It was another winning week for the stock market amid thinner holiday trading conditions. S&P 500$S&P 500(.SPX)$ is up 1.5%, while tech heavy Nasdaq Composite$NASDAQ(.IXIC)$ also closed the week on a positive note with a gain of 0.7%. The gains were consistent with a seasonal bias considering the market normally trades with a positive disposition during Thanksgiving week.

Friday’s U.S. jobs report for November will be the main highlight of the coming week as investors remain hopeful that the Federal Reserve will soon slow the pace of rate hikes. Remarks by Fed Chair Jerome Powell mid-week will be closely watched. PMI data will also be under the spotlight amid concerns over a resurgence of COVID cases there.

Here’s what you need to know to start your week.

1. Fed Chair Powell Speaks

Fed Chair Jerome Powell is to discuss the economic outlook during an appearance at the Brookings Institution on Wednesday.

While Powell has indicated that the Fed could shift to smaller rate hikes next month, he has also said rates ultimately may need to go higher than policymakers thought would be needed by next year.

2. Retail stocks

As Wall Street reopens after the Thanksgiving holiday investors will be focused on how retailers are faring over the holiday shopping period, as well as the Fed’s next steps.

Black Friday sales got underway against a backdrop of persistently high inflation and cooling economic growth. Retailers are offering steep discounts both online and in store, which will likely impact profit margins in the fourth quarter.

Online spending rose by 2.3% to a record $9.12 billion on Black Friday, according to a report by Adobe Analytics on Saturday, but the percentage increase was well below the annual rate of inflation which is currently running at 7.7%.

U.S. retail stocks have become a barometer of consumer confidence as inflation bites. So far this year, the S&P 500 retail index is down a little over 30%, while the S&P 500 has fallen 15%.

3. China PMIs

PMI data on Wednesday will be closely watched. China said on Friday it would cut the amount of cash that banks must hold as reserves for the second time this year, releasing liquidity to prop up economy.

Key Economic Calendar (Weekly)

It will be a very busy week in the US with the labor report taking the central stage followed by speeches by several Fed officials, 2nd estimate of GDP growth, ISM manufacturing PMI, CB consumer confidence, and personal income and spending.

All times listed are EST

Tuesday

10:00 US – CB Consumer Confidence: forecast to decline from 102.5 to 100.0

Wednesday

8:15 US – ADP Non-Farm Employment Change: forecast to decline from 239K to 200K

8:30 US – Prelim GDP q/q: forecast to increase from 2.6% to 2.8%

10:00 US – JOLTS Job Openings: forecast to decline from 10.72M to 10.36M

1:30 US – Fed Chair Powell Speaks

Thursday

8:30 US – Core PCE Price Index m/m: forecast to decline from 0.5% to 0.3%

10:00 US – ISM Manufacturing PMI: forecast to decline from 50.2 to 49.8

Friday

8:30 US – Non-Farm Employment Change: forecast to decline from 261K to 200K

8:30 US – Unemployment Rate: forecast to maintain at 3.7%

Top Leading and Lagging Sectors (Weekly)

All 10 S&P 500 sectors closed with a gain this week, less energy sector as market participants continue to deal with growth concerns.. The utilities (+5.0%) sector sat atop the leaderboard.

Heat Map (Weekly Performance)

$Apple(AAPL)$ $Amazon.com(AMZN)$ $Microsoft(MSFT)$ $Alphabet(GOOG)$ $Alphabet(GOOGL)$ $Meta Platforms, Inc.(META)$ $Johnson & Johnson(JNJ)$ $Pepsi(PEP)$ $Procter & Gamble(PG)$ $Tesla Motors(TSLA)$ $Berkshire Hathaway(BRK.B)$ $Berkshire Hathaway(BRK.A)$ $Bank of America(BAC)$ $Eli Lilly and(LLY)$ $NVIDIA Corp(NVDA)$ $Broadcom(AVGO)$ $Cisco(CSCO)$ $UnitedHealth(UNH)$ $Visa(V)$ $MasterCard(MA)$ $Wal-Mart(WMT)$

