Under the background of continuous recovery of travel and tourism, Uber & Lyft, two travel giants, have successively announced Q4 financial reports.Relying on scale effect, $优步(UBER)$ achieved sustained revenue growth, active consumers and profits, and rose by more than 5% before the market.$Lyft, Inc.(LYFT)$ is inferior to Uber, the monthly active passengers decreased month-on-month, but the annual adjusted profit was positive for the first time. Both are emerging from the haze during the epidemic.

Uber has experienced the impact of epidemic and regulatory storm in the past two years. Since the second half of 2021, everything is back on track. Q4 earnings show a strong recovery trend. The Mobility and Delivery business are driven by dual cores, and the scale is expanding steadily. At the same time, the improvement of profit seems to make the market feel better.

Active consumers hit a record high,Mobility Business is Close to the pre-epidemic levels

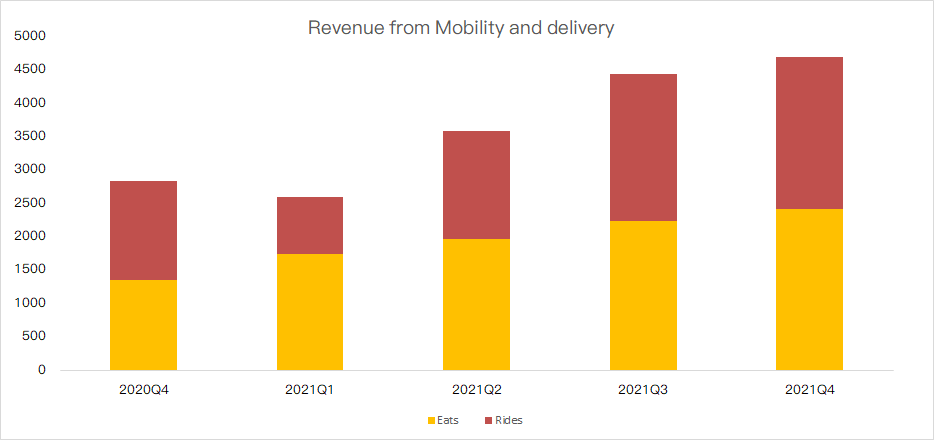

1) Q4 monthly active platform consumers(MAPC) increased by 27% year-on-year to 118 million, and the number of trips increased by 23% year-on-year to 1.77 billion, with an average of about 19 million trips per day.The total order amount increased by 51% to US $25.9 billion, and the revenue from Mobility and Delivery was half and half.

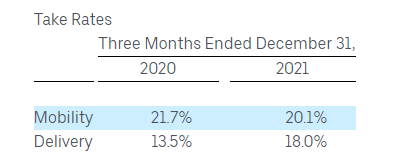

2) Among them, the take-out business contributed 13.4 billion dollars (+34% yoy). After the epedemic, Uber increased its investment in grocery distribution, which partially made up for the loss of the mobility business. Now, Uber's take-out business has gained a firm foothold in the competition with DoorDash, and the take-rate has greatly increased from 13.4% to 18%. The take-out business is becoming an important support for the company's medium-term growth.

3) The recovery degree of the network car business was better than expected, and the take-rate was 20.1%, which decreased year-on-year and month-on-month. Omicron and labor shortage are the two major tests of the current mobility business. This quarter, the department contributed 11.3 billion (+67% yoy), which basically recovered to the level of 2020Q1.

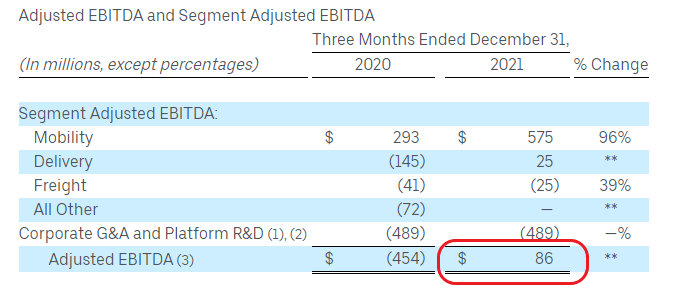

Adjusted EBITDA turned positive again after Q3

Uber's profitability has always been criticized. In recent quarters, the management has obviously begun to focus on improving the profitability of its core business, paying more attention to efficiency and cost control in user experience and marketing strategy. UbersQ3 and Q4 have achieved positive EBITDA.

