Cameco Corp. Q2 Results Better, But Shares Down Over The Last Month

Summary

- Cameco Corp. has the world's largest high-grade reserves and is a low-cost producer of uranium, with investments in nuclear energy.

- Second Quarter 2024 financial results show strong operational performance, with revenue up 24% year-over-year.

- Cameco's stock price has been under pressure of late but the worst could be over.

honglouwawa

Introduction

Twelve months after the disaster that struck Fukushima we posted an article on Cameco Corp (NYSE:CCJ) with a "Buy" rating on 12 April 2012. This stock had suffered badly in an environment where nobody wanted nuclear energy as the chart below shows:

Cameco Chart April 2012 (stockcharts)

I am for nuclear energy as a part an energy strategy along with the new green technologies and have traded in and out of various uranium miners over the last two decades. More recently I covered Cameco in May 2021 and again in August 2023 on release of their Q2 financial results. So today I will take a quick look at Cameco's 2024 Q2 financial results and try and ascertain if it is a Buy, a Hold, or a Sell.

Cameco Corp. Brief Description

Cameco is a $17 Billion company and is in the enviable position of being the world's largest high-grade reserves and low-cost producer of uranium. Allied to their mining operations they also have considerable investments throughout the nuclear energy space, evidenced by their ownership in Westinghouse Electric Company and Global Laser Enrichment. They have been present in the nuclear energy field for 35 years and are considered a "Go To" company by investors wanting to deploy their funds into this segment of the energy sector.

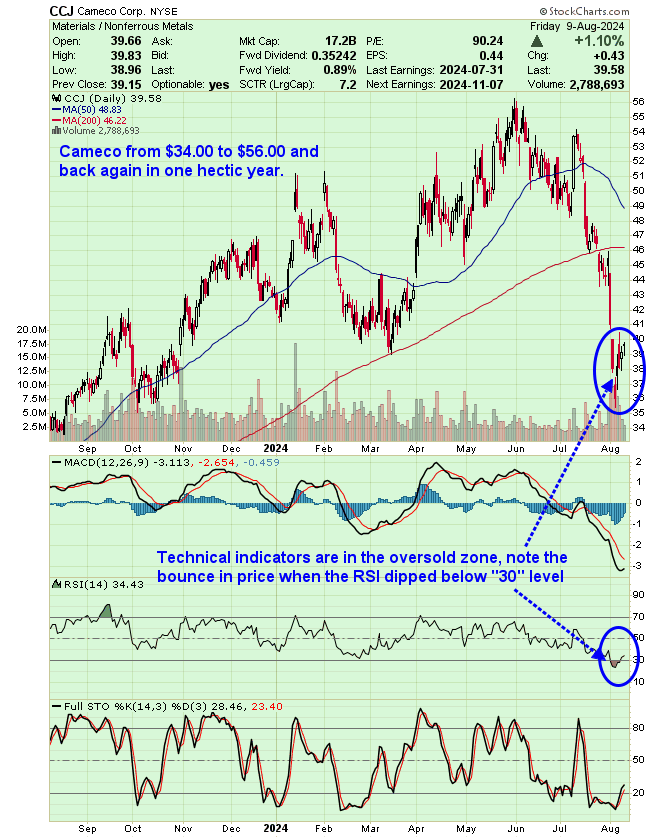

Cameco One Year Chart

The following chart depicts Cameco's wild price oscillations over the last twelve months which saw the price move from $34.00 to $56.00 and back again in a volatile trading period.

Cameco Corp One Year Progress Chart (stockcharts)

The Technical Indicators are in the oversold zone, note the bounce in price when the RSI dipped below the "30" mark. The selling off of this stock may now be over but we do need to wait and allow the dust to settle in order to get a clearer picture of just what the future might hold. A lot depends upon the underlying commodity of uranium so we will take a quick look at its price chart next.

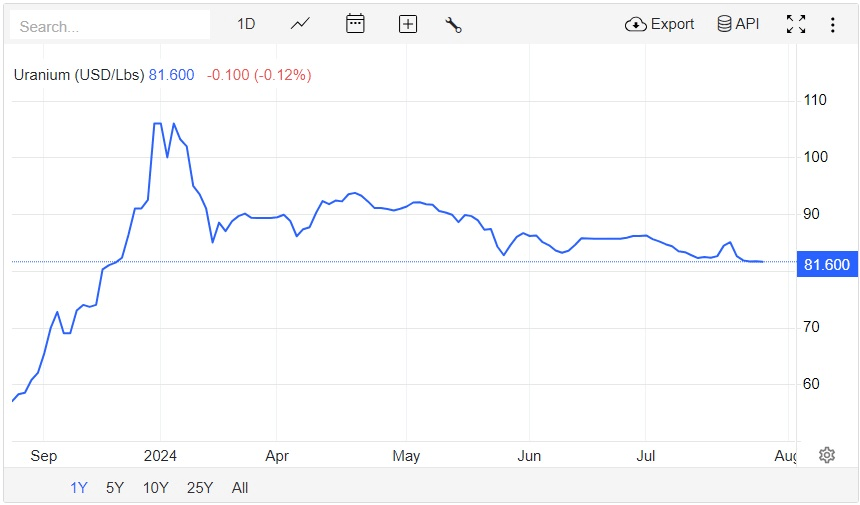

Uranium One Year Price Chart

A rally in the price of uranium took it to $106/lb before drifting back to today's price of $81.60/lb. From this chart we can glean that the "fizz" in the price has eroded a little, however the price is still holding up fairly well.

