FatCamera/E+ via Getty Images

Introduction

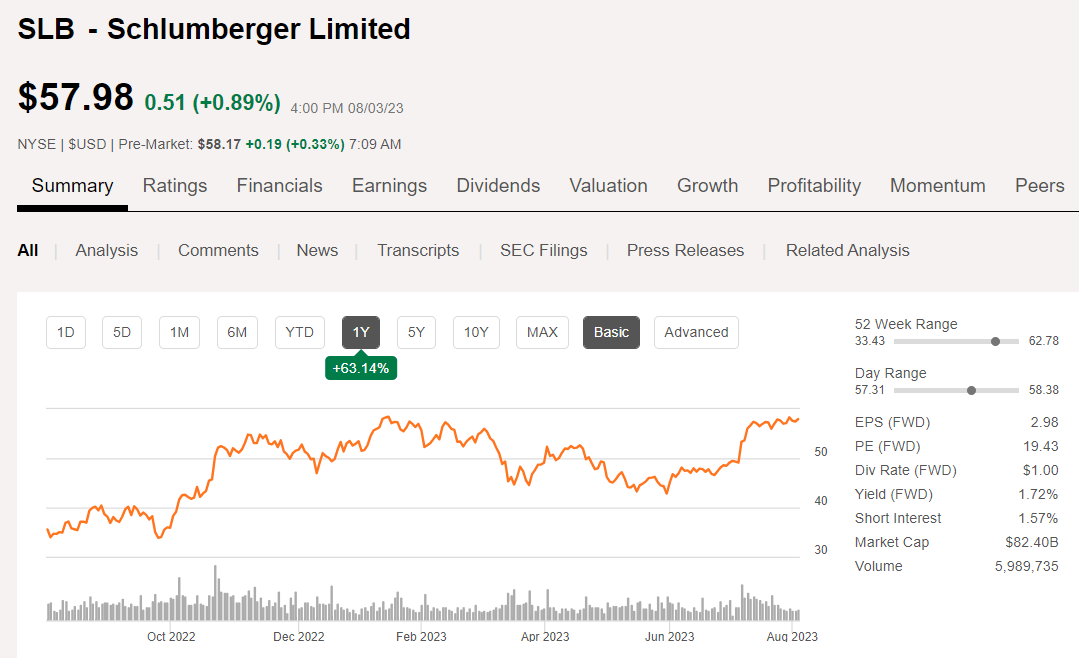

Schlumberger Limited (NYSE:SLB) missed on the top line by $112 mm, but beat on the bottom line by a penny in their most recent Q2 earnings release. This news was clearly priced into the stock, as the trading has been flat since. There was a window from late April to early July where it was trading at a substantial discount to today's price, in the mid-$40's, and it was a frequent topic of discussion in my investing group. That window has now closed for this cycle, and I expect the easiest path is higher for the stock in the market we see developing over the next few months.

SLB price chart (Seeking Alpha)

The task before us now is to decide if the company remains investable at today's much-improved pricing. In this discussion, we will look at the macro environment for OFS companies, and then project what this may mean for Big Blue.

I have discussed SLB many times, and anyone who is unfamiliar with them should access those older articles for background.

The next few years for OFS companies

There are a couple of key themes that will favor this segment, that still are in the early phases.

1. A new offshore exploration and development cycle is beginning. Recent discoveries in West Africa- Ghana, and Niger have resulted in a clear tightening of the supply of vessels built to explore for "Elephants." 6th and 7th generation drill ships have much superiority-hook-load capacity, standpipe pressure, pump capacity, dual activity, etc., and day rates have been rising rapidly. This also extends to countries on this side of the Atlantic. From the GoM to the Guyana/Suriname basin, all the way down to Brazil's Santos basin, modern drillships are being put to work in the hunt for oil "Pachyderms." Offshore is where the big money is made in OFS and SLB rules this sector. Olivier le Peuch, CEO of SLB commented on the outlook for the offshore cycle-

Furthermore, we continue to witness a broad resurgence in offshore driven by energy security and regionalization. Operators all over the world are making large-scale commitments to hasten discovery, accelerate development times, and increase the productivity of their assets.

