After a strong Q2 performance, cloud computing company ServiceNow (NOW) saw a decline of nearly 2.7% in after-hours trading on Thursday. However, looking at its performance over the past year, NOW not only outperformed the market but also emerged as one of the most favored targets in the entire SaaS industry. In the era of AI, the company has further strengthened its advantages through various external collaborations.

ServiceNow (NOW) remains one of the top-tier tech companies worth holding, even amid the current market pullback.

Q2 Highlights

The company's Q2 revenue reached $2.15 billion, a year-on-year growth of 23% (adjusted for exchange rates, the growth was 22.5%), surpassing the market's expectation of $2.13 billion.

The subscription revenue (SaaS) amounted to $2.075 billion, with a year-on-year growth of 25% (adjusted for exchange rates, the growth was 25%), exceeding the previous upper guidance.

The remaining performance obligation (PRO) stood at $14.2 billion, a year-on-year growth of 24% (adjusted for exchange rates, the growth was 22.5%), with the current remaining performance obligation (cPRO) at $7.2 billion.

The adjusted net profit reached $490 million, corresponding to an adjusted net profit margin of 22.6%. Earnings per share after adjustments were $2.37.

Q3 Guidance

The subscription revenue is expected to be between $2.185 billion and $2.195 billion, with a mid-range year-on-year growth of 25.8%. The adjusted operating margin is forecasted at 27%, and cPRO is expected to grow by 25.5% year-on-year. Moreover, the management has revised the full-year guidance for 2023, raising the mid-value of annual subscription revenue guidance by $95 million, resulting in a projected range of $8.58 billion to $8.60 billion, with a mid-range year-on-year growth of 24.6% (adjusted for exchange rates, the growth is 24%), and the adjusted operating margin guidance is raised by 0.5 percentage point to 26.5%.

Investment Highlights

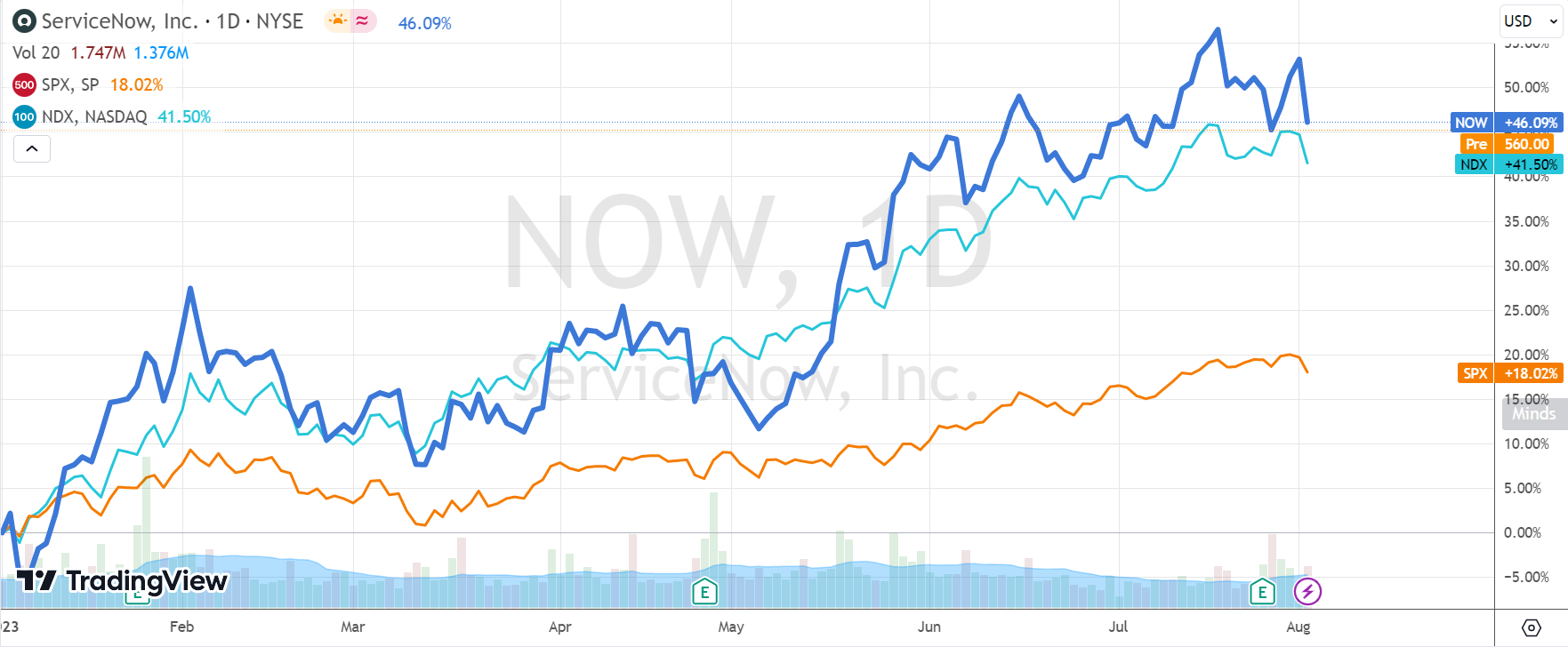

Despite the 2% post-market drop, it is undeniable that ServiceNow (NOW) has outperformed the $S&P 500(.SPX)$ this year, even surpassing $NASDAQ 100(NDX)$

The current pullback does not indicate that investors are abandoning the stock. On the contrary, it remains highly favored in the SaaS industry.

Firstly, the performance improvement is supported by new order growth. In Q2, there were 70 net new contracts with an annual value exceeding $1 million, a 30% YoY increase. The number of customers with an annual contract value (ACV) exceeding $2 million reached 45, a 55% YoY increase. Additionally, the customer renewal rate for the quarter was 99%, indicating strong customer loyalty.

Furthermore, the emergence of AI has expanded the company's opportunities and product range through collaborative efforts with companies like $NVIDIA Corp(NVDA)$ $Accenture PLC(ACN)$ , KPMG, and $Cognizant Technology Solutions Corp(CTSH)$ to accelerate the application of AI technology in their products.

Cost reduction efforts have shown significant results, and in addition to effective spending control, the company has initiated its first stock repurchase plan. With continuous improvement in profits, the company's cash flow has reached record levels, with Q2's free cash flow reaching $450 million, supporting the stock buyback plan worth approximately $1.5 billion.

Comments