While we continue to view Grab Holdings Limited (NASDAQ:GRAB) as a highly speculative investment, we continue to see the company making progress towards profitability after it reportedthird quarter results. Year-over-year group revenuewas up over 140%, and loss for the period improved substantially. Monthly transacting users also grew 30% y/y, accelerating significantly from the previous two quarters.

The company achieved an important milestone during the quarter, with the delivery business turning segment adjusted EBITDA positive for the first time. Another big positive was that revenue for deliveries tripled compared to the same period a year ago.

While the company continues to be unprofitable, there is a lot of potential. We, therefore, continue to view Grab as a high risk, high reward type of investment. As a reminder, about one in twenty people in Southeast Asia eat, ride, or pay with Grab every month. Grab is Southeast Asia's leading super app, operating in more than 480 cities.

Grab Investor Presentation

The company is becoming more disciplined with its spending and incentives in order to make progress towards its profitability goal. Total incentives as a percentage of gross merchandise volume (GMV) continued to improve, going down to ~9.4%. This helped improved adjusted EBITDA margins as a proportion of GMV improve to -3.2%.

Grab Investor Presentation

The deliveries segment adjusted EBITDA margin turned slightly positive, delivering 0.4% adjusted EBITDA as a percentage of the deliveries GMV. The mobility segment delivered adjusted EBITDA margins of 12.5% for the quarter, despite still being at only ~80% of pre-Covid levels in terms of driver-partners. Advertising and financial services still remain relatively small businesses for the company, but have a lot of potential. For example, merchants were getting four to seven times returns on their advertising spend on Grab in the third quarter this year. We believe these relatively new business have a lot of potential.

Q3 2022 Results

Revenues grew 143% y/y or 156% on a constant currency basis to reach $382 million. Mobility revenues doubled y/y thanks to the continued recovery in ride-hailing demand. Deliveries revenue more than tripled, while financial services and the enterprise segment recorded revenue growth of 44% and 113% respectively.

GMV for the third quarter recorded growth of 26% y/y to reach $5.1 billion, an all-time high. On a constant currency basis, GMV grew by 32% y/y. The company reported an IFRS loss of $342 million, representing a 65% improvement from the loss of $988 million in the prior year period.

Grab Investor Presentation

Pathway to Profitability

During its investor day in September this year, the company shared its goal to reach group adjusted EBITDA breakeven in the second half of 2024.

Grab Investor Presentation

The company reaffirmed this target during the most recentearnings call, saying it remains confident that the $5.3 billion of net cash liquidity as of the third quarter should be a big enough buffer to allow the company to reach its expected group adjusted EBITDA breakeven in the second half of 2024. Peter Oey, the company's CFO, even talked about the possibility to accelerate this time line, although for the time being they are not updating their guidance:

On your question about group EBITDA breakeven time line, as Alex mentioned, deliveries profitability was a very critical milestone for us. And we're just getting started here, and we're going to continue to accelerate the profitability time line for deliveries to get to that steady state margin. That's a key focus area for us. We're also very focused Pang, on making sure our cost base also continues to be optimized as a business.

Now your question, is there room for upside for that time line for the second half 2024? Yes, there is upside. And see potential for that to accelerate. But where we are today, we are maintaining guidance for now, and we can continue to focus on – continuing to focus on the deliveries, acceleration margin, as well as just continuing to refine the business and continue also to have that profitable growth that we saw this quarter again.

Balance Sheet

Grab ended the third quarter with $7.4 billion of gross cash liquidity, with cash liquidity declining by $291 million from the end of the second quarter of 2022. Net cash liquidity was $5.3 billion as of the end of the third quarter. The company shared that right now cash preservation is top of mind for them.

Grab Investor Presentation

Guidance

The company sounded confident that revenue can outperform their initial guidance range of $1.25 billion to $1.3 billion for 2022, which they now raised to be $1.32 billion to $1.35 billion. This represents 105% to 110% y/y growth on a constant currency basis.

Grab also reiterated its expectation to grow revenues by 45% to 55% y/y in 2023 on a constant currency basis. The company also raised its adjusted EBITDA expectations for the second half of 2022 to a $315 million loss from a $380 million loss previously. This would represent a 40% half-on-half adjusted EBITDA improvement.

Valuation

It is difficult to value Grab given that it has yet to turn profitable, and for the time being it continues to burn cash. Still, the company has a lot of potential and it could become profitable in a few years if the company hits its targets. One way to think about Grab's valuation is by comparing its enterprise value and market cap against the size of the economy taking place in its super app, otherwise known as the GMV. Annualizing the most recent quarterly GMV results in ~$20 billion of GMV, which compares favorably to Grab's ~$12 billion market cap and ~$7.5 billion enterprise value.

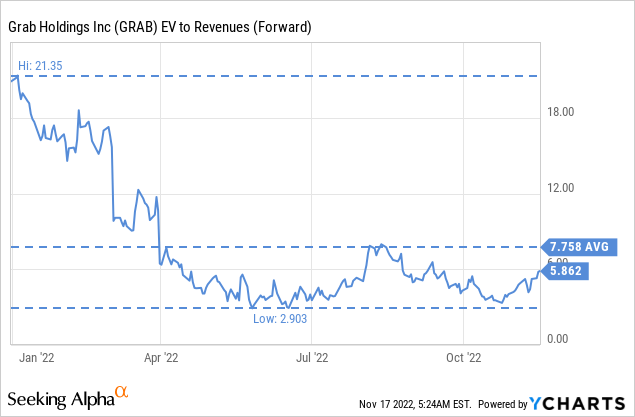

Another valuation metric that can be used is EV/Revenues. The forward EV/Revenues multiple currently stands at ~5.8x. Whether this turns out to be cheap or expensive will, of course, depend on how long the company can maintain its high growth rate, and whether or not it can turn profitable in the next couple of years.

Risks

Risks

The biggest risk we see with an investment in Grab is that it continues to be a cash burning operation, although it is making significant progress on its road to profitability. We believe this is a very high risk, high potential reward type of investment.

Conclusion

Grab delivered positive news during the most recent quarterly results, in particular sharing that its delivery segment achieved breakeven in the third quarter. The mobility segment still has not gotten back to pre-Covid levels, but it is quickly recovering. Importantly, the company committed to ~55% revenue growth in 2023, and to reach group profitability in the second half of 2024. We continue to view shares as offering high risk and high potential reward, depending on how long it can maintain its high growth rates, and whether or not it manages to become profitable.

Comments