Baytex Energy Corp. is undervalued, trading at a 35% discount to book value, with strong fundamentals and catalysts in both U.S. and Canadian markets. Baytex's acquisition of Ranger Oil in the Eagle Ford basin has diversified its production, now over half of its daily output. The company is focused on reducing debt and returning capital to shareholders, with a free cash flow yield of 18% and attractive valuation multiples. BTE rates a strong buy for investors anticipating higher oil prices and improved market conditions for upstream E&P operators. FG Trade Latin/E+ via Getty Images Introduction Baytex Energy Corp. (NYSE:BTE) has traded in a fairly tight range for about a year now, oscillating between slightly less than $3.00 and $4.00 p

Fluidsdoc

I am an oilfield veteran of 38+ years. Retired from Schlumberger since 2015. My background is drilling and completion fluids. I have authored a number of technical papers on completion topics.

0Follow

693Followers

0Topic

0Badge

Baytex Energy: A 'Scratch And Dent' Standout

Baytex Energy: A 'Scratch And Dent' Standout

Liberty Energy: Democratizing Energy Around The World (Rating Upgrade)

Liberty Energy Inc. offers diverse energy exposure and is poised for growth with the incoming administration's favorable energy policies, making it a Strong Buy. Despite recent financial setbacks, Liberty's strategic investments and ESG initiatives, like the Bettering Human Lives Foundation, highlight its long-term value and commitment to societal impact. The company's balance sheet remains robust, with disciplined capital deployment and a focus on delivering healthy free cash flow and shareholder returns in 2025. Market trends suggest a rebound in completions activity and pricing improvements, positioning LBRT stock for potential upside as the energy sector stabilizes. golero/E+ via Getty Images Introduction You want crude oil exposure? Liberty Energy Inc.'s (NYSE:

Liberty Energy: Democratizing Energy Around The World (Rating Upgrade)

Kosmos Energy: Scratched And Dented, But Still A Strong Buy

Kosmos Energy (KOS) has faced challenges but is poised for growth with the upcoming start of the Tortue LNG project, lower capex, and increased cash flow. Operational issues at Winterfell and Jubilee, and the FID delay for Tiberius, have been offset by positive developments in other projects and debt rescheduling. The balance sheet is stronger with new senior notes, and reduced capex will allow for debt reduction and potential shareholder returns by 2026. Despite current market reactions, I maintain a Strong Buy rating for KOS, with a price target of $8.00-$10.00 as cash flow improves. FatCamera/E+ via Getty Images Introduction Kosmos Energy, (NYSE:KOS) has had a tough year on Wall Street and in some of its GoM and Ghanan operations. The ma

Kosmos Energy: Scratched And Dented, But Still A Strong Buy

Civitas Resources Stock: Substantial Upside Potential

Summary Civitas Resources, Inc. is a strong buy due to its aggressive M&A strategy, attractive valuation multiples, and substantial free cash yield. The company is leveraging its DJ and Permian Basin assets, focusing on cost reduction and production efficiency, with significant shareholder returns. Civitas Resources' hedging strategy ensures cash flow stability amidst commodity price fluctuations, aiding in rapid debt reduction and potential share buybacks. Investors with modest risk tolerance should consider CIVI for capital appreciation and exceptional free cash yield at current prices. georgeclerk/E+ via Getty Images Introduction It's not surprising to me that the E&P universe was so ripe for consolidation, beginning a couple of years ago. Over the past couple of years, a couple

Civitas Resources Stock: Substantial Upside Potential

Imperial Oil: Taking A Pass, There's A Canadian Heavy Oiler We Like Better

Summary Canadian Natural Resources and Imperial Oil Limited have outperformed smaller heavy oil cohort members on an EV/EBITDA basis. Imperial Oil's stock has seen significant returns, with price targets ranging from the $60s to the $80s. The company's production has been meeting or exceeding goals, with potential catalysts in 2025 including new projects and increased output. We rate IMO as a hold and think there are better opportunities in the heavy oil cohort. We discuss one briefly in this article. Now lemme tell ya somethin...about oil sands. Ugur Karakoc Introduction As illustrated by the graphic below, at least two members of the Canadian heavy oil cohort have had a good first half of 2024. I refer to Canadian Natural Resources (CNQ),

