Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Singapore Airlines Limited$SINGAPORE AIRLINES LTD(C6L.SI)$ does use debt in its business. But should shareholders be worried about its use of debt?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

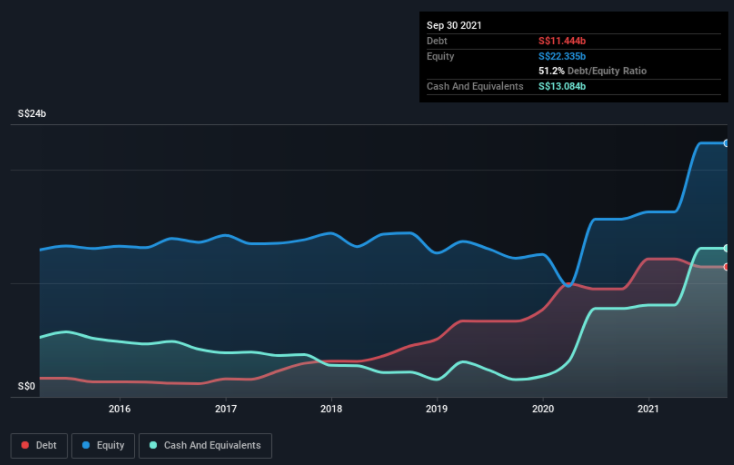

According to the last reported balance sheet, Singapore Airlines had liabilities of S$5.67b due within 12 months, and liabilities of S$16.4b due beyond 12 months. Offsetting these obligations, it had cash of S$13.1b as well as receivables valued at S$1.19b due within 12 months. So its liabilities total S$7.76b more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Singapore Airlines is worth a massive S$14.7b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. While it does have liabilities worth noting, Singapore Airlines also has more cash than debt, so we're pretty confident it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Singapore Airlines's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out thisfreereport showing analyst profit forecasts.

In the last year Singapore Airlines had a loss before interest and tax, and actually shrunk its revenue by 46%, to S$5.0b. To be frank that doesn't bode well.

By their very nature companies that are losing money are more risky than those with a long history of profitability. And in the last year Singapore Airlines had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through S$3.5b of cash and made a loss of S$1.6b. With only S$1.64b on the balance sheet, it would appear that its going to need to raise capital again soon. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. For riskier companies like Singapore Airlines I always like to keep an eye on whether insiders are buying or selling.

Comments