This is resulting in increased infill and tie back activity in mature basins, new development projects both in oil and gas, and support for new exploration. With this backdrop, we anticipate more than $500 billion in global FIDs between 2022 and 2025, with more than $200 billion attributable to deepwater. This reflects an increase of nearly 90% when compared to 2016-2019. These FID investments are global taking place in more than 30 countries, and we are seeing the results with new projects in offshore basins across the world. T

2. The sources of excess crude supply-the U.S. shale patch, the Middle East, and Russia are going through various scenarios that will impact their ability to produce at previous levels for the foreseeable future...if ever. Shale is suffering from a decline in acreage quality that is only just beginning to manifest itself, as we have discussed recently. Output over the last couple of years has been maintained through technology and DUC withdrawal, and those sources of supply are hitting some limits. The Middle East-The Emirates, Saudi, and even Iraq and Iran are recapitalizing after years of underinvestment. All will be boosting output, but it will be several years before renewed efforts to bring on new fields bear fruit. Russia... well there isn't really a lot to say about them in this context. No Western OFS companies are supporting them and it remains to be seen if they will be able to maintain production without western support.

All of this is good for the technology that OFS companies have developed and it's the international growth that underpins the investing case for SLB. Ok, New Exploration, Middle East Recapitalization, and Technology are a three-pronged platform that will drive profits for SLB.

Le Peuch, speaks to the key elements of the international business cycle-

In the international markets, the investment momentum of the past few years is accelerating. This is supported by resilient long-cycle developments in Guyana, Brazil, Norway, and Turkey; production capacity expansions in the Middle East, notably in Saudi Arabia, UAE, and Qatar; the return of exploration and appraisal across Africa and the Eastern Mediterranean; and the recognition of gas as a critical fuel source for energy security and the energy transition.

In the Middle East, this is resulting in record levels of upstream investment. From 2023 to 2025, Saudi Arabia is expected to allocate nearly $100 billion to upstream oil and gas capital expenditure, a 60% increase compared to the previous three years, as they invest to attain a maximum sustained production capacity of 13 million barrels per day by 2027. Several other countries in the region have also announced material increases in capital expenditures that extend beyond 2025.

The case for SLB

Big Blue is a colossus, larger than all but the biggest of the oil companies, and an Enterprise Value 2X its nearest rival, Halliburton Company (HAL). SLB has a couple of advantages that will bolster profits in the coming up cycle for OFS. One Subsea is a Deep Water delivery juggernaut with a total product/service delivery mix that is particularly focused on the services that will be in high demand as the cycle accelerates.

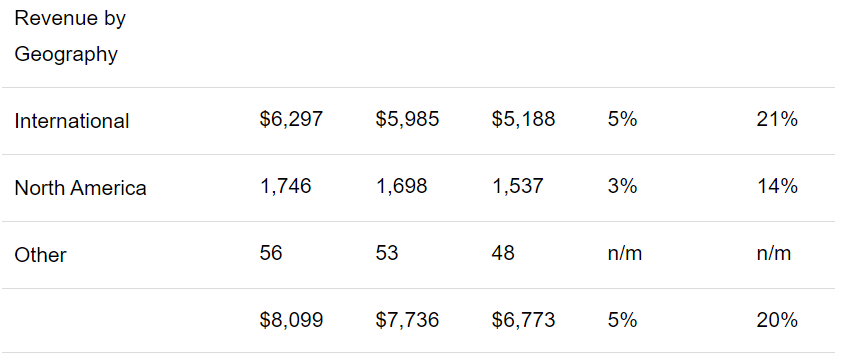

SLB's international footprint already in place will be a springboard for enhanced revenues and profits as the cycle ramps up. As you can see from the snapshot below, International Revenue already outpaces North America nearly 4:1. Growing international revenue will drive this number higher.