Imperial Oil: Taking A Pass, There's A Canadian Heavy Oiler We Like Better

Patterson-UTI: The Worm Has Turned In Gas

Summary Patterson-UTI Energy has been struggling due to low commodity prices, but improvements in the natural gas market could reverse the trend. The company offers a range of services in the drilling and fracking sectors, and its cash conversion rates are among the top in the industry. The potential decline in shale production and increasing demand for gas in electricity generation and industrial usage could benefit PTEN. We rate PTEN as a buy at current levels. A pretty sight! grandriver Introduction Patterson-UTI Energy (NASDAQ:PTEN) has been treading water for most of this year as rig counts have suffered and frac spreads have gone to the house. The problem, of course, has been the slow withering of commodity prices, particularly on th

Patterson-UTI: The Worm Has Turned In Gas

Atlas Energy Solutions: The Road Must Roll!

Summary Atlas Energy Solutions Inc. is a locally sourced producer of high-grade sand for fracking and is introducing a step-change in last mile sand logistics with the Dune Express conveyor belt. Analysts have a bullish outlook for Atlas, with estimates for Q4 EPS slightly above Q3's and estimates for Q2 and Q3 2024 showing an increase. Atlas has several advantages, including the Dune Express conveyor belt, access to the Pecos aquifer for sand mining, and efficient last mile logistics using triple-trailers. We like Atlas, but are hoping for a slightly better price, so it's a hold at present. alvarez Introduction The case for Atlas Energy Solutions Inc. (NYSE:AESI) is not complex. The company is a locally sourced producer of high grade sand

Atlas Energy Solutions: The Road Must Roll!

Kosmos Energy: Santa's Bringing A Deal On This Beaten Down LNG Stock

Summary Kosmos Energy is currently trading at a discounted price, making it an optimal entry point for investors. The company's core thesis is the impending startup of the Greater Tortue Ahmeyim-GTA project offshore Senegal and Mauritania. Kosmos Energy has taken a 90% stake in the Yakaar-Teranga-Y&T field, which is expected to be larger than GTA and has strong market potential. We rate KOS as a strong buy at current prices but may look for a slightly better entry point, given present market conditions. Santa...Pssst. I'd like a full position in Kosmos Energy in my stocking. AlexRaths/iStock via Getty Images Introduction In my view, we are being given a gift by the market's current disdain for everything related to oil or gas. Burgeoning supplies of oil and gas, combined with demand fe

Kosmos Energy: Santa's Bringing A Deal On This Beaten Down LNG Stock

Dril-Quip: Ready For Liftoff

Summary Dril-Quip, Inc. is a company focused on complementary operations and sales items in deepwater, carbon capture, and offshore wind farms. The company's stock is at a recent low after missing on the bottom line in the recent quarter. Dril-Quip has a long runway for growth and may be a buy at current levels, especially if there is a major upcycle in offshore operations that we anticipate. We are calling a buy on Dril-Quip, Inc. at current levels for risk-tolerant investors. CHBD Introduction We haven't written up Dril-Quip, Inc. (NYSE:DRQ) previously, and that's a regrettable oversight on our part. It's a company with which I used to be very familiar due to their focus on deepwater connectors and liner hangers...the bits and bobs that m

Dril-Quip: Ready For Liftoff

Comstock Resources: When The Market Gives You Lemons

Summary Comstock Resources stock is down 20% due to warmer weather and high gas storage levels. New LNG plants set to open in 2024-2026 will create new demand for gas. The future investment case for Comstock Resources depends on higher gas prices and potential catalysts in the Haynesville region. CRK is in the buy zone at current prices. viafilms/iStock via Getty Images Introduction Comstock Resources (NYSE:CRK) is down 20% this month, following a decline back to the low-3's for Natty. Warmer weather and the prospects of more of the same, just crushed the stock. Then there are the relentless injections into gas storage, nearing what some call tank-top, with the addition of another 60 BCF last we

Comstock Resources: When The Market Gives You Lemons

Patterson-UTI: The Future's So Bright

Summary Patterson-UTI Energy has positioned itself for growth with strategic transactions and attractive free cash flow yield. Positive drivers are emerging for drilling to recover in the macro market, potentially leading to better times for the company. Patterson-UTI Energy's acquisitions and market position make it a solid investment case for long-term growth and moderate to increasing income. We rate Patterson-UTI Energy stock as a buy at current levels for investors with a healthy tolerance for risk. vvvita Introduction Patterson-UTI Energy (NASDAQ:PTEN) has revamped itself with two strategic transactions closed over the summer that could position it for growth in the coming year. The company is trading an attractive free cash flow yie

