Net inflows into U.S. equities by retail investors continued to climb over the past week as the stock market started the new year in a buoyant mood, but data analysts at Vanda Research said the pace of purchasing could easily slide if bullish momentum stalls.

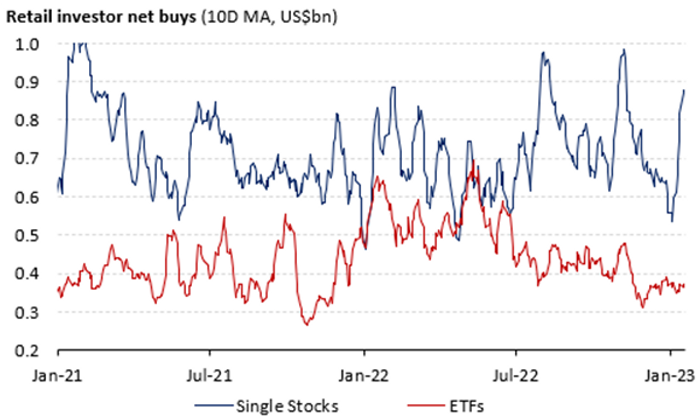

Marco Iachini, senior vice president of Vanda Research, attributed the January’s jump in retail purchasing of U.S. stocks to the muted purchases of exchange-traded funds, which indicate a sign of low conviction in the long-term prospects of financial markets (see chart below).

“We believe the January market rally is once again stemming from a bout of institutional investor short covering and rising equity demand from retail investors. However, despite the rebound in purchases, the aggregate retail flow has not yet recovered to previous highs, meaning that we’re still in a longer-term downward trajectory when it comes to retail participation,” wrote analysts led by Iachini, in a Thursday note.

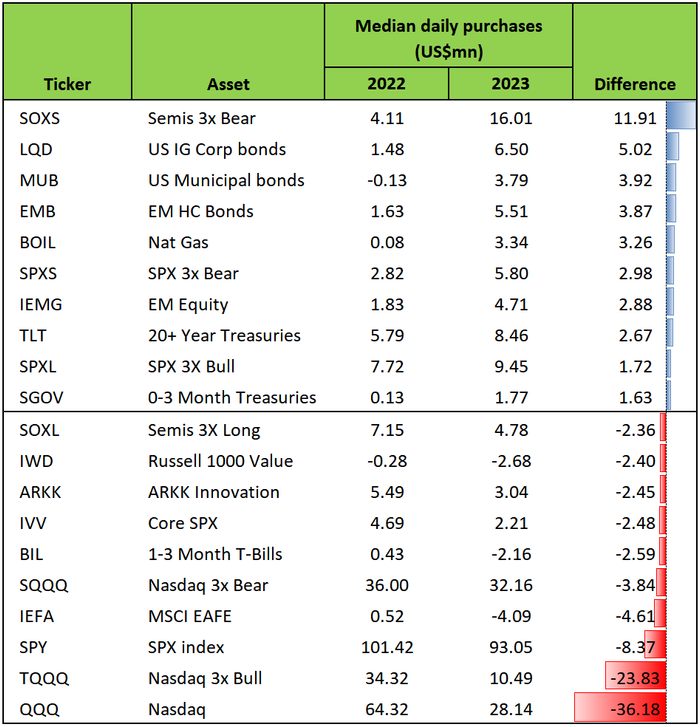

The table below shows ETFs are currently experiencing the biggest flow divergences since 2022. “The three bottom ETFs are the last two years’ more popular vehicles,” said analysts, while the biggest gainers, such as Direxion Daily Semiconductor 3X Bear, have a defensive tilt to them.

Iachini and his team also expect retail investors to “maintain high participation levels” in single stocks when companies comprising over half the S&P 500‘s market value report results in the next two weeks. That includes Microsoft Corp.,which will step up to deliver its second quarter of fiscal 2023 report Tuesday, followed by Elon Musk’s Tesla Inc. and The International Business Machines Corporation (IBM) on Wednesday and Intel Corp. on Thursday. Apple Inc. and Google-parent Alphabet Inc. will report in the following week, according to FactSet.

“[Tesla] stock remains a bellwether of overall retail sentiment/health, in our view,” Iachini said. “Retail investors are buying the EV-maker’s shares at one of the widest margins relative to their history and other securities.”

With 11% of S&P 500 companies reporting actual fourth-quarter results as of Friday, 67% of them have reported earnings per share (EPS) above estimates, while 64% of the companies have reported a positive revenue surprise, said John Butters, senior earnings analyst at FactSet. EPS refers to net income divided by the number of shares outstanding, and could indicate how much money a company makes for each share of stock.

The blended earnings decline for the S&P 500 for the fourth quarter is 4.6%, said Butters in a Friday note. If that is the actual decline for the quarter, it will mark the first time the index has reported a year-over-year decline in earnings since the third quarter of 2020 which recorded a slump of 5.7%.

U.S. stocks finished higher on Friday, with help from Netflix Inc. and Alphabet which jumped 8.5% and 5.3%, respectively, oncorporate news. The Nasdaq Composite rallied 2.7%, booking a weekly gain of 0.6%. The Dow Jones Industrial Average was up 330 points, or 1%, to end at 33,375. It fell 2.7% for the week and notched its worst weekly performance since September 2022. The S&P 500 rose 1.9% on Friday, but posting a weekly loss of 0.7%, according to Dow Jones Market Data.

Comments