One Year Uranium Price Chart (Trading Economics)

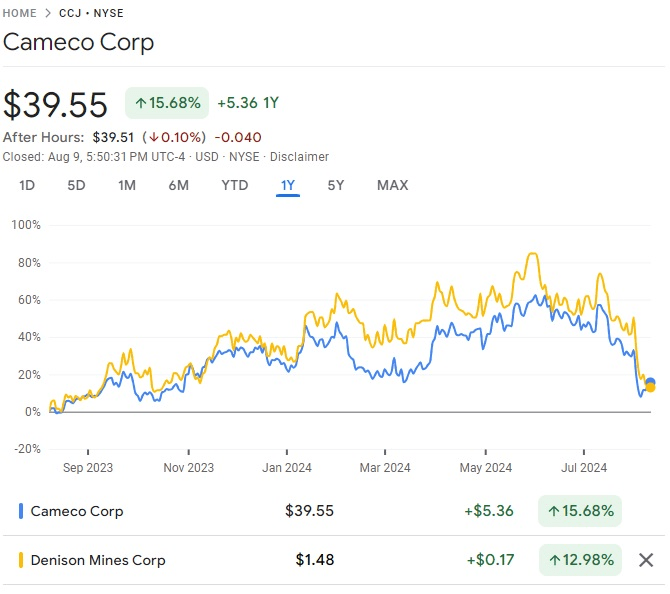

It should be noted that others in this space suffered a similar price pull back, such as Denison Mines Corp (DNN) as illustrated on the chart below comparing the two companies

Cameco Corp compared with Denison Mines Corp (Google Finance)

Despite the sell-off both Cameco and Denison are still up for the year by similar percentage points.

Second Quarter 2024 Highlights

I would like to start with a quote from Tim Gitzel, Cameco's president and CEO who commented as follows:

"Second quarter operational performance was strong, driving financial results that remain in line with our full-year 2024 outlook," He also touched on their outlook with the following comment:

"Our contract portfolio spans more than a decade, with annual commitments from 2024 through 2028 increasing this past quarter to an average of about 29 million pounds per year."

All very positive from the CEO but do remember that it is his job to display the company in a good light in order to attract investment funds.

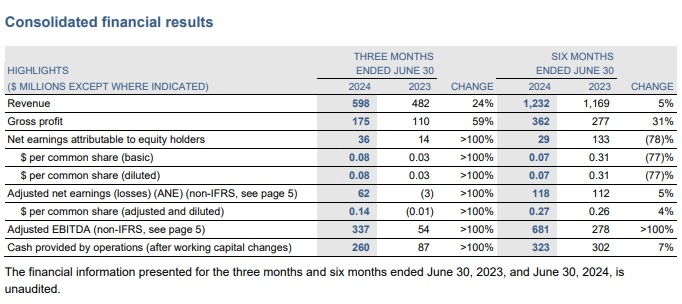

The chart below shows Cameco's Consolidated financial results where we can see that the six month period ending June 2024 compared with the same period in 2023. Revenue was up 5% and the Gross Profit was up 31%. For the three-month period ending June 30, 2024 the net earnings are $36 million. A standout for me is that the Revenue of $598 million is up on a Y/Y basis by 24%.

Cameco Corp Consolidated Q2 Results (Cameco Q2 Financial Results)

Also pleasing to read is that the outlook for 2024 is on schedule with the expectation of strong cash flow generation, with revenue of between about $2.85 billion and $3.0 billion

On the downside we need to take into consideration that the price of uranium is well off its peak and that casts a shadow over the whole of this sector and Cameco's stock price has given back a lot of its recent gains. This suggests that it is not all blue sky sailing and that the uranium producer's future could be as volatile as its recent past has been.

However, I am of the opinion that there are profits to be made in this sector but stock selection and the timing of entry and exit points will be critical to one's financial health. So please put some effort in and do your own due diligence for your own peace of mind, after all it's your hard-earned cash that is on the line.

Financials

Cameco has a market capitalization of $17.21B, a 52-week trading range of $33.63-$56.24, a P/E Ratio (TTM) of 92 and an EPS (TTM) of 0.43. The average volume of shares traded per day is 3,618,393 enabling easy access for traders of both Stocks and Options.

Looking ahead the EPS (FWD) is 0.59 and the PE (FWD) is 66.57 which is a slight improvement on the current position and a tad more attractive to both investors and speculators who are interested in investing in this unique part of the energy sector.

Taking a quick look at Seeking Alpha's Quant Ranking Cameco is ranked in Industry at 7 out of 15 with a rating of Hold which is fairly average for this sector. Although the Quants have six other companies above Cameco they cannot compete with the size of Cameco and the resources at its disposal. As the demand for uranium grows I suspect that this giant will perform well, however, there may be those smaller companies that can provide a larger capital gain in percentage terms and that is where I aim to be. If I owned Cameco today I would be tempted to retain it in my portfolio, but I don't own it and I just can't pull the trigger and acquire it, although the stock price has become a lot more attractive of late.

Cameco Corp. trades on both the NYSE under the symbol of CCJ and in Canada on the TSX under the symbol of CCO.

Conclusion

Cameco, from a chart perspective, does look oversold and therefore a correction in the near term could be on the cards.

A giant in this sector of the market it is an attractive proposition for fund managers seeking exposure to the nuclear energy sector.

Cameco may be too big to sprint and smaller producers may outperform it in terms of capital gains.

Got a comment?

Then, please fire it in whether you agree with us or not, as the more diverse comments we get, the more balance we will have in this debate and hopefully, our trading decisions will be better informed and more profitable.

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.