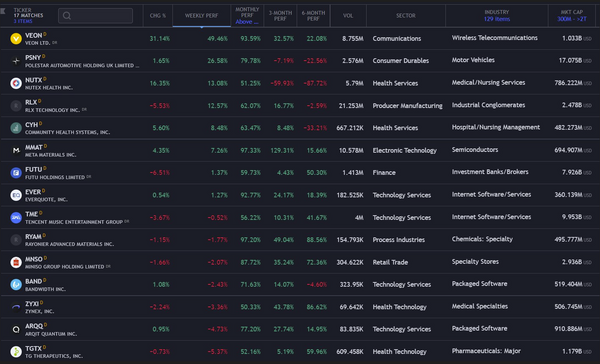

Strongest Momentum Leaders Of The Week (% Gain Sorted)

Market Breath (Weekly)

% of Stocks Above 20 DMA = 67.20% (+4.61%)

% of Stocks Above 50 DMA = 70.48% (+5.68%)

% of Stocks Above 200 DMA = 45.84% (+7.94%)

Market Technicals – (S&P 500, NASDAQ, Bitcoin, Bonds & Credit Spread, NAAIM)

$S&P 500(.SPX)$ SPX (S&P 500) – (Net High/Low +58)

A hard landing for the economy was a prominent concern for market participants as the central banks ramped up their fight against inflation. It led to broad-based selling, rooted in worries that there will soon be large cuts to earnings estimates. Accordingly, there was a reticence to pay up for stocks and an inclination to take risk off the table. Worries about an economic downturn have hammered equities this year. The S&P 500 remains down -16.8% for the year to date, remaining on track for its largest annual decline since 2008.

$SPX regain its upward posture this week, bouncing off its rising 10-day moving average with a gain of+1.5% for the week. Aside from the seasonality factor, the upside bias was fueled by better than expected earnings reports from retail issues like Best Buy ($BBY) and Abercrombie & Fitch ($ANF), along with some names from the tech space like Analog Devices ($ADI) and Dell Technologies ($DELL). Also, farm equipment company Deere ($DE) was among the more notable earnings-driven winners.

At the current juncture, $SPX remains above its rising 10/20-day moving average inside the month long uptrend channel, but still caught below its medium term downtrend line.

The resistance to reclaim for further positivity in the market is at 4,060, the current declining 200-day moving average level.

Bull Case: Reclaim above 4,060, the current declining 200-day moving average level.

Bear Case: Breakdown of 3,906 level, breaching its rising 10 & 20-day moving average. Next support at 3,800, the current 50-day moving average level.

$Invesco QQQ Trust(QQQ)$ QQQ (Nasdaq 100) – Similar Range Breakout From July 2022 May Be In Play

Tech and growth names have been hard hit since the start of 2022 by a rapid rise in Treasury yields on the back of expectations that the Fed will hike interest rates aggressively to combat high inflation as higher rates can hurt their companies with high valuations based on the prospect of future profits.

The tech-heavy $QQQ gained +0.74% for the week. Similar to $SPX, $QQQ rebounded via finding support on its rising 10-day moving average.

The support level to watch for $QQQ this week is revised up to 274, undercutting its current rising 10/20-day moving averages.

Bull Case: Reclaim above 293 the immediate classical resistance.

Bear Case: Breakdown of 274 level, undercutting its current 10/20-day moving averages.. The next support level is at 260.

BTCUSD (Bitcoin / USD) – A True Breakdown, But More Weakness Ahead

Bitcoin ($BTCUSD) price action remains subtle for another week with a +1.88% gain. $BTCUSD remains languishing at the $16,000 level as $3 billion escaped crypto exchanges in early November amid a bank run on fears of an FTX contagion.