Patterson-UTI: The Future's So Bright

Enbridge: Oops, They Did It Again

Summary Enbridge's $14 billion acquisition has caused investors to abandon the stock, leading to a yield of over 8%. The gas market has experienced a solid gain, and if maintained, it could lead to enhanced profitability in the industry. Enbridge's move into the regulated utility space increases their utility base rate business and diversifies the company. ENB stock is a buy at current levels. jcamilobernal/iStock Editorial via Getty Images Introduction There's nothing like investing in diversifying assets to crash the price of a pipeline stock. The ink wasn't dry on my last article... hardly, before Enbridge (NYSE:ENB) management went and "Did it a

Enbridge: Oops, They Did It Again

Shell: Out Of The Doghouse

Summary The new Shell plc CEO, Wael Sawan, has taken a more realistic approach to the energy transition, acknowledging the ongoing need for oil and gas. Shell's focus on gas and deepwater markets, as well as its low breakeven costs, position the company well for future success. Shell's presence in EV charging and potential offshore reserves in Namibia could serve as catalysts for growth. Shell stock is a buy at current levels. alexei_tm/iStock via Getty Images Introduction One of the first articles I authored in Seeking Alpha was on Shell plc (NYSE:SHEL, OTCPK:RYDAF). It was a natural for me to cover the company, as I had worked closely with them for many years. To say I was a fan is an u

Shell: Out Of The Doghouse

Occidental Petroleum: Take Me Down To 45Q Funkytown

Summary Occidental Petroleum Corporation stock is trading sideways to down despite high oil prices and tepid analyst ratings. The company has been working to repair its balance sheet and has raised its dividend and implemented a share repurchase plan. Occidental's investment in carbon capture technology and potential revenue from carbon credits could be a catalyst for the company. We think Occidental Petroleum Corporation stock is a Hold above $60, but would add to our position in the middle $50s. Petmal Introduction It's no secret. Shale companies are on a plateau, trading sideways to down from recent highs right now. Even with the price of WTI touching highs not seen in almost a year, many of the shale names are acting toppy. Our subject this week is Occidental Petroleum Corporation (NYS

Occidental Petroleum: Take Me Down To 45Q Funkytown

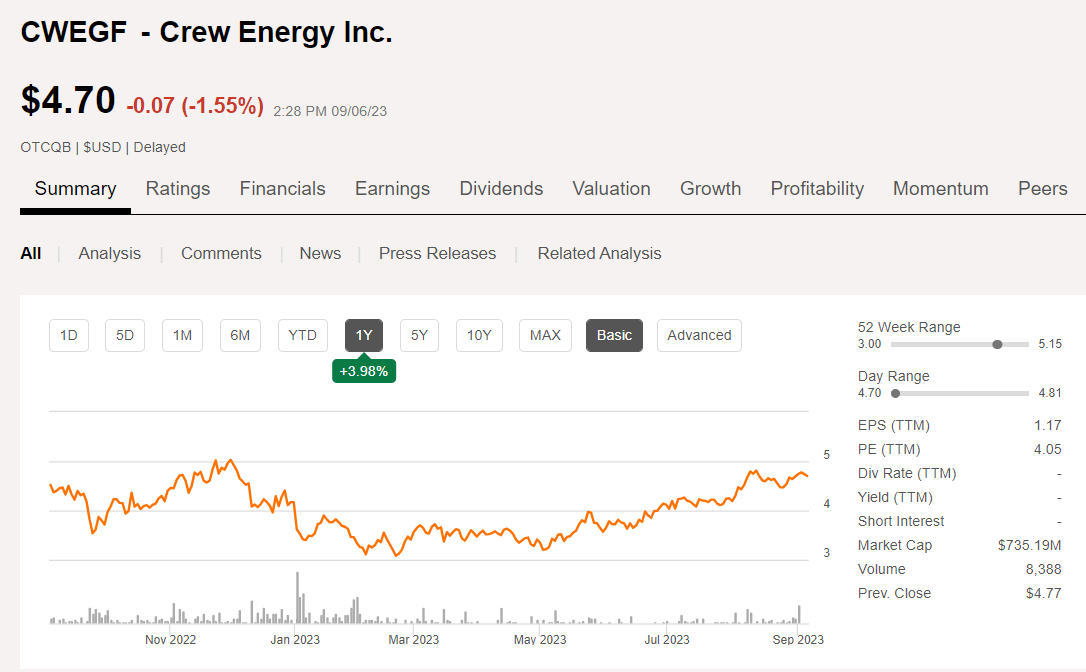

Crew Energy: Emerging Catalysts Could Carry This One Higher

wwing Introduction Crew Energy Inc. (OTCQB:CWEGF) is a Canadian gas-oriented producer that we last wrote up with a strong buy in the low $3's in February, noting however the macro environment for gas might make growth difficult over the short haul. That's still true, but there are some catalysts with a 3-6 month timeline that could change the story. Crew Energy price chart (Seeking Alpha) That wasn't a bad call, as the company has rallied to the upper-$4's, before making a slight pullback. Analysts are