SLB Revenue by Geography (Seeking Alpha)

Key wins in Q2

The company is executing across its portfolio with a number of key wins around the globe.

Well construction

- In Mexico, through its reference agreement process, PEMEX awarded SLB contracts with a total value of approximately $1 billion over the next two years for land and shallow-water exploration and development.

- In Saudi Arabia, SLB received a contract award from Saudi Aramco for directional drilling services for the world’s largest oil and gas fields. On both land and offshore, SLB will deliver directional drilling and digital drilling solutions and logging-while-drilling services.

- In Qatar, Qatargas awarded SLB a five-year exclusive contract with an optional five-year extension for the provision of unitized Cameron wellhead and tree systems. The equipment will be installed in 50 offshore and five onshore wells in the North Field South project.

- In Brazil, Petrobras awarded a contract to OneSubsea to supply critical subsea equipment to assist in the development of the Búzios pre-salt field in the country’s prolific Santos Basin. SLB will supply 15 subsea trees and electrohydraulic distribution units to serve the Búzios-11 project, set to enter production in 2027 via the P-83 floating production, storage, and offloading vessel.

- Offshore Egypt, bp and its joint venture partner Wintershall Dea have awarded Subsea Integration Alliance an engineering, procurement, construction, and installation (EPCI) contract for the Raven infill project.

- In the UK North Sea, BP awarded OneSubsea a contract for the supply of subsea dual-bore trees, as part of its ongoing infill drilling program in the Schiehallion/Loyal fields west of Shetland.

- In Turkey, Turkish Petroleum awarded SLB an EPCI contract for Phase 2 of the Sakarya field development, offshore Turkey in the Black Sea.

Technology and Performance

- In Mauritania, the XR-Perf™ expanded-range wireline perforating system restored production in a deepwater well operated by bp by enabling the perforation of more than 300 meters in eight runs without incident or nonproductive time.

- In Libya, SLB executed the first treatments utilizing the OneSTEP EF efficient, low-risk sandstone stimulation solution for Waha Oil Company to improve the well influx from a fractured reservoir, mitigate the increasing water production in the field.

- Offshore Malaysia, the integrated solution of Gyrodata Quest gyro-while-drilling (GWD) system together with PowerDrive X6™ rotary steerable system delivered the longest extended-reach-drilling well in the country, the first integrated deployment since SLB’s acquisition of Gyrodata Incorporated.

Digital

- In Brazil, SLB was awarded a five-year contract by Petrobras for an enterprise-wide deployment of its Delfi digital platform. The contract scope facilitates Petrobras’ digital transformation from exploration, development, and production operations, including moving subsurface workflows to the cloud to significantly accelerate decision making. The award represents one of Petrobras’ largest investments in cloud-based technologies.

- In Ecuador, Empresa Nacional del Petróleo ("ENAP") has awarded SLB a three-year software-as-a-service contract, granting ENAP access to the advanced technology solutions in the Delfi digital platform to enhance its operations and respond more efficiently to daily challenges.

- In India, Cairn Oil & Gas, Vedanta Limited selected SLB and Cognite to deploy an industrial DataOps platform at the enterprise level. The project scope includes implementation of a consolidated and unified data enterprise platform for reservoir management in the Rajasthan basin, with the aim of enhancing efficiency, leveraging data science and analytics, and enabling the development of novel applications to optimize reservoir and production workflows.

- In Kuwait, Kuwait Oil Company ("KOC") utilized Neuro™ autonomous solutions, which included the autonomous downhole control system, DrillOps™ Automate, DD Advisor coupled with well construction rig equipment, the AxeBlade ridged diamond element bit, and the PowerDrive Orbit G2™ rotary steerable system. Optimization through autonomous directional drilling capabilities delivered a 90% increase in rate of penetration, (ROP) and a 37% increase in steering effectiveness, saving over $500,000 and eight rig days compared to the authorization for expenditure-AFE.

