partner in the U.S., allowing consumers to have more options on how to pay at the checkout.

As more consumers sidestep credit cards for online shopping, Visa is poised to lose importance in the payments options, which may be a reason why Amazon has threatened to drop Visa cards in the U.K. Even though this would not be a major blow to Visa's revenues or earnings, the most important question that investors should make is how a retailer can stop accepting Visa and not lose significant sales, and if this is a sign that Visa is losing its moat.

Amazon Dispute

A couple of months ago, Amazonannouncedthat it would no longer accept U.K.-issued Visa credit cards, beginning next January. Moreover, the company also said that it was considering dropping Visa as a partner for co-branded cards in the U.S. due to the high fees that Visa is charging on both cases. Note that in the U.K., MasterCard is Amazon's partner for its co-branded cards, thus the relationship with Visa in the U.K. is only as a payment method.

Even though Amazon decided to not go ahead with this decision close to the date when it was expected to enter into effect, what is more important is how a company can consider dropping Visa as a payment choice and not be afraid of losing much sales due to this decision. In my opinion, this would be inconceivable five or ten years ago, showing that the digital payments landscape has changed considerably in recent years.

While in the past a credit card was almost indispensable to shop online, nowadays there are other payment options and dropping Visa would certainly have a limited impact on Amazon's sales in the country. Beyond that, this is also a strategy for Visa to lower its fees, as Amazon is a very large retailer with a global presence and as pricing power over payment suppliers.

This can be seen on Amazon's recent agreement with PayPal to accept Venmo payments in the U.S., which PayPal said that would be positive for volumes growth, but not in the same way for revenue growth, as fees are lower than average in this agreement. This happens because Amazon has bargaining power, and is doing the same thing with Visa, targeting particularly international markets where its operating margin is close to breakeven and lower fees to payment networks can have a significant impact on its business profitability. Indeed, prior to this dispute in the U.K., Amazon had moved to limit transactions processed by Visa in Singapore and Australia, offering credits to customers who used an alternative payment method.

This shows that Amazon clearly has a strategy to push for alternative payment methods rather than Visa, a 'battle' that may extend to its most important market (the U.S.) in the next few months. But if Amazon would stop accepting Visa cards in the U.K., would customers have enough alternatives and still shop on its website?

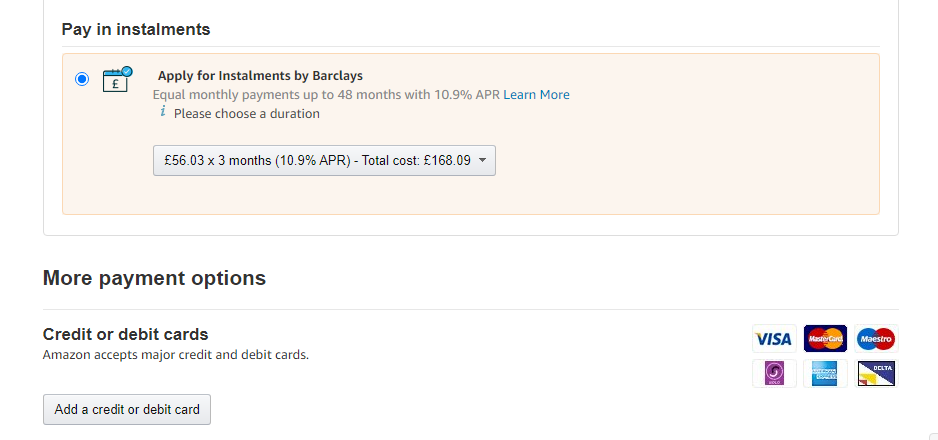

As I'm Portuguese, and there isn't a local website, I have an account on Amazon UK, so I decided to check which payment options are available at checkout. As you can see in the next image, Amazon first highlights payment in installments, and only next it has credit and debit cards including Visa, MasterCard orAmerican Express(AXP).

This shows that Amazon is pushing consumers to choose payments in installments rather than using cards, probably because it has lower costs for the retailer and is a good way to boost operating margins. When choosing installments, consumers have three options as seen below and none of them relies on Visa, a strategy that Amazon is also pushing for in the U.S. by partnering with competitors like Affirm or PayPal.