- Uber One was officially launched in the United States in November. The membership fee is $9.99 per month, and members can enjoy discounts, specials, priority services and exclusive discounts on rides, delivery and grocery stores.

- The incentive measures continued unabated, and Take-Rate decreased from 21.1% in Q3 to 20% in Q4. In this quarter, the total revenue of drivers and distributors was 9.5 billion US dollars, up 56% year-on-year, which was faster than the growth rate of total orders (51%).

- In addition, Uber also holds 11.9% of Didi and 14% of Grab.At the end of the quarter, Uber has cash and short-term investment of 5.295 billion US dollars, which has good financial flexibility.

Positive Guidance, Omicron's influence is limited

Omicron's impact on passenger traffic is mainly reflected in the first quarter, but the management description is optimistic: Omicron began to affect the company's business in late December, but the taxi business has started to rebound, and the total order volume in the latest week increased by 25% month-on-month. For 2022Q1, it is estimated that the total order amount will be between 25 billion and 26 billion US dollars, and the adjusted EBITDA1-130 million US dollars.

Lyft, another travel giant, seems to pay more attention to the present, and some growth uncertainties are beginning to be exposed.

Although LyftQ4 revenueIt exceeded expectations and achieved adjusted full-year profit for the first time. However, the MAPC(monthly active platform consumers) declined month-on-month, which caused the market to worry about the development prospects, and the gap between the overall user volume and revenue scale and Uber also widened.

Lyft's business is relatively simple, and its main sources of income are service fees and commissions. In addition, Lyft also rents bicycles and scooters, and provides institutions with shared access to the market.

Since the second quarter of this year, Lyft's revenue has resumed positive growth, Q4 revenue has increased by 70% year-on-year, and travel business has basically recovered to the pre-epidemic level. In 2021, the total revenue increased by 36% year-on-year, close to the revenue scale in 2019.

In addition, lyft achieved adjusted full-year profit for the first time. During the epidemic, Lyft reduced costs and expenses by laying off employees and cutting budgets, and divested some assets related to autonomous driving, helping the company survive the most difficult period.

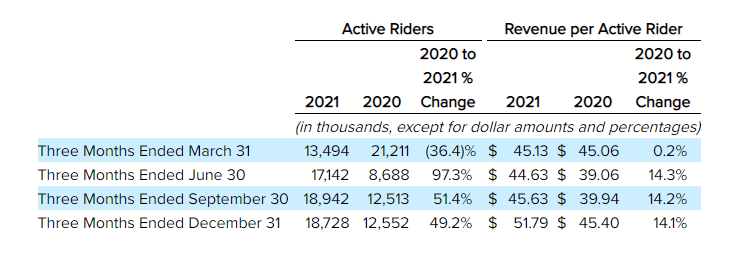

However, the disadvantages of cost reduction are gradually revealed: revenue slows down and active consumers are lost. The number of active passengers in the quarter was about 18.72 million, down from 20 million expected by analysts and down from 18.94 million in the previous quarter. The weakness of this key indicator disappointed the market.

A very important reason is the shortage of labor. Under the high inflation environment and odd-job economy, the lack of welfare and low wages make drivers leave the online car jobs one after another, and Lyft has to invest more fees as bonuses to retain and motivate drivers. On the other hand, lyft is also raising the service price to balance this part of the cost. According to the financial report, the income of each active driver reached $51.79 this quarter, a record high. The impact of driver shortage and rising incentive cost on smaller Lyft will be more obvious.

Comments

[Like]