- Upstart initially guided for $500 million of revenues in 2021. It delivered $849 million.

- The company is profitable and has projected strong growth for 2022.

- The company also announced a $400 million share repurchase program, highly unusual for a high-growth company.

- Many investors think share repurchases are bad for growth. I explain why that is wrong.

- I rate UPST stock a strong buy as one of my higher conviction ideas.

$Upstart Holdings, Inc.(UPST)$ delivered a strong close to the 2021 year and announced something surprising for high-growth companies: a share repurchase program. Growth investors often disdain share repurchases, but I explain why those feelings are misplaced. I also discuss why UPST is repurchasing shares, and what it means for investors. UPST is set to continue its rapid growth rates into 2022 and beyond and is already quite profitable. I rate shares a strong buy as this is one of my higher conviction positions coming out of the tech crash.

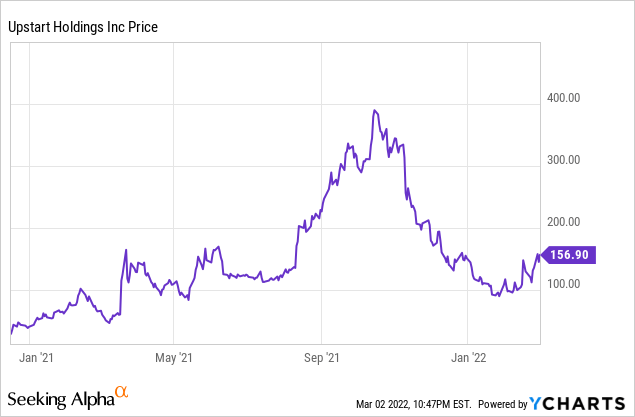

UPST Stock Price

UPST came public in December 2020 at a price of $20 per share. Since then, the stock has had a rollercoaster of a ride, trading as high as $401 and experiencing many 50% drawdowns in just a few years span:

Now trading around $150 per share, the stock is one of my higher conviction ideas amidst the crash in tech stocks.

UPST Stock Key Metrics

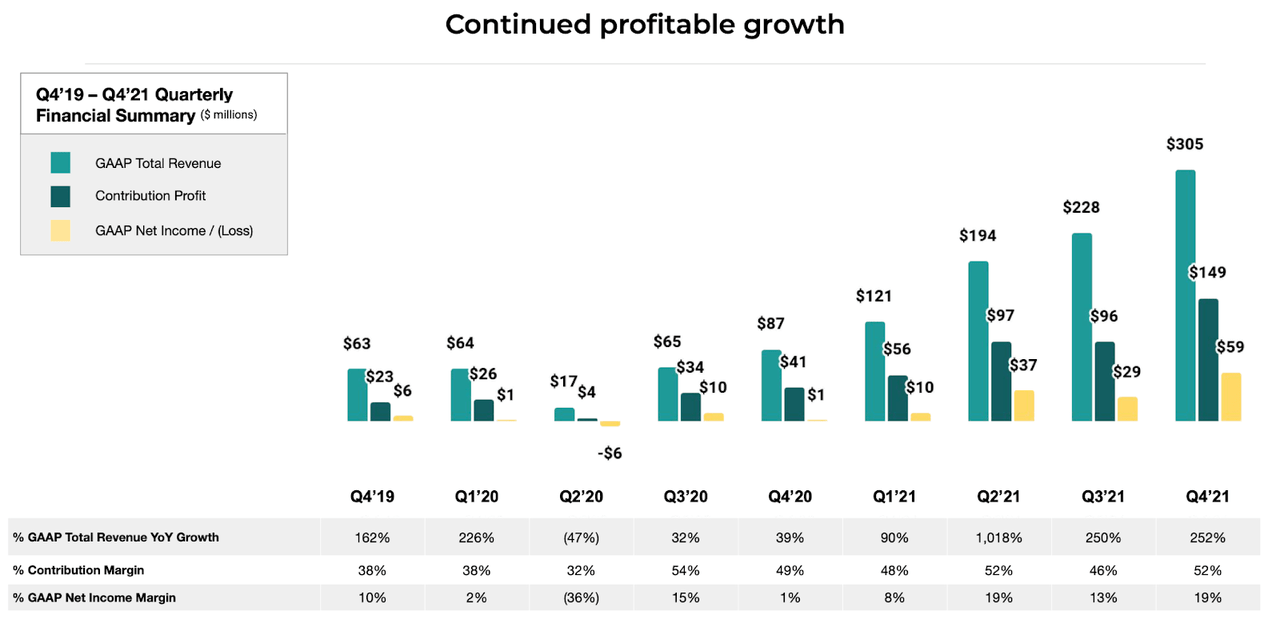

The latest quarter showed more of the strong strength that UPST shareholders have become accustomed to. UPST reported $305 million of revenue - far outpacing its guidance of $265 million. Net income was also strong at a 19% net margin:

That brings its 2021 revenue to $849 million. The company had guided for $500 million before starting the year!

