$AMD(AMD)$$Micron Technology(MU)$

KEY POINTS

- Micron Technology stock has been outperforming Advanced Micro Devices so far in 2022.

- Though AMD is growing at a fast pace, its rich valuation has turned out to be a headwind in light of the Fed's hawkish stance.

- Micron's cheap valuation and decent growth could act as tailwinds in 2022.

There is a clear winner if you are looking to add one of these two tech stocks to your portfolio.

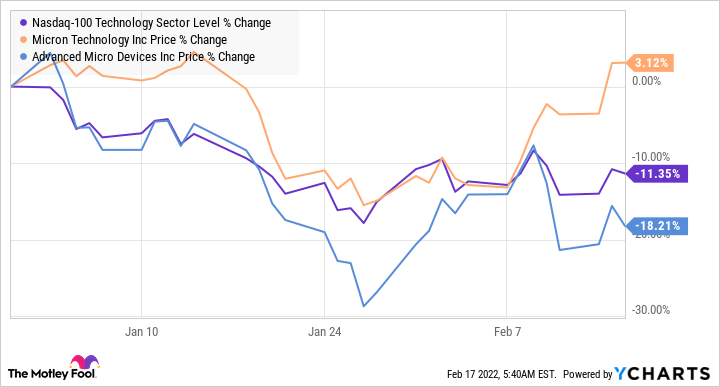

Shares ofAdvanced Micro Devices(AMD)andMicron Technology(MU)have enjoyed contrasting fortunes on the stock market so far in 2022.

While Micron Technology has held its ground despite the broader sell-off in tech stocks, AMD has been hammered badly. What's surprising is that investor confidence in AMD stock hasn't improved despite the company posting solid fourth-quarter 2021 results on Feb. 1 thatblew past Wall Street's expectations.

Micron, on the other hand, has started gaining investor confidence since it became clear that the demand for memory chips will be strong enough tosupport robust pricing.

Investors have sold off AMD stock this year due to factors out of the company's control. The Federal Reserve is expected to hike interest rates as many as seven times this year, according toGoldman Sachs. The investment bank was originally expecting the Fed to hike rates five times this year, but it now sees two additional hikes to control surging inflation.

This does not bode well for richly valued stocks such as AMD, whose fast pace of growth may be hampered by an increase in borrowing costs on account of higher interest rates. As a result, investors seem to be in panic mode, and have sold off shares of AMD in 2022, opting for safer options such as Treasury bonds where they canget higher yieldsin light of the Fed's hawkish policy.

However, investors should not forget that AMD's chips are being used in several fast-growing end markets that should help the company sustain its outstanding growth in the long run. The data center market, for instance, is one of AMD's fastest-growing markets thanks to the terrific demand for its server processors and graphics processing units (GPUs).

CEO Lisa Su said on the company's Februaryearnings conference callthat AMD's data center revenue more than doubled in 2021. Sales of data center chips accounted for "a mid-20 percentage" of AMD's annual revenue last year, according to Su, and she believes that 2022 could be another year of significant growth for the data center business.

That's not surprising, as demand for AMD's Instinct data center accelerators is on the rise to support high-performance computing (HPC) applications. More importantly, the demand for data center accelerators is expected to increase at an annual pace of 43.8% through 2027 to $53 billion, according to a third-party estimate, which bodes well for AMD given its rising influence in this space.

The adoption of AMD's data center processors has shot up impressively of late. The number of supercomputers powered by its EPYC server processors tripled year over year in November 2021, and the company's chips are now powering eight of the top 10 most efficient supercomputers in the world.

On the other hand, AMD's market share gains in client CPUs andthe enormous potentialin the gaming console market are going to be additional catalysts for the company. All of this explains why AMD aims to deliver 31% revenue growth this year, while analysts are forecasting a 43% jump in earnings thanks to margin improvements. Such impressive growth could help AMD put behind its disappointing start to the year and send the stock higher.

Micron Technology's cheap valuation, fast-growing revenue and earnings, and bright long-term prospects have helped the stock beat the broad market sell-off so far this year. The company's revenue shot up 33% year over year to $7.69 billion in the first quarter of fiscal 2022 that ended on Dec. 2, 2021, along with a 177% increase in earnings per share to $2.16.

Analysts expect Micron to post 16% top-line growth this fiscal year, followed by a 20% increase in fiscal 2023. Even better, the company's earnings are expected to clock annual growth of 24% for the next five years. Micron is in a solid position to clock such impressive growth thanks to its growing share of the memory market.

Memory market research provider TrendForce estimates that Micron's share of the DRAM (dynamic random access memory) market increased by four percentage points to 25% in the third quarter of 2021. Micron's growing influence in the DRAM space is good news for the company, as this market is set for secular growth thanks to multiple catalysts.

Smartphones, for instance, have opened a huge volume opportunity for Micron thanks to the advent of 5G wireless networks. The chipmaker points out that 5G smartphones are using 50% more DRAM over 4G devices, and their shipments are expected to increase to 700 million units this year from 500 million in 2021.

Meanwhile, the addition of autonomous driving functions to self-driving cars is another factor that's boosting Micron's addressable market. The memory specialist points out that electric vehicles with level 3 autonomous driving capability are sporting 140 gigabytes of DRAM this year. This explains the 25% year-over-year growth in Micron's automotive revenue last quarter, and points toward a huge opportunity for the chipmaker as the adoption of autonomous vehicles increases.

So the growth in memory demand from multiple end markets should be a long-term tailwind for Micron Technology that should help this semiconductor play deliver robust upside.

The verdict

AMD is expected to grow at a faster pace than Micron, but the former's valuation is a disadvantage right now. AMD is trading at 47 times trailing earnings, compared to Micron's multiple of just 15. Micron's price-to-sales ratio of 3.7 is also lower than AMD's multiple of 9.

This explains why shares of Micron haven't been battered as badly as AMD. Micron's cheap valuation and decent growth make it an ideal pick for investors looking for a value play. Additionally, the probability of the Fed hiking rates several times this year could be a headwind for richly valued stocks such as AMD, making Micron Technology the better pick of these twotechnology stocksright now.

Comments

Should you buy AMD ?