Summary

- We were wrong about TSMC. Over the last 12-14 months, the consolidation zone was a distribution phase. Also, the bull trap in January drew in the last of the dip buyers.

- We realized that the market is digesting its massive 2020 gains. Also, its FCF yields are still much higher than its 5Y mean. Also, TSMC's profitability could be peaking.

- Our analysis indicates that investors need to be prepared for slowing growth from H2'22. As a result, it could lead to more digestion, given its weak FCF yields.

- Therefore, the risk/reward profile has weakened significantly. Accordingly, we revise our rating from Buy to Hold. We urge investors to wait for a better entry point.

Investment Thesis

Since November, we have been optimistic about TSMC (NYSE:TSM) as we thought its thesis remains strong amid the secular growth drivers underpinning its capacity expansion.

Management has also demonstrated its solid execution, as TSMC sees robust growth drivers in high-performance computing (HPC) and automotive segments. Therefore, it further underscores TSM's front-row seat as the semi industry's most crucial logic foundry leader.

However, despite a solid Q1 performance, with raised guidance, the market has not re-rated TSMC stock. That drove us to evaluate why the market has continued its massive consolidation phase, despite its robust performance.

That's when we realized that perhaps the market could have already priced in these performances. A closer look at its NTM FCF yields indicates our suspicion. It was also the critical underpinning of our initial Hold rating in October last year. We reminded investors to be cautious of its FCF multiples.

Therefore, as we revisited our previous thesis, we also saw the massive surge in 2020 that drew in buyers rapidly. Our price action analysis indicates that the consolidation that occurred over the last 14 months was a quiet distribution phase by the market makers. The price then broke below its critical support level as the market makers looked to digest its 2020 gains.

While the stock could have found a short-term bottom, we believe the risk/reward profile has worsened dramatically for its near-term re-rating. TSMC could face further headwinds relating to raw materials inflation as it seeks to protect its gross margins. The company's revenue growth and profitability are also estimated to decelerate from FY23.

As such, we revise our Buy rating to Hold, as we urge investors to wait for a more attractive entry point.

TSM Stock FCF Yields Are Low

TSM stock NTM FCF yields %(TIKR)

In our June article (Buy rating), we highlighted that investors must be wary of its massive capex expansion as it could significantly impact its FCF. Notably, the impact will be more pronounced if it faces operating deleverage, given its enormous fixed costs. But we were impressed with the company's stellar performance quarter after quarter. There's little doubt that TSMC has executed very well amid the upcycle. Management has also continued to emphasize that it believes the cycle is durable.

But, could its optimism have been priced into its stock amid the massive capex buildup? An analysis of its FCF yields is therefore instructive. TSM last traded at an NTM FCF yield of 1.33%. Notably, the stock has already fallen close to 40% from its January highs (also a significant bull trap). Furthermore, TSMC's FCF yield is even lower than NVIDIA's (NVDA). NVDA stock NTM FCF yield has improved to 3% due to its recent drubbing.

So, the market seems to have already priced in its optimism for FY21-22. Now, the market could be digesting those gains as Taiwan Semiconductor heads to a slower-growth FY23 next year as it laps challenging comps from 2022. The market is forward-looking.

Growth Could Be Slowing Down

TSMC revenue change % and gross margins % consensus estimates(S&P Capital IQ)

Notably, the consensus estimates suggest that TSMC's revenue growth could peak in FQ2 (ending June quarter) before it decelerates through FY23. In addition, the consensus estimates also indicate a normalization in its gross margins through FY23, thus impacting its profitability, given its inherent operating leverage. In other words, TSMC could likely be operating at near-term peak profitability.

TSMC reported revenue growth of40.1% YoY and 0.3% MoM in April as growth continues to be robust. However, we believe that the market has been pricing in the deceleration in its growth astutely. Therefore, if TSMC is operating at peak margins, it's justifiable for the market to de-risk TSM stock to moderate its valuations.

Furthermore, DIGITIMES reported recently that TSMC has also been feeling cost pressures, as it reported TSMC's intention to hike pricing quotes by 5-9% in 2023. DIGITIMES added (edited):

However, market observers have been skeptical about the prospects for wafer foundries, with many believing the peak will be over at the end of the year. These observers believe wafer foundry prices could then take a turn. The sources noted that the main reason for TSMC to raise the price again in January 2023 is that expenditures for production expansion in the US and Japan have far exceeded expectations. Originally, the cost of setting up factories overseas was expected to be four to five times that in Taiwan, but the global inflation in recent months has added pressure. -DIGITIMES

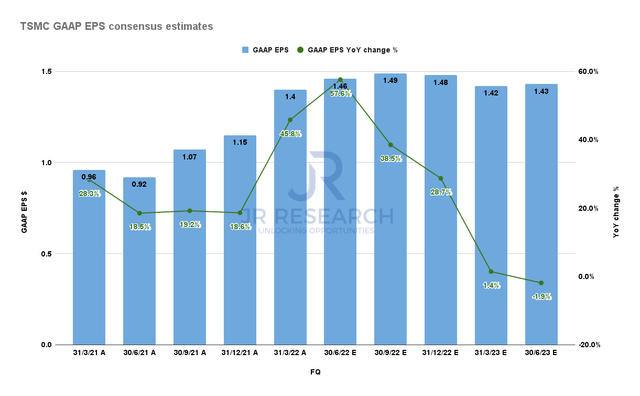

TSMC GAAP EPS consensus estimates(S&P Capital IQ)

Therefore, we believe that the market has been trying to price in the likely impact on its gross margins, which could have a marked impact on its profitability. In addition, as seen above, TSMC's GAAP EPS growth is expected to moderate significantly from its possible peak in Q2 and through FY23. Therefore, we think it's becoming more apparent that the market believes that TSMC's growth and profitability growth could start to moderate from H2'22.

Is TSMC Stock A Buy, Sell, Or Hold?

TSMC stock price chart(TradingView)

The consolidation zone over the last 12-14 months has been resolved. It was a distribution phase. The market makers have successfully drawn in the buyers allowing them to unload their massive gains from the rapid run-up in 2020.

TSM stock FCF yields also corroborate our view that the market had already priced in potential peak profitability in its upcoming Q2 report well before it even occurred. Furthermore, the January 2022 bull trap (post-FQ4 earnings) was highly remarkable. It drew in the final round of "dip buyers" before the market makers unloaded their holdings dramatically.

As a result, the $100 level is the new critical resistance level that could impede TSM stock momentum in the near term. Moreover, its FCF yield remains much higher than its 5Y mean. Therefore, we believe a near-term re-rating is highly challenging if the market expects TSMC's profitability to peak in FQ2 and fall after that.

Therefore, we are convinced that the risk/reward profile has weakened dramatically even as the stock nears a short-term bottom.

We urge investors to watch for a re-test of its current bottom before attempting to add exposure. Otherwise, the fall to its next support could induce even more pain.

Consequently, we revise our rating on TSM stock from Buy to Hold.

Comments