Grab$Grab Holdings(GRAB)$

Future potential

The company could benefit from numerous structural advantages. First, the market for deliveries of all kinds, including food orders, is still much younger and more immature in Southeast Asia than in Western countries. Second, the population is younger on average and very smartphone proficient compared to their parents. Compared to Western countries, smartphones are even more important as fewer people own desktop computers. And third, these countries have higher economic growth (5% in Indonesia before Covid and 7% in Vietnam).

Furthermore, the app benefits from the fact that Southeast Asia has become increasingly popular with short-term tourists and long-term expats (I am one of them) over the past decades. Thus, the app also indirectly benefits from China’s economic growth, enabling more people to vacation in nearby Southeast Asia. And if they were already used to ordering food in China, they would probably do the same on vacation.

The ecosystem

Overall, the company’s goal is to be the place to go to deliver nearly everything: food from restaurants and fresh groceries from the supermarket, providing mobility in the style of Uber$Uber(UBER)$ And then use this base to offer financial services.

Investor presentation

MTUs = monthly transacting users, where transact means successfully paying for any of Grab’s products.

This increased app usage is also reflected in the yearly monetary transaction per user. $579 is surprisingly high, considering that the median salary in Indonesia is $788.

Financial services mean that the merchants with whom they cooperate can get loans from Grab. This is supposed to be very fast and uncomplicated for the merchants and, thus, much more attractive than a loan from the bank. Moreover, the merchants can apply for the loan in the same app where they also see the evaluation of their sales. Furthermore, merchants have the option to advertise in the app.

Recent results & financials

Recently, the company reported itsQ4 numbers. Although EPS were slightly worse than expected, revenue was much stronger (GAAP EPS of -$0.10, missed by $0.03; revenue $502M, beat analyst consensus by $96.61M). This increase in revenue represents 310% more than the previous year. However, this rate of growth is not entirely representative. For instance, total revenue in 2022 ($1.43B) is 112% more than in 2021. For 2023, the company projects revenue of $2.2B to $2.3B, raising the estimate from $1.9B. This would represent a 50% increase over 2022.

Given the company’s business model, we should ask ourselves whether 2021 was a good or bad year for the company due to the covid restrictions. In Europe, we perceived the lockdown times as a boom year for all kinds of delivery services, and then in 2022, the growth figures dropped significantly. Here, however, the situation is not so clear. Because in 2021, tourism also fell away and, with it, a major source of income for many locals and, therefore, less restaurant activity and less demand for mobility. In addition, there is significantly less demand for mobility in cities when many leisure activities are not allowed. The CEO also speaks of a rebound:

WE ACHIEVED THESE RESULTS BY FOCUSING ON CAPTURING THE REBOUND IN MOBILITY DEMAND, OPTIMIZING OUR COSTS, REDUCING OUR COST-TO-SERVE AND INNOVATING ON PRODUCTS AND SERVICES THAT DRIVE STICKINESS AND ENGAGEMENT WITHIN OUR ECOSYSTEM.

CEO ANTHONY TAN

Due to numerous lockdowns and factory closures, the demand for mobility was significantly lower and is experiencing a rebound this year; in Q4, the mobility segment rose 78% YoY. In this respect, I suspect the situation is different than in Europe and that 2021 was a relatively weak year for Grab. This would mean that the growth figures for 2022 look unusually strong, and the real question will be how growth will continue this year, especially in the second half of 2023.

Future revenue growth initiatives

For the future, Grab still has numerous opportunities to increase sales. One is to expand the number of collaborations to offer users even more options for their orders. For example, there is a relatively new cooperation with Starbucks in six markets. Furthermore, they want to expand the delivery from supermarkets, because this is not yet possible in all countries.

For customers, there is also a subscription model called GrabUnlimited. This costs different amounts depending on the market and allows for savings on delivery and exclusive discount. Here in Thailand, where I am currently, this service costs just over $1.

Another possible growth driver is the plan to significantly expand the financial services area and become a fintech. In September 2022, Singapore became the first country to offer this opportunity. According to Grab, they already have a permit for a license in Malaysia as well.

Valuation & Cash

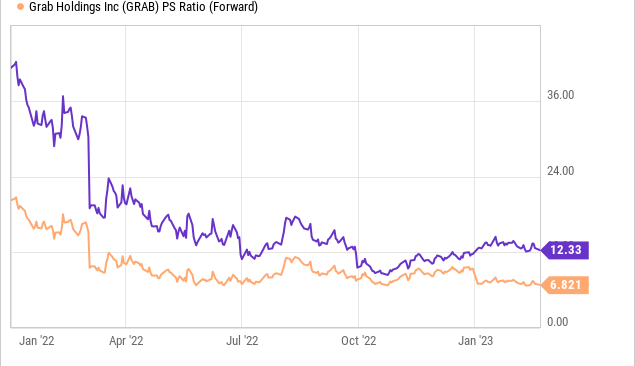

The company is currently valued at an enterprise value of $9B. The market cap is $13.5B (maybe more when you read this article), and they have significantly more cash than debt. Since Grab has no positive cash flow, it makes a fundamental share valuation difficult. The price-sales ratio of 8.6 (according to Seeking Alpha) is quite high. On YCharts, the numbers are different. The Seeking Alpha number is quite close based on total revenue in 2022 and the market cap. I think it makes sense to use the market cap and not the enterprise value, as the excess cash will be used up very quickly anyway.