This strategy is obviously bad for Visa, as its relationship with Amazon is clearly threatened as consumers have more alternatives and Amazon can more easily drop Visa as a payment option, or at least put pressure for Visa to lower its fees if it wants to remain as payment method on Amazon's websites. I think this possibility would be almost inconceivable a few years ago, showing that Visa's moat is clearly not so strong today as it was in the recent past and investors should increasingly question if Visa still has a competitive advantage in the digital payments industry. I think in physical stores Visa, and MasterCard, still has an edge over fintech companies, but in online payments its position is clearly not so strong and increasing competition is making it 'just' another payment option.

Visa's Recent Earnings

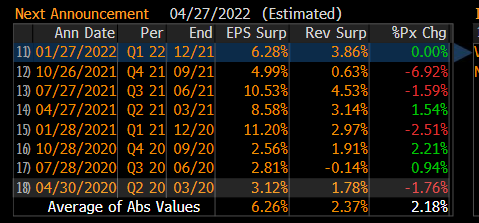

Visareporteda couple of weeks ago its results related to the first quarter of fiscal year 2022, beating estimates on both the top and bottom-lines, as can be seen in the next graph. Its EPS was 6% above expectations and revenue was close to 4% above estimates.

Regarding its financial figures, Visa's revenues in the last quarter (ended December 2021 - first quarter of fiscal year 2022) amounted to $7.06 billion (vs. $6.79 billion expected), up 24% YoY, while its non-GAAP EPS was $1.81 vs. $1.70 expected.

These positive results are justified by higher payment volumes, which increased by 20% YoY, with cross-border volume up 40% and processed transactions up 21%. Note that cross-border volume is mainly related to travel and has been the main headwind for Visa's revenue growth during the pandemic, even though it is the company with less exposure to cross-border volumes compared to its competitors MasterCard and American Express.

Strong cross-border volumes are a very positive signal for revenue growth over the coming quarters, especially considering that a new variant (Omicron) appeared during this last quarter. This is a strong signal that the pandemic is gradually progressing to an endemic disease, and further disruptions like happened in 2020 to travel aren't likely.

Despite strong revenue growth in Q1, operating expenses also increased by 24% YoY, thus margins were flat in the quarter. However, this includes a litigation provision of $148 million that is non-recurring, without this item Visa's total operating expenses increased by 16% YoY.

Regarding its cash flow generation, it remained very strong in the last quarter given that free cash flow (FCF) was above $4 billion. Its balance sheet is very strong with a net debt position of less than $3 billion, which leads to a net debt-to-EBITDA ratio of about 0.2x.

This is a very low level of financial leverage and enables Visa to return capital to shareholders, above its own FCF generation capacity. Indeed, Visa returned $4.9 billion in the quarter to shareholders, in the form of dividends and share buybacks. This is a higher amount than FCF, but it is not an issue because Visa's financial profile is very strong and therefore is likely to maintain this shareholder remuneration policy over the coming quarters.

Its guidance for the next quarter was revised upwards, and Visa now expects revenue to climb by a percentage at the high of high teen's range, while operating expenses could jump by a percentage in the high end of mid-teens range.

Conclusion

Visa has a strong position in the global digital payments industry, but as shown by the recent dispute with Amazon, its moat is increasingly questionable, at least for online shopping. It has a stronger position with physical stores, which is positive on a cyclical perspective as cross-border volumes are expected to recover from the pandemic-driven drop, which is positive for earnings growth over the coming quarters.

Regarding itsvaluation, Visa is currently trading at 29x its forward earnings, below its historical average over the past couple of years (close to 33x forward earnings). However, this valuation profile is similar to MasterCard, which is also trading below its historical valuation multiple, while its competitor has a higher exposure to cyclical cross-border volumes.

Even though Visa and MasterCard have a similar business profile, MasterCard seems to be a better investment right now from a perspective to play the cyclical rebound of cross-border volumes. While previously I preferred Visa as a long-term play due to its moat in the industry, the digital payments industry is changing rapidly and barriers to entry are relatively low, which may impact Visa's business over the long term and make it 'just' another payment option over the coming years.

Comments