$BTCUSD daily action continue to morphed out a further Bearish Pennant pattern prompting the risk of a further accelerated sell off in near term remains.

The level of support to watch for $BTCUSD this week remains at $15,630, a breakdown of the year to date low.

Bull Case: Recapturing its declining 50-day moving average at $19,000.

Bear Case: Breakdown of $15,630, the year to date low.

PCCE (Put/Call Ratio Equity) & VIX (Volatility S&P 500) – Lowest $PCCE Print In 4 Months Violated Mid-Term Bearishness

VIX >30 is assumed to accompany large volatility, resulting from increased uncertainty, risk, and investor fear. VIX <20 generally correspond to stable, stress-free periods in the market. Higher VIX levels equates to more expensive options premium and vice versa for lower VIX level. Market will often bottom when the VIX gets up to a high level as traders will be willing to pay a very high premium to protect themselves from further downside.

The spike level to watch for $PCCE in the last 24 months period is at 1.00. The current reading is 0.737 (+0.39%), 2 weeks after setting lowest print for $PCCE over the last 4 months, a violation of its year-long build up in momentum for a major sell off for the equities market.

Conversely, the VIX volatility index, also known as Wall Street’s fear gauge decline to 20.51 (-11.25%).

It is worth to note that both $PCCE and $VIX is currently below its 200-day moving average, which could translate to more positivity for market indexes in the upcoming week.

$Cboe Volatility Index(VIX)$ $BIONDVAX PHARMACEUTICALS SPON ADS EACH REP 400 ORD SHS(POST SPLT)(BVXV)$

VIX/VXV – Reading at 0.88 (Tranquility)

The VIX/VXV measures the ratio between 1-month implied volatility and 3-month implied volatility, which is helpful as it filters out higher baseline readings on VIX.

If it is greater than one, it implies uncertainty, negative for equities. On the contrary, such high reading (i.e. spikes) coincide with market bottoms.

If it is less than one, it implies tranquility, favorable for equities.

If it is below 0.82, the returns for S&P500 are often less than stellar.

$IEI(IEI)$ $HYG(HYG)$ IEI/HYG (Credit Spread) & TNX (10YR Treasury Yield) – Aggressive Equity Rally Was a Relief Rally In An Inverted Yield Environment

Market participants are keeping a close watch on credit spreads as one of the better economic signals. Junk bond issuers are perceived to be bigger credit risks, so if economic growth slows or contracts, there will be increased angst that these issuers won’t be able to make good on their interest payments. Hence, a widening high-yield spread is regarded as a leading indicator of difficult economic times which, in turn, often invites a more challenging period for the stock market since difficult economic times translate into weaker earnings prospects.

Higher Credit Spread = Insolvency Concerns

Lower Credit Spread = Healthy Market

Credit Spread movement remains subtle as it inched down to 1.54 (-0.01) for the week. The year to date high level is at 1.64 set in early July.

Movement in the Treasury market was generally supportive of the stock market this week. The 10-yr note yield ($TNX) fell 13 basis points to 3.69% and the 2-yr note yield fell 2 basis points to 4.48%.

NAAIM Exposure Index 64.96 (+21.81%)

The NAAIM Exposure Index represents the average exposure to US Equity markets reported by members of the National Association of Active Investment Managers. It provides insight into the actual adjustments active risk managers have made to client accounts over the past two weeks. The blue line depicts a two-week moving average of the NAAIM managers’ responses.

This week’s NAAIM Exposure Index number is: 64.96 (Wednesday)

https://www.getrevue.co/profile/jeffsuntrading/issues/10-minutes-weekly-picture-growing-covid-protest-spreads-across-china-but-disconnect-already-expanded-with-global-economies-trading-ideas-tme-ryam-mnso-tgtx-28th-november-2022-2nd-december-2022-1476593?via=twitter-card&client=DesktopWeb&element=issue-card

Comments