When will the company be profitable?

When will the company be profitable?

HE ADDED THAT THE COMPANY REMAINS “LASER-FOCUSED” ON ACHIEVING SUSTAINABLE PROFITABILITY MOVING FORWARD. CFO PETER OEY ADDED THAT THE COMPANY EXPECTS COST EFFICIENCY EFFORTS IN 2023 TO HELP THE COMPANY UPDATE ITS BREAKEVEN OUTLOOK ON AN ADJUSTED EBITDA BASIS TO THE FOURTH QUARTER OF 2023, ACCELERATED FROM A PRIOR GUIDE OF BREAKEVEN BY THE SECOND HALF OF 2024.

According to the company, the last quarter of 2023 could therefore be breakeven. However, one has to be careful here because adjusted EBITDA offers room for creative adjustments (more on stock-based compensations below). More realistic for real breakeven or even profitability is 2024 or even 2025. At the moment, the company is still burning an enormous amount of cash.

Given this cash burn rate, the company’s financial cushion should last at least another two or three years. Possibly until the company reaches profitability. This is good news for investors as otherwise, the most obvious way to raise money would be to issue new shares.

It needs to be emphasized how severely unprofitable the company is. In the full year 2022, the loss was $1.7B. As a reminder, total revenue was just $1.4B. One of the big problems with the delivery business is that scaling doesn’t come for free. In the investor presentation, it sounds like it is a pure software business where the app is infinitely scalable. That may be true for small parts of the business but not for the main business. It always needs a driver to deliver, and also, in Southeast Asia, wages are rising, and this year, the cost of gasoline has increased. And Southeast Asia is still far away from autonomous driving; the cities there are still far too chaotic.

I think the company’s high valuation is mainly based on the fact that in the future, more profitable business areas can be developed through the one super-app. However, the current core business is a difficult business, both in the West and in Asia.

Risks

There are several risks for the company. The first is the possible emergence of competition. When I first came to Thailand 10 years ago, there were virtually no delivery services. Grab quickly captured market share as a first-mover and is now in an excellent position to defend this market. Usually, however, competition will emerge over time. Possibly in the form of many different companies that do not all focus on this large Asian market but only on individual sub-segments. For example, a company that only focuses on Malaysia can tailor their respective app even better to the market.

Furthermore, currency risks exist as the GRAB stock is traded on a US stock exchange and presents its results in dollars. However, I do not want to emphasize this point too much because currency risks can always be a currency opportunity.

Another risk lies in the currently very high valuation. Should the company unexpectedly disappoint in one of the subsequent quarterly reports, there could be a sudden and significant revaluation. In 2022, numerous companies lost 10%, 20%, or even more on the day of their quarterly results. So the higher the valuation, the greater the risk of this happening.

Share dilution and insider selling

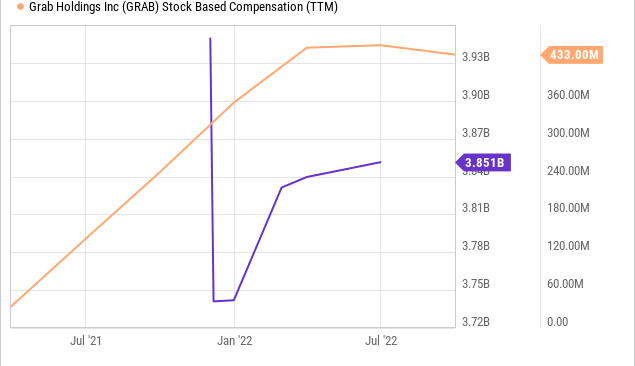

One thing I always want to look at, especially with companies that are not yet profitable, is stock dilution and whether there is insider selling. I have not found any information about insider sales. The stock-based compensations have added up to 433M for the last 12 months. For comparison, in Q4 2022, the company’s total revenue was 502M. As I look at the SBCs for each company I analyze, I can say this is huge compared to other companies. Ultimately, this masks that GAAP earnings are worse than non-GAAP earnings because they omit SBCs. Since the IPO in December 2021, outstanding shares have increased by approximately 3%.

Conclusion

Conclusion

The company has a lot of potential to expand its existing customer base and strong market position in several countries and become a super-app. I hesitate to call it that now as it is mainly a delivery service and cab replacement. I don’t want to badmouth the business, but we as investors should keep in mind that these are two areas where even in the west, companies have problems becoming profitable. It is often like this with strong growth but unprofitable companies: High-risk, high reward. The risk is too high for my taste because of how much cash is currently burned, and the valuation is very high. In addition, as an investor, I do not like when SBCs are enormously high, and thus the actual personnel costs of the company are somewhat masked. Overall, I think there are currently better and safer opportunities in the market.

Comments