Summary

- NIO's stock price has been obliterated, dropping by a staggering 85% from its ATH in 2021.

- Ironically, while the bulls were out in force when the stock was trading in the stratosphere, many investors are screaming sell now.

- NIO is a unique company with excellent growth prospects and significant profitability potential.

- Moreover, at around 1.2 times forward sales estimates NIO's stock is dirt cheap now.

- As uncertainties fade, sentiment should improve, and NIO's stock will likely move much higher in the coming years.

Despite the recent indiscriminate selling, NIO may have bottomed, and its stock is a strong buy now. Bulls were out in force when the stock skyrocketed to the absurdly overbought $50-$70 range. However, now that the stock has returned to ten bucks, many are screaming to sell. On the contrary, I think now is the time to buy NIO's stock for the long term. The company has incredible revenue growth potential and excellent profitability prospects. NIO should continue increasing sales and improving profitability as the company moves forward, and its stock should appreciate considerably in the coming years.

NIO - Then and Now

There is a massive difference between buying into NIO around its highs in 2021 and now. At its height in 2021, NIO was worth nearly $100 billion. However, the company's market capitalization has dropped to only $18 billion. The company brought in approximately $5.6 billion in revenues in 2021. Thus, the stock was trading at an absurdly high valuation of roughly 18 times forward sales estimates at its peak. Consensus revenue estimates are for approximately $14 billion in 2023, illustrating a much more affordable stock that is only trading at around 1.24 times forward sales now. I'll go further than that and say that NIO is dirt cheap at this valuation, which is why you want to own this stock.

China's Government Support For NIO

NIO is one of the top EV producers in China, and EVs are critical to China's future. Also, China is by far the most significant car market in the world and plans for EVs to account for 40% of all vehicle sales by 2030. When NIO ramped up production in 2020, the company ran into severe headwinds due to COVID-related effects. NIO was in financial trouble, and the Chinese government stepped in, acquiring a 17% stake in the company, providing the necessary liquidity required to continue operations. Therefore, there is much misguided fear about the Chinese government hurting companies. On the contrary, when it comes to NIO, we see that the government is eager to help.

China's Massive EV Market

China's global passenger EV sales share has surged from 26% in 2015 to 48% in 2021. Moreover, the country's share increased to 56% in the first half of 2022, and analysts anticipate the EV share to expand to around 60% by year-end.

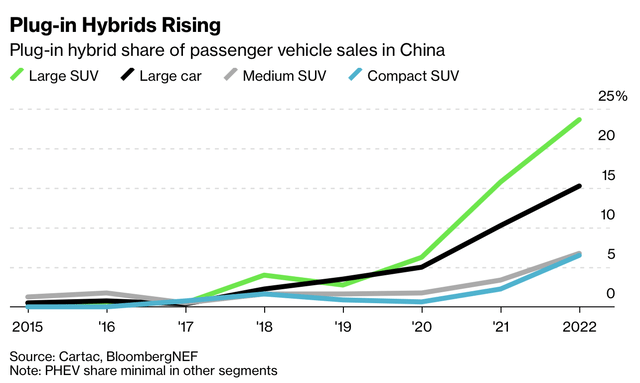

China EV sales (Bloomberg.com)

Increasing numbers of large SUVs and large cars in China are now EVs. The percentage of large SUVs attributable to the EV sector is approaching 25% in China (15% for large vehicles). China's massive EV segment is set to grow rapidly, and NIO is well-positioned to capitalize on the expansion in the coming years.

NIO's Growth Opportunity

NIO's popular ET7 sedan and ES7 large SUV are among the country's top-selling EVs and should continue experiencing robust demand. The ET7 has a range of approximately 290-555 km, goes from zero to 100 km in 3.8 seconds, and has a top speed of around 200 km/h. The car also has a five-star safety rating and is rolling out in Europe (Germany and the Netherlands). Moreover, NIO recently launched its new ET5 smaller and cheaper sedan in China, and sales of the popular vehicle should take off globally.

Last month (October 2022), NIO delivered 10,059 vehicles, a whopping 174% increase YoY. Deliveries comprised approximately 6,000 premium smart electric SUVs, including 2,814 ES7 vehicles. Also, around 4,000 premium smart electric sedans were sold, including roughly 3,000 ET7s and 1,000 ET5 vehicles. In October, NIO unveiled ET7, EL7, and ET5 cars for the European markets. These vehicles are available for order in Norway, Germany, the Netherlands, Denmark, and Sweden. NIO is gradually moving into the European market, a phenomenon that should supplement its domestic growth story nicely as the company moves forward in future years.

