Holy Moly... Enbridge is in the $30's???? Gotta tell Dad to load the wagon!

Olga Potylitsyna/iStock via Getty Images

Introduction

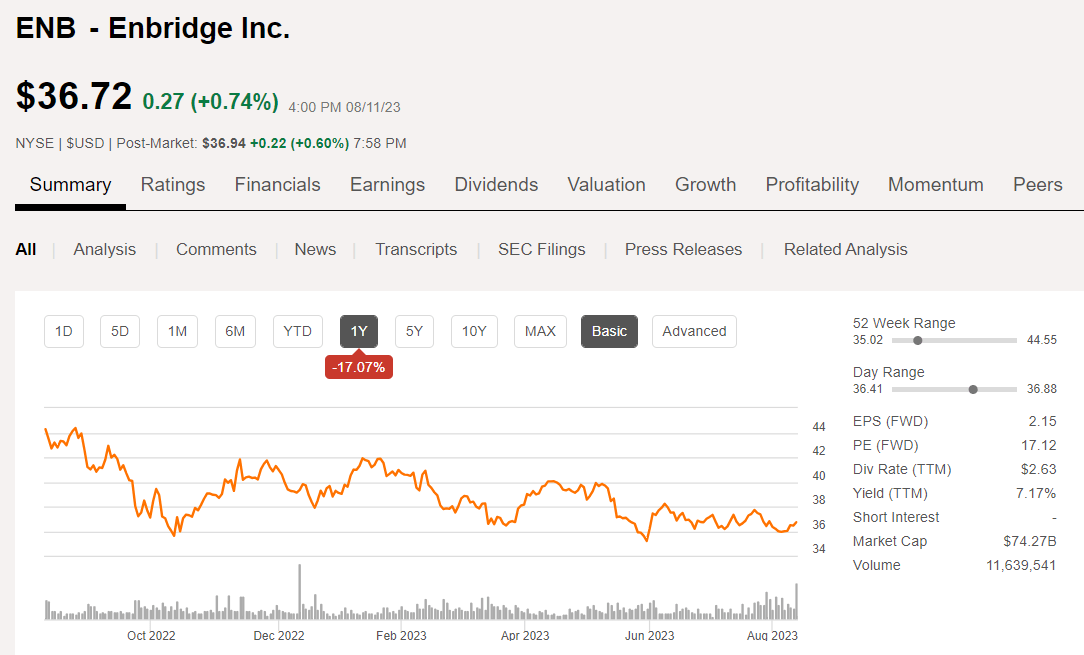

Enbridge (NYSE:ENB) hasn't been this cheap since 2021. Since early May it's been making lower highs and lower lows, bumping off support at $36.72 and then reversing to resistance at $37.42. On July 25th, it collapsed toward support set on 10-13-2022 at $35.00, and was saved only by a 10-12 mm share buy on the 11th (last Friday), from tapping the $35 line. Missing by a bit-$0.01, on their bottom line, and by a mile-$1.0 bn, on their top line for Q-2, probably has likely contributed to the recent share weakness.

ENB Price Chart (Seeking Alpha)

