Summary

- Alibaba undoubtedly suffered severe profit speed bumps in recent past years.

- However, it coped with these challenges successfully in my view, and I see even better days lie ahead now due to several immediate catalysts.

- Regulatory pressure and COVID restrictions are abating.

- Thanks to a humongous cash position and strong cash flow, I see the company well-positioned to resume growth once the macroeconomic parameters improve.

- Yet, its P/E is only in the single-digit range once the cash position is adjusted, simply unjustifiable in my view.

Investment thesis

- I now see a potential thawing of relations between Chinese regulatory authorities and big technology firms. In recent years, regulators have taken a hard stance onChinese tech companies but, given the struggling domestic economy and the impacts created by the COVID pandemic, I see signs that the authorities are now more focused on returning the country to growth mode. For example, Ant Group recently received a regulatory greenlight for raising $1.5 billion in capital to further expand its consumer business.

- Moreover, COVID-19-related headwinds should start to abate, thereby supporting a healthier economic backdrop and improved consumer spending. Even amid the COVID challenges, according to Toby Xu, the CFO of BABA, the company's profit growth has been strong due to its efforts to improve operating efficiency and cost optimization in the past. In the meantime, BABA's net cash position remains healthy (more on this later) and I see the company well-poised to resume strong cash flow growth once the macroeconomic environment improves.

Alibaba$Alibaba(BABA)$ recently released its 2022 December quarter earnings. In my view, the December quarter and also TTM 2022 earnings are quite solid, especially when the challenges were considered. As commented by Daniel Zhang, Chairman and CEO of BABA, "We delivereda solid quarter despite softer demand, supply chain and logistics disruptions due to the impact of changes in COVID-19 measures."

In the remainder of this article, I will examine its profitability, capital allocation flexibility, and also valuation to better support the above thesis.

Profitability remains strong even amid the COVID

Alibaba undoubtedly suffered severe profit headwinds in the past few years due to a range of factors including the aforementioned regulatory tightening, elevated operating costs, and softened consumer demand due to COVID, as you can see clearly from the following two charts.

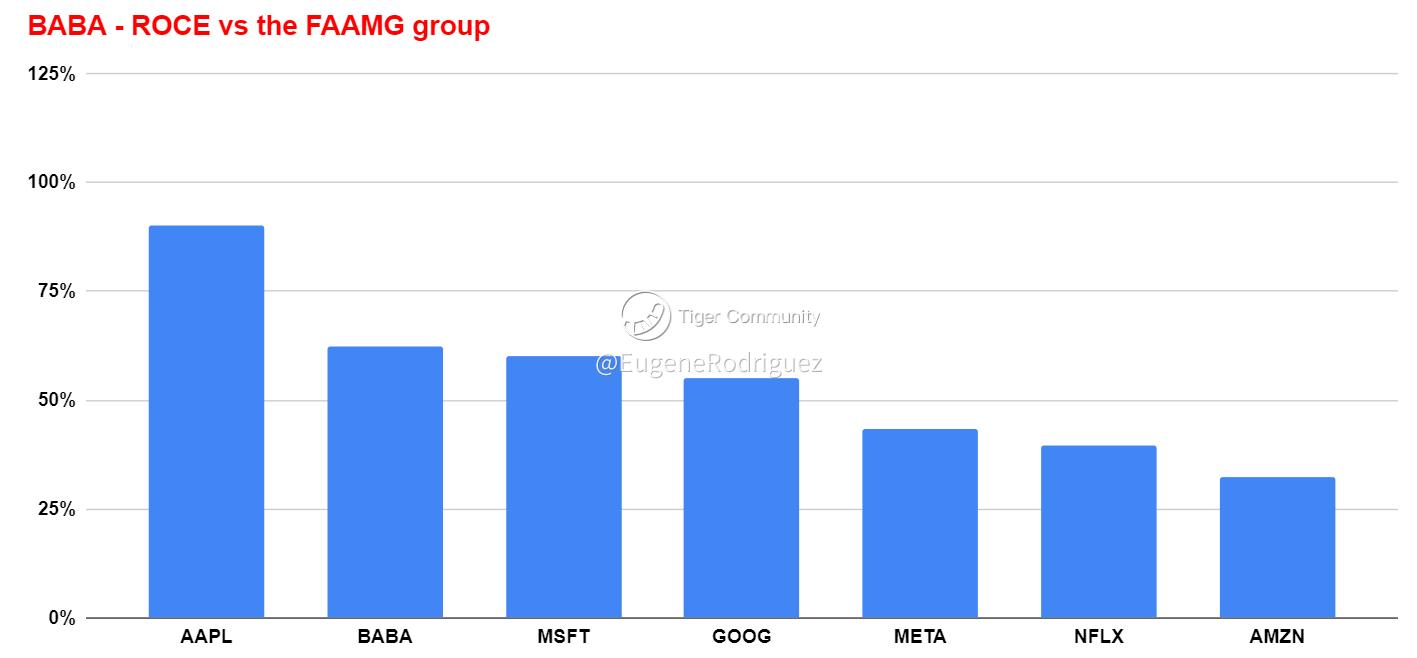

The first chart shows its return on capital employed ("ROCE") in recent years, highlighting the year 2022. As seen, the company's profitability has suffered significantly, and its ROCE retreated from almost 97% in Q1 of 2022 to about 64% based on TTM 2022 financial results. The second chart, taken from its December earnings report ("ER"), shows its operating margin falling to a meager 3% by the end of 2021.

