Will Under Armour's plummet affect NKE/LULU?

$Under Armour Class A(UAA)$ released Q1 earnings report before May 6 open, and fell by 26% in a single day. Although the stock price was already staying low the, it still could not stop investors selling it to single digit.

The performance fell short of expectations, and the guidance lowered, all of which made investors tremble with fear in the current jittery market.

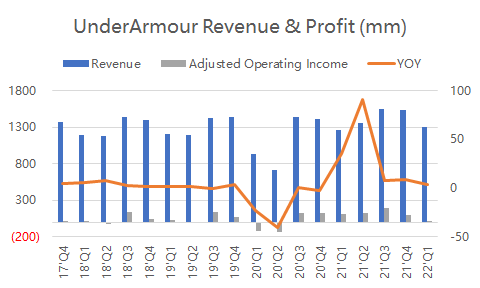

- Revenue growth rate further decline to 3.5% $1.3 billion in a single quarter, roughly the same as market expectations.

- Among them, clothing was 880 million US dollars, a year-on-year increase of 8.2%; Footwear was 300 million US dollars, a year-on-year decrease of 4%; Authorized revenue increased by 23% year-on-year to US $26.6 million;

- Regionally, the revenue in North America was 840 million US dollars, a year-on-year increase of 4.4%; The Asia-Pacific region was US $180 million, a year-on-year decrease of

- Inventory turnover rate further increased to 3.45, and the inventory turnover days further decreased to 106 days;

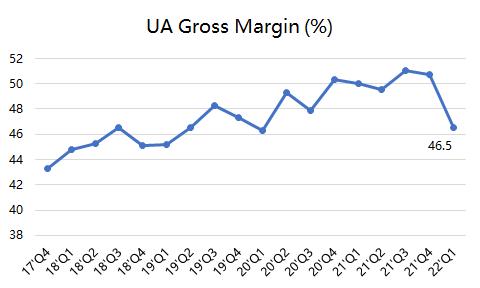

- Gross profit decreased by 3.7% year-on-year to US $600 million,Gross profit margin fell to 46.5%The level of;

- The operating loss was $46 million. The adjusted EBITDA was US $45.68 million, which was far less than the expected profit level of the market.

Judging from Q1 performance, the revenue was barely equal to the market expectation, but the profit index was much lower than expected, and there was an operating loss, which was unexpected by the market. Among them, gross profit margin dropped to the lowest level in history.

Due to the telephone conference last quarter, UA executives have warned that rising freight rates will erode profits. Therefore, most investment banks have lowered their gross profit margin accordingly. Still, costs for the quarter were well ahead of analysts' expectations, and it is more likely that executives are not "telling the truth."

In fact, compare to $adidas AG(ADDYY)$, $Nike(NKE)$, $Lululemon Athletica(LULU)$, Under armour is more vulnerable to the rising cost of raw materials .

One of UA's motto is that "cotton is our natural enemy", which implies that their sports clothing products do not use cotton as the material, because in sports , cotton are not easy to dry, so they are not the best materials. Therefore, most of the raw materials of UA are polyester fibers of petroleum derivatives, including polyester, spandex, acrylic fiber and so on. The biggest advantage of polyester fiber is its good wrinkle resistance and shape retention, high strength and elastic recovery ability, and it is a favored raw material in sports field.

Therefore, rising oil prices are the natural enemies of Under armour.

Supply chain crisis and rising logistics costs did affect the company to a certain extent in Q4 last year, but the problem has been alleviated to a great extent in Q1 this year, the company's revenue, inventory turnover rate and other data are improving, so the biggest problem is still the profit margin.

Will such problems also bother other sports brand companies?

Yesterday in the UAA belt fell, LULU bigIt fell 7.7%, while NKE was slightly stronger and fell 3.5%.

In fact, the market is by no means a fool. Nike dropped less, not only because of its great scale, but also the market understands that companies embracing "cotton" will less impact by oil price, even if the profit margin is affected, it will never be as big as UA.

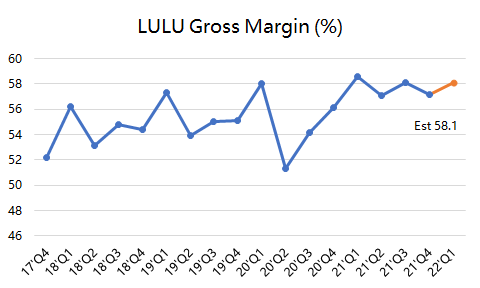

While LULU's large portion of yoga clothes are also polyester products, so its profit margin may be greatly affected. (Even if the impact in the current period is not great, it will be deferred).

At present, the market expects LULU's gross profit margin to be 58.1%, which is still a new high. With UA's experience, will investors reconsider?

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- lappiloco·2022-05-08bad news for retail industry3Report

- familoveyou·2022-05-07I won't consider buying Under amour.3Report

- Dollydolly·2022-05-07Thank your sharing, good readability3Report

- Ra007·2022-05-08Lulu’s got a huge following2Report

- YSLiu·2022-05-07they are all linked2Report

- JessieTheresa·2022-05-07maybe it's right time to do short for others?1Report

- Toshies·2022-05-09nike is quite a beast1Report

- JuliusGoldsmith·2022-05-07gonna find another industry to invest hmmLikeReport

- DouglasMalan·2022-05-07Surely it will affect LULULikeReport

- Trevelyan·2022-05-07that was so shockedLikeReport

- N00b·2022-05-10okLikeReport

- KenYH·2022-05-09Ok1Report

- Fayedea·2022-05-09Great2Report

- DQS4288·2022-05-09👍🏻1Report

- yoyose·2022-05-09[Like]2Report

- Imkpy·2022-05-09agree1Report

- ivyteo6911·2022-05-09👍👍👍LikeReport

- Jacklyn26·2022-05-09OK1Report

- Stx·2022-05-09Good day1Report

- wongps·2022-05-09棒1Report