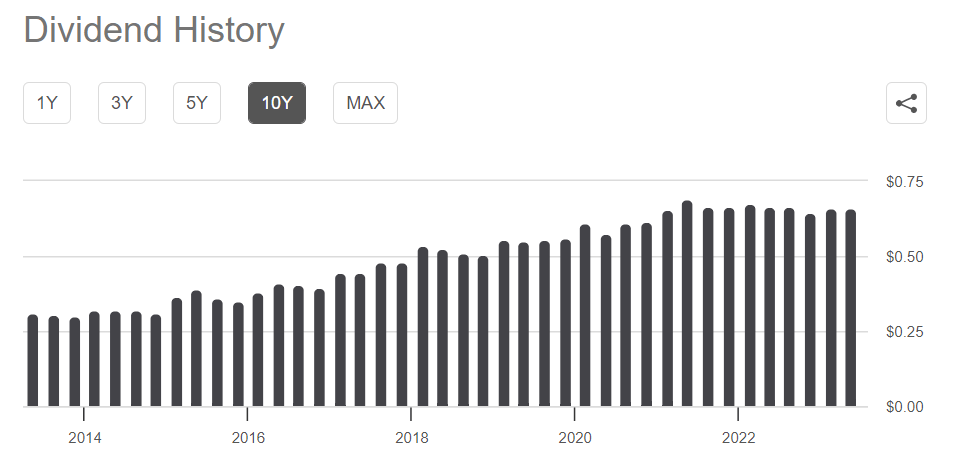

I would submit this is an excellent time to snag some of this reliable dividend payer, with a 10-year history of steadily paying and regularly increasing the dividend. I will further submit that the yield at current pricing is the primary reason to invest in ENB. Price improvement happens occasionally in pipelines, but mostly it is short-lived and the stock quickly reverts below the 200 Day, SMA. Where it is now. Who cares as long as that divvy check shows up regularly?

ENB Div History (Seeking Alpha)

I also like ENB for the yield and the fact it throws off a 1099 rather than a K-1. Long time readers know of my aversion to them, as I invest primarily through an IRA. ENB has been a reliable dividend payer for a number of years, and at current levels, I rate it a strong buy for superior and rising income, with possible catalysts for appreciation down the road.

The thesis for ENB as a dividend payer

As I get older, I think more and more about out-living my nest egg, upon which I will start drawing in the next year or so. I was able to save a substantial sum in my working years thanks to an above average income (Fluidsdocs get paid pretty well. Just try drilling a well of any depth without one. There's a common expression in the oilfield if there's a problem on the well. "It's the Mud." Most of the time, that is a fairly accurate statement.), most of that time, and some fortuitous investments that peaked at just the right time when I retired from SLB. My consulting, teaching, and then, a writing second career took off almost immediately and I was able to live off the income that work generated and put off drawing down the IRA.

Soon I will be faced with RMD's-Required Minimum Distributions, and will have to begin drawing that asset down. About half will go into regular expenses as my consulting career is beginning to tail off-(at 70, I just don't have the "fire-in-the-belly," I had at 69), and that income is dropping. The rest is destined for cash generating, regular dividend payers, like Enbridge, in my taxable account. I know I have a lot of company in the search for high yielding but relatively secure income, which is probably the reason you are reading this article. I am convinced that with ENB's superior assets, strong management, and successful, strategic business model they are a good choice for helping me maintain my standard of living, especially at today's pricing. ENB can help you too!

We all know ENB, and I will refer you to past articles for a detailed workup on the company. In my last article I called a hold on ENB in the upper $30's, thinking the stock price might present a better opportunity down the road. Thanks to improving macro-conditions, that hasn't happened, and with it recently declining from the mid-$40's, I am ready to make my move.

In the rest of this article we will discuss relevant events that could impact the shares, a potential catalyst that might deliver some growth, and the safety of the dividend going forward.

Recent events

We can't ignore that big buy last week. Something's up with ENB and perhaps pipelines in general as well. ENB has been in the news a lot over the past couple of years related to the Line-5 issue. News broke last week, that was probably the catalyst for the massive buy logged on the 11th.

ENB has agreed to relocate the line away from the Indian tribes property, thus (hopefully) putting end to uncertainty and future litigation on the matter. That is probably a fool's errand as where ever they go, there will be litigation, but at least they've cleared the path for the present. And, the market seems to like it.

It could also be something else, but settling that Line-5 deal, at least temporarily gets my vote as the reason funds (I presume with that kind of volume), loaded up on Friday. If you think otherwise, please tell me in comments.

