Views are my own. Broad macro thoughts. Not investment advice.

Last year FX was driven by two huge macroeconomic shifts. Terms of Trade divergence and Rate Divergence. The sudden removal of Russian and Ukrainian commodities from some markets created a world of the Have’s and the Have Not’s. Those that had access to the core commodities the world needed – US, Australia, Canada and Norway – and those that didn’t: Europe, Japan, and UK. The Have’s received a boost from the increased demand for their exports whilst the Have Not’s were pressured by higher prices for key inputs. The result was not just a divergence in terms of trade but an additional divergence in rates as the Have’s tightened monetary policy quickly to calm their booming economies. Meanwhile the Have Not’s had to be more cautious, their central banks treading the tight rope of trying to ease price pressures from higher commodity prices without adding additional pressure on their consumers that were already struggling with the cost of living.

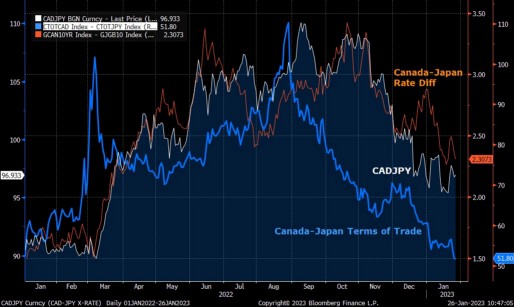

The above theme played out strongly from March 2022 – Aug/Sep 2022. I feel that CADJPY sums up this theme best as this is where the terms of trade divergence and rate divergence were strongest:

What changed in August 2022 was that Fed hawkishness reached a tipping point that drove a wave of risk aversion and lower commodity prices. The catalyst was Powell’s “pain” speech at Jackson Hole on 26th August 2022. This put an end to the sharp trend higher in commodity prices and slowed the growth of the Have’s. This has turned the terms of trade divergence sharply back lower and the rate divergence has followed. I think it is interesting to note where we are at as the most hawkish G10 central bank in 2022, the Bank of Canada, reached a pause in their hiking cycle at yesterday’s meeting. BOC’s Tiff Macklem has gone from saying this in March 2022: “The economy can handle it. We know this will be a significant adjustment, and we fully intend to tighten policy in a deliberate and careful way, being mindful of the impacts and monitoring the effects closely.” To this now: “We have raised rates rapidly, and now it’s time to pause and assess whether monetary policy is sufficiently restrictive to bring inflation back to the 2% target,”. The BOC has shifted from being the most hawkish of the pack to arguably the most dovish.

So how about the BOJ. They were clearly the most dovish central bank of 2022. Not much has actually changed there with Kuroda committing again to YCC at the last meeting. He remains adamant that the widening of the YCC band to 50bps was just an adjustment to improve market functioning. He added additional measures to improve market functioning by increasing loans to local banks for them to buy JGB’s. The aim here is for local banks to do more of the heavy lifting for the BOJ as they already own too much of the JGB market. This is similar to the TLTRO’s that the ECB used to encourage banks to buy bonds using cheap ECB financing. This should be a concern for those speculating on an end to YCC as the BOJ are attempting to make the policy more sustainable. That hasn’t put off speculation of an end to YCC yet though and Tokyo CPI tonight could add further fuel to that narrative if it comes in strong. It is generally assumed that the new governor of the BOJ after Kuroda steps down in early April will be quick to exit YCC. I treat this assumption with caution as the BOJ held its inflation forecast for fiscal year ending March 2024 at 1.6%. With medium term inflation forecasts still below target the new governor may not be in a rush to adjust policy. A lot will depend on how CPI develops along with wage negotiations. Speculators long positioning in JPY is high so I see risk of a move higher in USDJPY if Tokyo CPI is weak or Fed is hawkish next week.

Where do we go from here. How will these macro drivers develop across 2023?

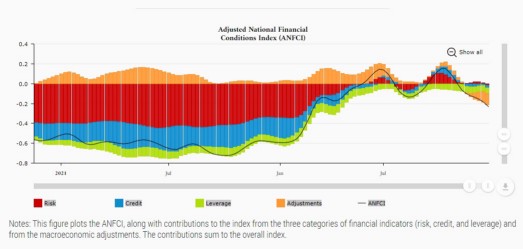

The Russia-Ukraine conflict that started all this is still in full swing. Those commodities are still unavailable to most markets in the West. Although so far to start the year the key commodity (gas for Europe) has continued to ease off in price as a warmer winter has meant lower demand whilst US LNG supply has been able to fill the gap. As a result the Have Not, Europe, has been on a track of improvement. Whilst the Have, the US, has been slowing down due to tighter Fed policy. As a result EURUSD has traded from 0.9536 in September to 1.0927 this month, levels we were at in March 2022. For the trend higher in EURSUD to continue we would need to see a continued convergence in rate differentials between Europe and the US. Therefore the Fed and ECB meetings next week are going to be critical. The ECB is almost fully priced to hike 50bps. Meanwhile the Fed is priced to hike just 25bps. Given what is priced I see a risk of ECB disappointing whilst Fed overdelivers. US financial conditions have eased significantly this year. The Chicago Fed’s index of financial conditions show that they are currently much looser than they should be given prevailing macroeconomic conditions. Given that the battle against inflation is not over yet I expect Powell to want to tighten financial conditions. Tighter US financial conditions and a slowing global economy would be a very negative backdrop for risk assets so I still expect safe havens USD, CHF and XAU to outperform whilst EUR, GBP and growth currencies underperform. Given that the BOC are at the end of their hiking cycle CAD is likely to take the brunt of any risk off selling.

National Financial Conditions Index: Current Data – Federal Reserve Bank of Chicago (chicagofed.org)

Comments