So-called 'zero days to expiry' or '0DTE' options, are designed for institutional investors to hedge their exposure to outsized price swings on days of known event risk, such as U.S. employment and inflation data releases, or Federal Reserve interest rate decisions.

But they are attracting the attention of more speculative parts of the investment and trading community, at a time of increased market fragility due to higher interest rates, an unfolding banking crisis, and growing fears of wider economic and financial turmoil.

In a report published earlier this month, analysts at JP Morgan sketched out a worst-case scenario in which these options could trigger anintraday 25% routin the S&P 500 if they are unwound following an initial, sudden 5% market drop.

Understandably, a potential 25% crash in one day garnered a lot of attention. But even the less gloomy hypotheticals outlined in the report, such as a sudden 1% or 2% slump, still pointed to an even greater selloff than the original fall.

Peng Cheng, one of the authors, says this kind of scenario is less likely to play out on 'event days' like nonfarm payrolls data or Fed policy decisions. Investors know the event risk so they tighten controls, and are generally more cautious.

All else equal, this helps reduce systemic risk to the wider market. But on 'non-event days,' speculative activity increases.

"These options are being used more now for systematic trading, which is surprising ... (and) because of that, they have more potential to increase volatility on 'non-event days,'" Cheng said.

"On 'non-event days' there is more chance of an unexpected market shock, in which case investors may face greater losses in their short option positions, and that may increase intraday volatility," he added.

This nods to the Rumsfeldian world of 'known unknowns' and 'unknown unknowns.' Calendar event risk, or 'known unknowns,' may unleash market volatility, but investors can hedge or sit on the sidelines. Their '0DTE' options positions are much more likely to be hit by 'unknown unknowns' at random times.

POPULARITY SURGES

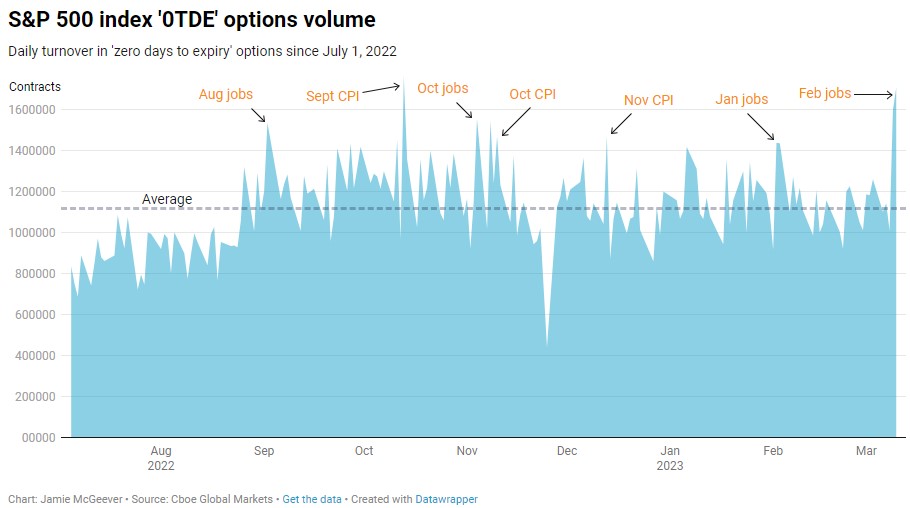

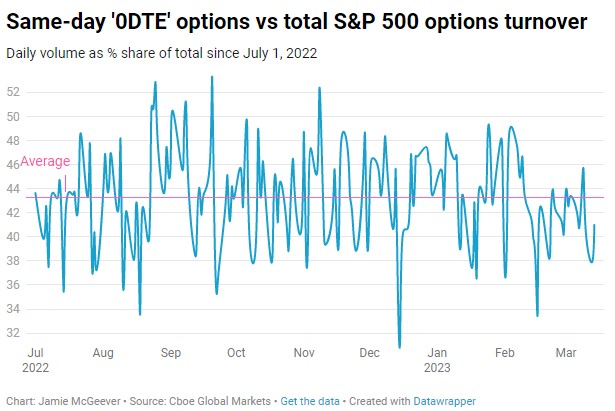

Data from Cboe Global Markets shows that '0DTE' options have grown in stature over the past several months. They have accounted for more than 40% of daily turnover in all S&P 500 index options since last July - a year ago it was around 20%.

Nominal trading volumes in these contracts often spikes up on 'event days' like U.S. jobs and inflation data days. The 1.7 million contracts traded on March 10, the day of the February employment report, is second only to the 1.76 million traded on Oct. 13, the day September CPI inflation data was released.

However, as a share of overall options turnover - which Cheng says is a better indication of potential market risk - many of the recent peaks have been on random 'non-event' days.

He and his colleagues estimate that the daily notional value of trading in '0DTE' options has grown to about $1 trillion.Reuters exclusively reportedlast week that Wall Street players and a major U.S. clearing house are examining the potential risks the explosion in trading these contracts poses.

But the Cboe points out that volume is evenly split between 'put' and 'call' options, reflecting a balanced market. Some 65%-70% of trades are closed out before expiry, which caps the accumulation of large, outsized positions, the exchange adds.

But it is worth monitoring how these options evolve, particularly with the Fed switching to a more data-dependent policy stance, which could in turn generate more speculative activity on big calendar 'event days.'

Fed Chair Jerome Powell indicated to lawmakers earlier this month that the decision to raise rates by 25 or 50 basis points at the March 21-22 policy meeting would likely hinge on February employment and CPI inflation data. These reports were released on March 10 and 14.

It's one thing for central banks to be 'data-dependent,' another to pin policy decisions on specific data.

"My sense is that Powell was trying not to surprise the market with 50bp — a little bit of forward guidance," said John Silvia, economist and founder of Dynamic Economic Strategy. "But it is very rare — and risky – to make such a specific number outlook."

Comments