- In Malaysia, SLB has incorporated Neuro autonomous solutions to deliver autonomous directional drilling in one of PETRONAS Carigali Sdn Bhd’s ("PCSB") operated asset development campaigns.

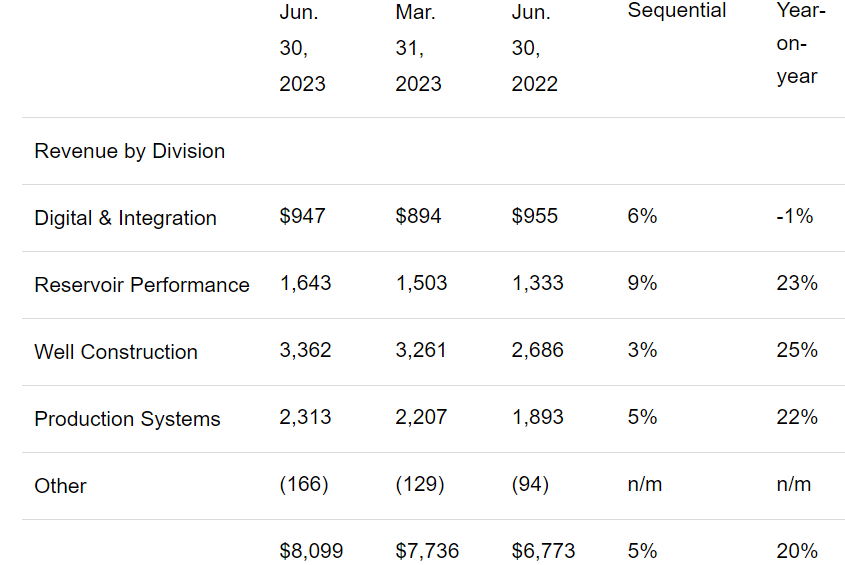

SLB Revenue by Division (Seeking Alpha)

These new awards underpin the fact that SLB's entire business is improving incrementally QoQ, and and at double-digit rates YoY. Collectively they represent 10's of billions in future revenue, and its impressive to realize these awards came in a single quarter. Finally on a YoY basis the most service intensive business lines are up evenly and contributing to revenue growth. It was noted in the call that underperformance in Digital YoY was driven by overperformance the year before and some special revenue streams that did not repeat.

A catalyst for SLB- One Subsea Alliance

As we have discussed, Olivier Le Peuch, CEO of SLB has confirmed the start of an upcycle in offshore, mostly deep water development that will last at least 3-5 years. Perhaps longer. Estimates like this get a little spongey when you try to look too far out, but Le Peuch identified $500 bn that will be spent along these lines by 2025, with $200 bn for deepwater. A big chunk of this will land on SLB's balance sheet.

This is what the One Subsea Alliance, was formed to do. Consisting of SLB's core Cameron assets, Subsea 7's EPIC, Installation and Commissioning services, and Helix Energy Solutions Robotics, vessel support, and intervention capabilities, this asset-lite alliance gives SLB a considerable advantage in pursuing this kind of work.

SLB One Subsea Alliance (SLB)

Q2 and Guidance

Revenue of $8.10 billion increased 5% sequentially and 20% year-on-year. GAAP EPS of $0.72 increased 11% sequentially and 7% year-on-year. EPS, excluding charges and credits, of $0.72 increased 14% sequentially and 44% year on year. Net income attributable to SLB of $1.03 billion increased 11% sequentially and 8% year on year. Adjusted EBITDA of $1.96 billion increased 10% sequentially and 28% year on year. Cash flow from operations was $1.61 billion and free cash flow was $986 million. Board approved quarterly cash dividend of $0.25 per share.