{kind=link}

NextDecade: Maybe In The Next Decade

Hmmm...need a permit, hunh? I know a guy...but, it's gonna cost ya. Ugur Karakoc/E+ via Getty Images Introduction There is a good bit of churn in the marginal LNG space. When I say marginal, I mean plants that are not likely to be up and running until the latter part of this decade, or early in the next decade. (You got that pun, didn't you? Old mud engineers can't resist a pun.) NextDecade Corporation's (NASDAQ:NEXT) Rio Grande proposed facility in Brownsville, fits neatly into that category, as does Tellurian's (TELL), Driftwood plant south of Lake Charles, and Energy Transfer's (ET) Lake Charles LNG. They are all swimming upstream engaged

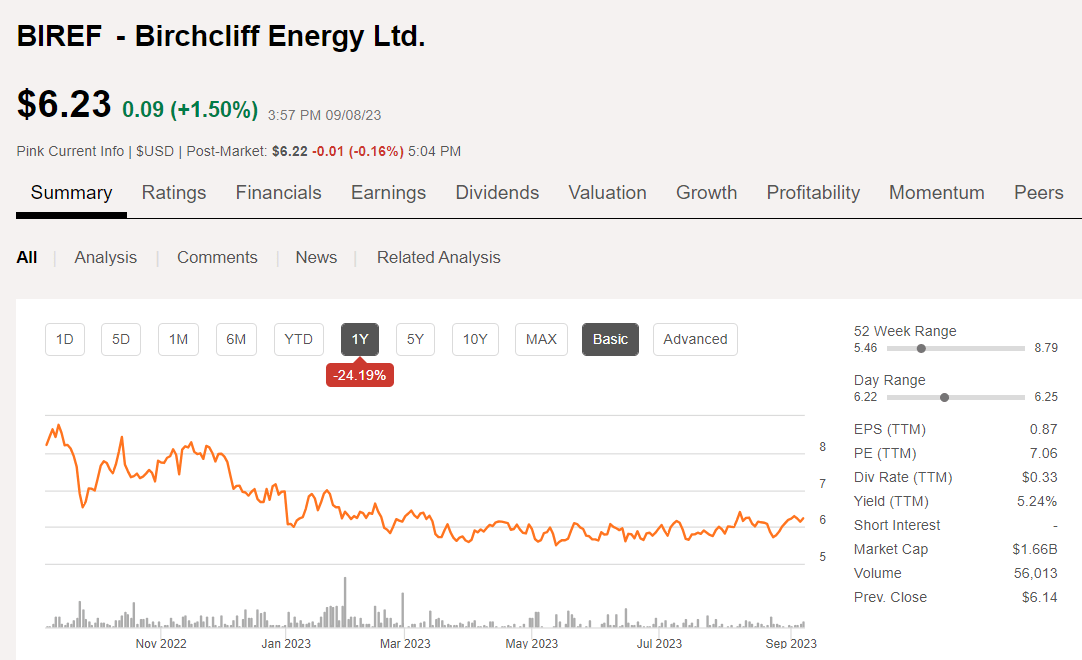

Birchcliff Energy: Higher 2024 Gas Prices Put Them In A Buy Zone

I want higher gas prices...and I want them NOW. zdravinjo Introduction Birchcliff Energy Ltd. (OTCPK:BIREF) is a Canadian energy company with a production base that runs lopsidedly to natural gas. The last time we covered them in May of 2022, we thought the company was in a buy zone near $8.00 per share. BIREF price chart (Seeking Alpha) That call looked ok for about a month as natty rallied in the $10 MCF range, and the stock rallied into the high $9's. It quickly began to age out as gas futures began to suggest the bottom was about to drop out