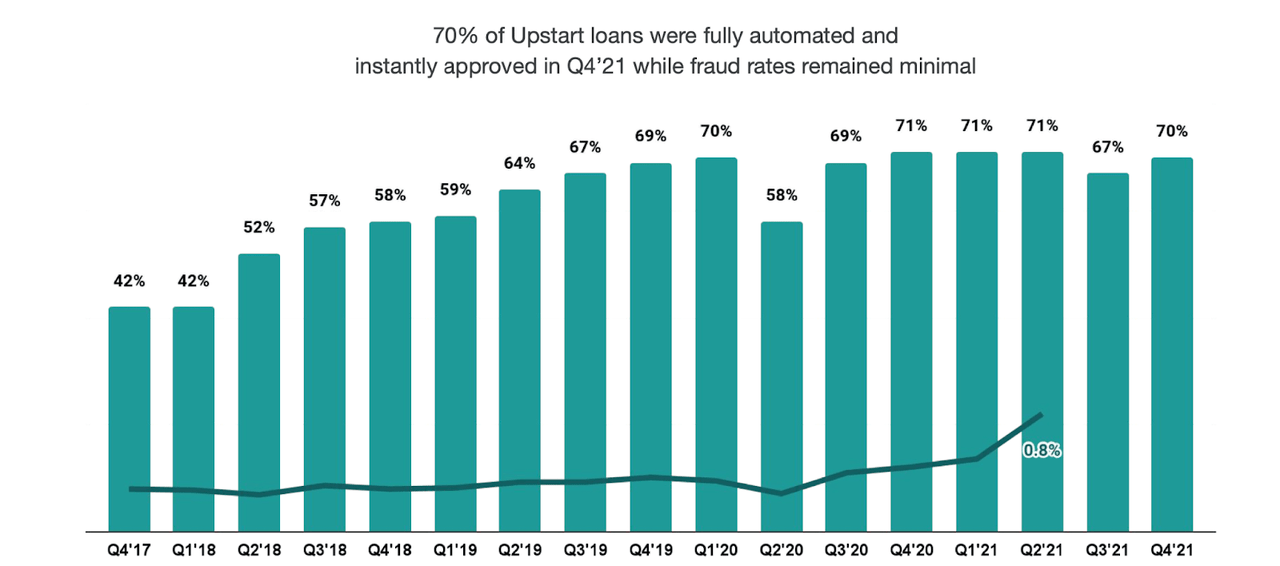

UPST saw automated loans return to the 70% level - this metric should continue to improve moving forward as the company perfects its algorithms.

