$Exxon Mobil(XOM)$ and $Chevron(CVX)$ are two of the most recognizable names in the oil and gas industry that currently suit momentum-type investors well.

Year-to-date, these two oil giants have seen very favorable price action, and each of their market valuations has increased quite significantly. Let’s take a closer look at CVX and XOM to get a clearer view of why these oil suppliers could be good options for momentum investors, comparing some key financial metrics with earning reports data.

CVX

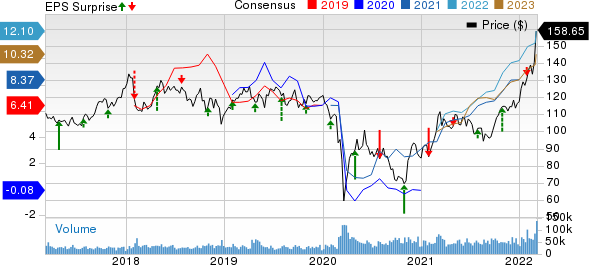

Chevron’s current market cap is around $305 billion and year-to-date, the oil giant is up nearly 35% to a price of $160 per share. The company trades at a beta of 1.13 and has consistently been hitting all-time highs in 2022. Dating back to July 2020, CVX has posted mixed earnings results. In the last seven reports, CVX has missed estimates four times and beaten estimates three times, and in its most recent earnings report, CVX missed the $3.11 estimate by nearly 18%, or $0.55.

Analysts are forecasting that CVX will reward investors nicely over the next two years. Over the last 60 days, consensus estimate trends for FY22 and FY23 have both seen favorable increases. For FY22, the consensus estimate trend is up 22.4%, or $2.21, to $12.10 per share. For FY23, the trend has risen nearly 27%, or $2.17, to $10.32 per share.

Currently, CVX’s top line is forecasted to grow 10.8% for fiscal 2022 and net income has a projected growth rate of 34% year-over-year. Looking further ahead, CVX is expected to grow its bottom line by roughly 10% over the next three to five years.

CVX’s current free cash flow sits at $21.1 billion, the highest it’s been in five years, and is 110% higher than its median of $10 billion. The company’s free cash flow has increased by roughly 1200% since a low point of $1.6 billion last December.

The oil giant produces billions in liquids per day, a critical component driving the success of its business. In its January report, it had a 3% positive surprise on net liquids produced per day, increasing the metric to around 1.8 billion and beating estimates of 1.7 billion. CVX is currently ranked sixth out of 49 in its industry, with revenues of nearly $163 billion over the last twelve months. The company has a Value Style Score of D, a Growth Style Score of B, and a Momentum Style Score of A. Its overall VGM Score is a B and is a Zacks Rank #1 (Strong Buy).

Year-to-date, Exxon Mobil’s share price has increased nearly 42% and is trading at around $85 per share, 25% off its all-time-high share price of $105. XOM sits on a higher $363 billion market cap and has a beta of 1.16.

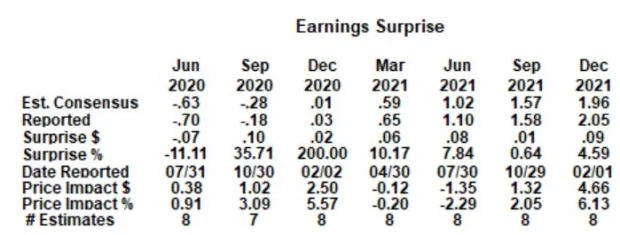

XOM has consistently beat earnings estimates dating back to July 2020; out of the last seven reports, six have been positive surprises. The average earnings surprise for the oil giant over its last four reports is 5.81%, and in February, the company posted an earnings beat of roughly 4.6%, or $0.09 per share, with its bottom line coming in at $2.05 per share.

Additionally, XOM has consistently beaten sales estimates in its earnings reports. In its most recent quarter, Exxon beat sales estimates by 3.1%, or $2.5 billion. Revenue for FY22 has been projected to grow by 11%, while net income is expected to see a 21% increase. For the next three to five years, XOM is expecting to see its bottom line grow by 18%.

The company’s current free cash flow comes in at approximately $36 billion, up about 160% off its median of $13.9 billion over the last five years and up 1200% from a negative cash flow value of $3.3 billion back in October 2020.

XOM’s $286 billion in revenue over the last twelve months is enough to set it higher than CVX at number three in the industry out of 49. Exxon Mobil currently has a Value Style Score of C, a Growth Style Score of A, and a Momentum Style Score of A. Its overall VGM Score is an A and is a Zacks Rank #1 (Strong Buy).

Similar to Chevron, XOM’s major factor driving its level of success is crude oil prices. With the price of crude oil surging, XOM and CVX stand to greatly benefit during this time and provide ample opportunity for momentum investors.

Exxon Mobil has displayed greater strength within the recent earnings reports, beating estimates consistently. Meanwhile, CVX has struggled to do the same and has posted mixed earnings results.

Exxon Mobil beats Chevron in expected EPS growth over the next three to five years, free cash flow, and ranks higher within the industry with a much higher revenue over the last twelve months.

Both names provide excellent exposure for momentum investors, but due to these metrics, I currently believe that XOM would be a better buy over CVX.

Comments