Possible catalysts for the shares

There's the Enbridge system which moves heavy crude down from Alberta, Canada, picks up in Pontiac, makes a stop in Cushing, and barrels down to Freeport, Tex. A veritable super highway for this heavy stuff used to raise the gravity of Texas light oil. All of this sets up the SPOT-Seaport Offshore Oil Terminal, now being developed by ENB, and Enterprise Products Partners L.P., (EPD). This map from RBN shows the ENB Crude Oil Supersystems:

RBN Pipeline map (RBN)

Finally, no discussion of comparative advantage would be complete without reminding everyone of the company's Permian Light oil system which RBN notes in the article as having-

The company’s Permian light oil supersystem has few moving parts — three pipelines (two long-haul and one short), a small inland terminal at Taft and a gargantuan marine terminal in Ingleside — but it’s every bit as impressive and is poised to undergo expansions of its own.

The terminal has 15.6 MMbbl of existing storage capacity and is building another ~2 MMbbl of tankage (four 490-Mbbl tanks) that will be operational by late 2023 or early 2024. The kickers, of course, are the 52-foot draft alongside EIEC’s docks, the resulting ability to load up to 1.6 MMbbl onto a VLCC, and the potential to load two VLCCs and one Suezmax tanker at the same time. (The terminal can load at a pace of up to 160 Mb/h.) EIEC will be able to fully load VLCCs if and when the ship channel is deepened further.

Then there is the Permian pipeline export capacity. Over the past couple of years, the company has been increasing its ownership interest in the 670-Mb/d Cactus II pipeline (dark-blue line in Figure 1) to 30% and the 950-Mb/d Gray Oak Pipeline (green line) to 68.5%, and it announced earlier this month that it is pursuing a possible 200-Mb/d expansion of Gray Oak and that it’s likely the project will be sanctioned later this year. An expanded Gray Oak would allow Enbridge to further increase export volumes out of EIEC.

All in all, it's not hard to connect the dots here and see real competitive advantage for ENB in two areas. First with Permian crude export out of Ingleside, an area I remember for going offshore to Texas rigs in the Matagorda area, to points east. Second, demand for gasoline and diesel are on the rise, as are prices. This bodes well for the company's Heavy Oil System over the next several years, in terms of tolls, and long term contracts.

Risks

I think ENB is derisked at current prices. These are three-year lows; absent an industry collapse, shares are not getting much cheaper.

There is the debt, however. $54 bn is still $54 bn and interest rates are rising. Currently the company is paying about $2.3 bn in interest annually, and observationally, never seems to pay down the debt significantly. ENB has about $12.7 bn in credit facilities due between July, 2024 and July, 2027, with $1.9 due next year. The company has adequate cash flow to retire this debt, if it chooses. I don't see an imminent risk of default in ENB. For reference ENB carries an investment grade rating on its debt.

Q-2 Financials and Guidance

Revenue was lower sequentially but up YoY as was EBITDA. More importantly, EBITDA margin improved by 2% suggesting improved contract pricing. DACF, which is primarily what we care about with ENB as income investors, rose sequentially and YoY.

ENB Q-2, 2023 Results CAD (ENB)

Your takeaway

Since I am pitching ENB as a dividend play, the payout ratio of Net Income to dividends is worth touching on. Currently 97.36%, the company is flirting with a classic danger area for dividend safety in the current quarter. For reference ENB's ratio is historically high ranging from the current 97.36% to over 300% a year ago. As a dividend investor, I take some comfort in the fact that even at 300%, the dividend was paid. I respect companies that honor their commitments, and have noted that in articles on Exxon Mobil, (XOM), and Chevron, (CVX).

In terms of cash flow there aren't any concerns on an NTM basis. With EBITDA in the $15 bn range annually, capex of ~$3.6 bn, Divs of ~$5.6 bn are well covered, leaving plenty of spare cash for debt reduction or building a cash horde, and support the notion the company can maintain and incrementally raise the distribution for the foreseeable future.

What moves me off the dime at essentially the same pricing range where I called a hold six months ago, is the improving energy fundamentals on which the stock depends, and the improving margins that underpin distribution raises.

I think ENB rates a place in my income portfolio at its current price on improving industry fundamentals. Crude and gas prices have risen 25% and 33% respectively in the last couple of months, and these seem to have a tailwind behind them. The multiple is a little high, but a well covered yield above 7% is something we don't see everyday, and should be seized upon when it presents itself.

Comments