NIO's Recent Earnings

Despite a slight miss of $0.14 in non-GAAP EPADS, NIO's revenues came in at $1.83 billion last quarter (32.6% increase YoY), beating analysts' estimates by $50 million. Despite a challenging macro environment, NIO expects to deliver between 43,000 and 48,000 vehicles in Q4, representing a YoY increase of approximately 72-92%. Moreover, NIO expects Q4 revenues of $2.44-$2.7 billion, roughly a 75-94% rise over last year. These were excellent results, and the company's guidance was far from disappointing, implying that NIO's powerful growth story should continue as we advance.

NIO's Valuation Is Dirt Cheap Now

NIO is a high-growth company that prioritizes expanding car production and other operations. The company is also involved in the penetration of the European EV market. Therefore, we should not expect NIO to be profitable now, and it may not report positive EPS for several years. Nevertheless, NIO's remarkable growth story implies that the company has significant profitability potential, and just like any other high-growth company, we can evaluate NIO's valuation based on its sales.

NIO's Revenue Projections

Revenue estimates (SeekingAlpha.com )

NIO's revenues are projected to skyrocket by about 90% to roughly $14 billion next year. Then, we should see revenue growth moderate to about 30-45% in 2024 and lower double digits after that. However, consensus analysts' revenue growth of approximately 13-14% in 2025 and 2026 may be lowballed, and I expect the company will do better. Once the slowdown concludes and sentiment improves, 2025 and 2026 revenue estimates may rise to 15-25%.

Still, with a market cap of around $18 billion, NIO's forward P/S multiple is roughly approximately 1.24 here, remarkably low for a company in NIO's position. For instance, if we look at Lucid (LCID), a comparable EV company based in the U.S., its forward P/S multiple is between 7-8 now. Rivian (RIVN), another young EV company, trades at a forward P/S ratio of about six currently. Additionally, unlike NIO, Lucid and Rivian still need to prove that they can mass-produce vehicles. Nevertheless, these EV manufacturers trade at substantially higher multiples than NIO, implying that NIO's stock is dramatically undervalued now. As the slowdown concludes and uncertainties fade, NIO's P/S ratio will likely increase, enabling the company's stock price to move much higher.

What Wall Street Analysts Think

NIO price targets (SeekingAlpha.com)

Wall Street's average one-year price target is around $20.30, roughly 93% above NIO's current stock price. Moreover, higher-end price targets go up to nearly $35, illustrating a price target almost 250% above current levels. Even the lowest price target of $12.34 is roughly 20% above NIO's deeply depressed levels. This dynamic implies that NIO's stock is highly undervalued now and is likely to go significantly higher as NIO advances.

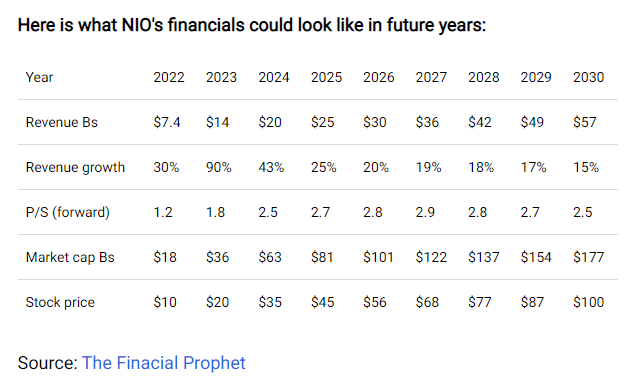

Due to NIO's remarkable revenue growth and exceptionally long growth runway, we should see revenues increase dramatically, possibly reaching approximately $55-$60 billion by 2030. Simultaneously, sentiment should improve as uncertainties fade, leading to P/S multiple expansion. I'm keeping my P/S ratio projection relatively modest, but even if the company's P/S ratio remains below 3, we can see NIO's stock price appreciate considerably in the coming years. Provided my projections, we may see around a 10X return in NIO's stock by 2030.

Risks to NIO

Despite my bullish outlook, there are various risks to my thesis. The company could run into various production issues and may not reach the production capacity I envision in time. Moreover, NIO's vehicles may experience a drop-off in demand, in which case the company's share price would suffer. NIO remains an elevated-risk investment, but there is substantial reward potential if everything goes right.

Comments