Nonetheless, BABA's profitability remained robust enough amid these strong headwinds, and now I see signs that the trend is turning. As shown in the next chart below, its current ROCE of 64% is on par with the FAAMG group. Furthermore, its profit margins have drastically improved in the past year. As shown in the chart above, its operating margin has improved from 3% as reported in its December 2021 quarter year to 14% during the most recent reporting period. In the meantime, the adjusted EBITDA margin also expanded from 21% in December 2021 to 24% in the most recent reporting period.

Next, I will argue that thanks to its strong net cash position, the company is well-poised to resume full speed growth once the macroeconomic environment improves.

Capital allocation remains highly flexible

Capital allocation remains highly flexible

BABA has historically always maintained a strong financial position. However, its financial position has been weakened to some degree due to its commitment to the Chinese common prosperity funds, high tax rates, fines, and regulatory changes. To wit, its $15.5B pledge to the common prosperity fund over the next five years translates to a commitment of $3.1B per year. Despite all these, for the nine months ended December 31, 2022 (see the next chart below), it reported an operating cash flow totaling $24.4B, putting a better context for the above commitment (and also its cash obligations for investing and financing obligations).

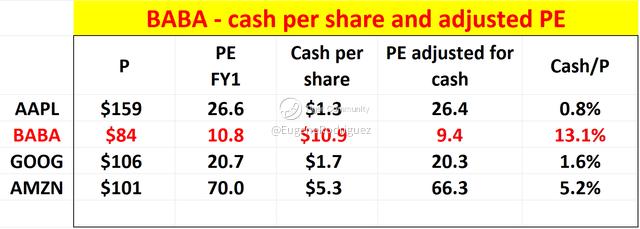

In the meantime, the company maintains a large cash position on its ledger. Total Cash and cash equivalents currently hover around $75.3B as shown below. It has a relatively low debt level (totaling $27.7B), resulting in a sizable net positive cash position. All told, these numbers translate into a cash position of around $10.9 per ADS, which is about 13.1% of its current shares.

And as to be discussed next, it's significantly higher than other comparable peers and makes its valuation even lower than on the surface.

Valuation unjustifiable

Valuation unjustifiable

According to SA data, the FY1 P/E of Alibaba is about 10.8x only, only a fraction of the valuation multiple of peers like AAPL$Apple(AAPL)$ , GOOG$Alphabet(GOOG)$ , and AMZN$Amazon.com(AMZN)$ . And bear in mind that, as just mentioned, there is roughly $10.9 worth of cash per ADS$Autodesk(ADSK)$ (about 13.1% of the current share price), dramatically higher than the other stocks listed here. AMZN has the second-highest cash per share as a percentage of its share price at 5.2%.

When the cash position is adjusted, BABA's FY1 P/E is in the single-digit: only 9.4x.

Risks and final thoughts

Risks and final thoughts

BABA is subject to various risks, and prospective investors should definitely exercise caution due to the significant uncertainties involved here. To start, as detailed in our earlier articles, some of these risks could result in a complete loss (such as with the VIE risk) or substantial losses (such as with the delisting risks).

Here I will focus on risks that are more relevant to the specific catalysts I mentioned earlier. These risks include competitive risks, operational risks, and geopolitical risks. BABA operates in highly competitive markets, including e-commerce, cloud computing, and digital payments. Existing and potential competitors can disrupt its business model or compete on price and pressure its margin. Operationally, even though China has recently lifted its Zero COVID policy, it remains uncertain how quickly customer demand can recover. And there is always the possibility for another resurgence. Finally, BABA operates in multiple countries and may face risks related to geopolitical tensions, especially with the trade tensions between the U.S. and China and also the political instability in the Russian/Ukraine region.

To conclude, BABA delivered solid results amid all the challenges in recent years the way I see things. And I see even better days lie ahead for BABA. I see a few key catalysts in the next 12 months or so, including the thawing of tension with regulatory authorities, the lift of COVID restrictions, and the recovery of consumer spending. With its strong balance sheet and strong cash flow, I see the company as well-poised to resume robust growth once the macroeconomic parameters improve. Yet, it's trading at a single-digit P/E, simply too low to be justifiable in my view.

Comments