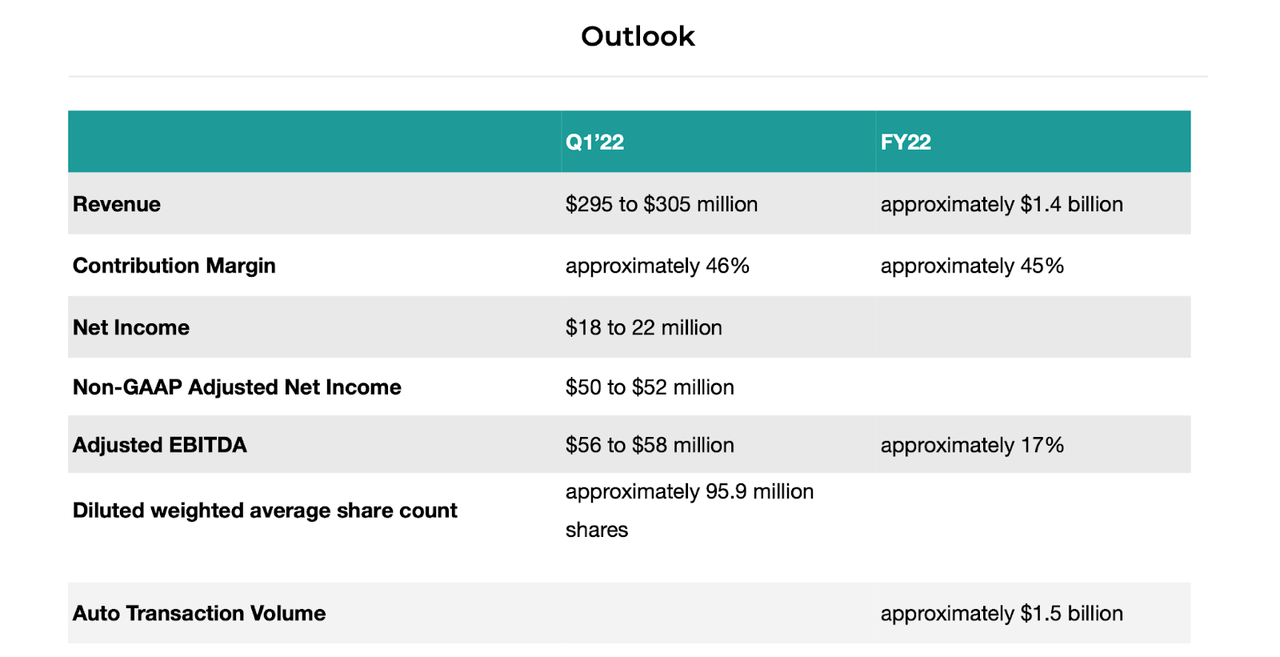

UPST guided for the next year to see around $1.4 billion in revenue, representing 65% year over year growth.

Why Is Upstart Repurchasing Shares?

In addition to the strong results and guidance, UPST initiated a $400 million share repurchase program. Why is UPST repurchasing shares?

From their earnings call, UPST stated the following:

I want to highlight as a final note that we recently announced the authorization from our Board of Directors to repurchase up to $400 million of Upstart shares. With the volatility in the trading of our stock, we have seen what we believe to be attractive buying conditions at various times over the past year, and our profitability puts us in a position to be able to initiate this program and take advantage of those situations on behalf of our shareholders.

Yeah, I would say, importantly, we have not run out of things to do by any stretch. As you know, we're growing quickly and hiring a lot. So this isn't a capital structuring decision, it's economic opportunism. And it's really a function of two things that are somewhat unique at our stage. First of all, well, one of them is the volatility of our stock is well known. You've seen it over the past year. And look, there's -- we have a conviction that there's just been numerous instances over the past year, we're knowing what we know about our business and our opportunity. We are of the opinion that it's been undervalued.

And then the second component is we are actually profitable, so because of that it's very unique feature, we have the actual ability to take advantage of that conviction on behalf of our shareholders. So it is opportunistic, and I think that the volatility in our stock continues, we'll watch it, and we'll be in a position to take advantage of that aspect. But it's not really a conviction around returning capital to shareholders as much as it is taking advantage of the volatility of the stock and the profitability we have as a business model already.

In summary, UPST is repurchasing shares to take advantage of opportunistic volatility. Management believes that the stock is undervalued on account of the high growth rate and profitability.

Is The Share Repurchase Good For Investors?

The share repurchase is the icing on the cake of a very good quarter, but we must discuss if share repurchases are good and whether they are good for UPST investors.

Let's start with share repurchases in general. I have seen it written that share repurchases impede growth prospects and thus growth stocks should not buy back stock. This notion is unfortunately popular and is not true.

Share repurchases are typically funded with free cash flow or net income. This is very important to note. The most important way companies fund growth is through increasing operating expenses - for tech companies like UPST, this will show up primarily through increased research & development (R&D) expenses. In the case of UPST, "engineering and product development" expenses increased 244% in 2021. Net income and free cash flow are what the company earns after all operating expenses, including any investments in growth. As a result, using net income to buy back stock will not inherently impede growth. This is an important accounting distinction, and one worth re-reading if it doesn't yet make sense.

Another less important way to fund growth is through acquisitions or capital expenditures. In this case, the cash will come out of net income or free cash flow. If the company uses all free cash flow to repurchase stock, then they will have less capital available for acquisitions and capital expenditures. In this case, there is some truth to the notion that share repurchases can be at conflict with growth. However, most tech companies do not have meaningful capital expenditure opportunities (cloud computing companies are a notable exception), and there is high execution risk in acquisitions. Whether a company should use free cash flow to repurchase shares or externally acquire depends on the projected return of either method. Share repurchases offer a more certain ROI than external acquisitions, making them arguably preferable much of the time. In this case, the main reason to avoid share repurchases and prefer external acquisitions would be if the stock in question was substantially overvalued relative to investible alternatives. In the case of UPST, I view the stock to be substantially undervalued in its own right, making share repurchases appear quite justified.

From Julian Lin

Comments