{kind=link}

Matador Resources: Still In A Buy Zone

BrianAJackson Introduction Matador Resources Company (NYSE:MTDR) was put on our buy list at ~$45 this May, and thus far it hasn't disappointed. For last couple of weeks it's been hanging about the $60 range, giving us a tidy ~30% bump higher in the last three months. Curiously, it took a step back on Friday for no reason I can discern but growing concerns about the Chinese economy, which appears to be ending a twenty year expansion that saw double-digit growth every year. On Friday, a big property developer in China, Evergrande, sought bankruptcy protection in U.S. and Hong Kong courts and had pundits wondering

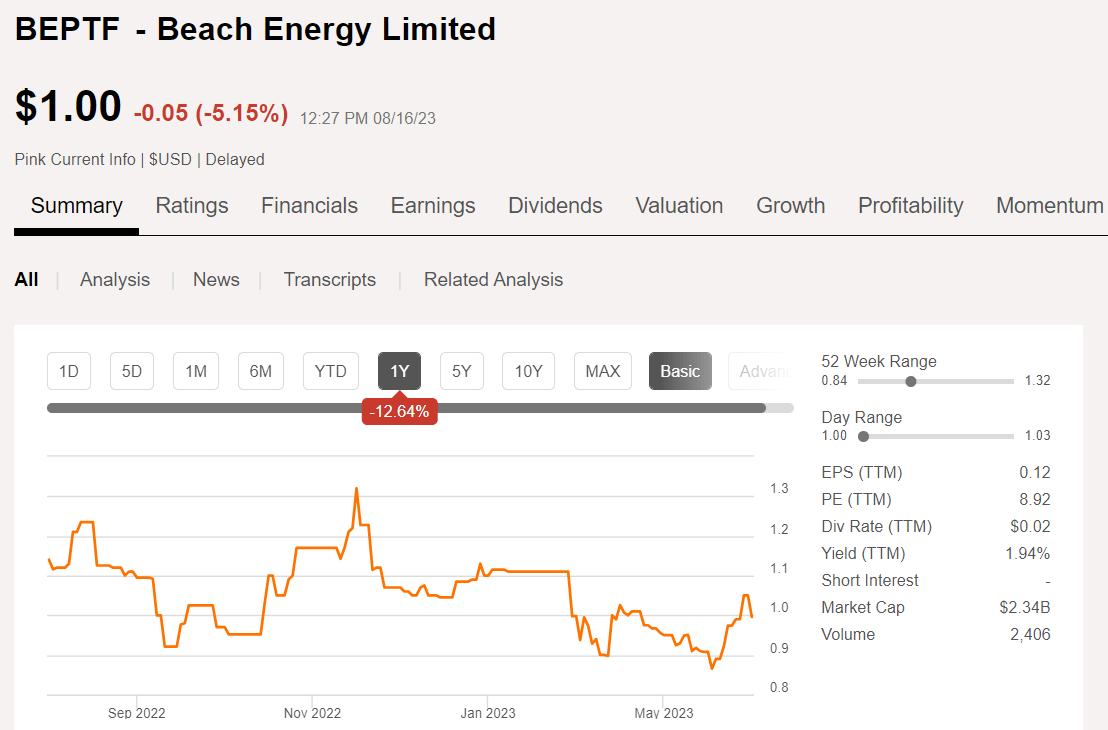

Beach Energy: Good Things Are Happening Down Under

moisseyev/iStock via Getty Images Introduction A quick look into my published article database showed that it had been a good while since I spilled any ink in the direction of Beach Energy Limited (OTCPK:BEPTF). Two years, as a matter of fact, so it was high time for a revisit. Readers might want to access this older article for more context, as I am going to focus on some key projects that are nearing fruition in this article. Beach Energy Price Chart (Seeking Alpha) Fortunately, we haven't missed much in the last couple of years,

{kind=link}

Core Laboratories: 'Spooked The Herd' In June, Things Might Be Looking Up

ftwitty/E+ via Getty Images Introduction Core Laboratories Inc. (NYSE:CLB) turned in a pretty decent quarter that was boosted by some one-off balance sheet adjustments. An $11,600 mm gain from rehoming to the U.S. from the Netherlands was logged, along with the proceeds from an insurance policy of $2.9 mm, made up most of the company's operating profit. Normal trading in this stock is 3-400K shares per day. On June 23rd an exit occurred of massive proportions, some 8 mm shares. As this was ahead of the earnings release a month later, one has to wonder what "spooked the herd" so early on. A "

Go to Tiger App to see more news