Debt fell YoY by $900 mm, landing in Q-2 at $10.1 bn. Capital investments, inclusive of CapEx and investments in APS projects and exploration data, were $622 million in the second quarter. For the full-year, they are still expecting capital investments to be approximately $2.5 billion to $2.6 billion. SLB repurchased 4.5 million shares during the quarter for a total purchase price of $213 million. They continue to target returning~ $2 billion to shareholders this year between dividends and stock buybacks.

Guidance. Free cash flow in the second half of the year will be materially higher than the first half. SLB expects to continue year-on-year revenue growth of more than 15% and adjusted EBITDA growth in the mid-20s. Specifically in Q3, they are looking for revenue to grow by mid-single digits in the international markets, with all international geographical areas growing sequentially, led by the Middle East and Asia. In contrast, North America revenue is expected to be slightly down. Their focus will be on the quality of revenue, harnessing operating leverage, and further technology adoption. SLB expects global operating margins to further expand by more than 50 basis points sequentially.

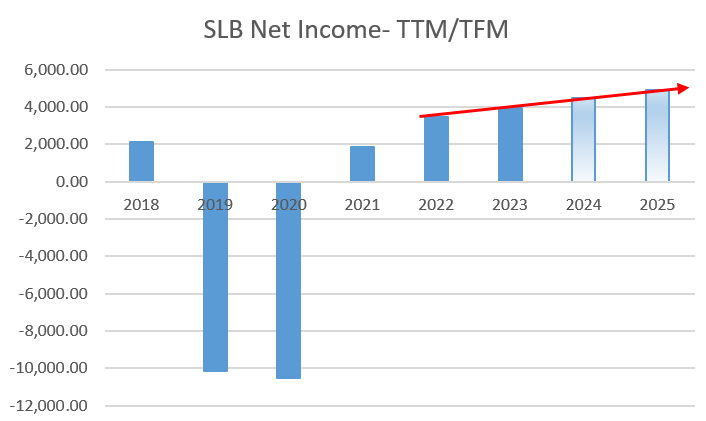

With a rising market and increased service intensity, I don't think I am going too far out on a limb here. Obviously the projected NI we have in the gradient blue bar depends on the beneficial market we see developing, for which I've hopefully made a case in this article.

SLB Net Income (Seeking Alpha/Chart by Author)

Risks to the thesis

As always we must note perils abound. It won't shock me to see further releases from the SPR to hold down prices. The temptation to put another million barrels a day on the market has to be building in the cloistered halls of the the D.C. circus. In that event, the inevitable will still come, but it will slip to the right on the Days vs Depth curve.

China demand could unravel. They are still the factory to the world and if they sneeze, the world may catch a cold.

In stead of the gradually increasing oil price, topping out in the $90-100 range, we could have a shortage-driven spike to the mid-$150's. These are always demand killers that put an end to an upcycle. This can't be totally discounted in the jumbled energy world in which we now live.

Your takeaway

Big Blue is now trading at 11.5X EV/EBITDA. That's not cheap by any measure, but remember we are getting growth from SLB, so multiples are going up. The 31 analysts who cover SLB rank it as a buy with targets that range from $57-73, with a median of $65. I think those numbers are actually a little stale and will be revised higher, but it might take the stock a while to catch up. EPS projections for Q3, 4 are $0.77 and $0.86 respectively. I think SLB is in a beat mode, so I am adding $0.02 to Q3, and $0.05 to Q4 respectively. Those still fall within those range estimates, so the short term upside could be limited.

All of that said, I think Schlumberger Limited is nearing a short-term plateau, having made a huge-richly deserved, parabolic move higher in a 7-day period in early July. It has traded sideways since, and absent a sharp move higher in Brent, I don't think I would add to my position at current levels. If we were to revisit the low $50's, I would add incrementally for long-term growth and rising income.

Nearing $60, we rate SLB a Hold.

Comments