Vanit Janthra

Plug Power Inc. (NASDAQ:PLUG) reported Q2 2023 results.

The share price was weak after the earnings as a result of the weaker gross margin than expected.

However, I expect this to be one-off, as there are multiple levers to pull for the rest of 2023 and in 2024 to drive margin expansion in the near term.

Management is showing improving execution in the quarter, as the beat in revenue improves confidence in meeting its sales guidance.

Let's dive right into Plug Power.

Strength in the top-line and weakness in the bottom-line

In Q2 '23, Plug Power revenue came in at $260 million, 5% ahead of market consensus as a result of strength in the core material handling and cryogenics and liquefaction.

Sales for the cryogenics and liquefaction business grew significantly, growing 283% from the prior year to $70 million in Q2 '23.

Management sees considerable revenue and margin ramp in the cryogenics and liquefaction business in the second half of 2023 as a result of the outlook of its backlog, ramp of capacity.

In the medium term, the company is pursuing about $1.5 billion in bookings opportunities for the cryogenics and liquefaction business.

The material handing business is growing strongly as well, with another new pedestal customer signed in North America. There are now a total of 11 pedestal customers around the world.

In addition, Plug Power added 17 material handing sites in 2Q23, which was a 70% increase from the prior year and remains on track for the more than 80 new sites expected in 2023. If achieved, this more than 80 new sites in 2023 will represent almost 100% increase in site growth from the prior year.

Gross margins were the main weakness for the quarter, coming in at -30% in 2Q23, compared to -33% in 1Q22 and -21% from the prior year in 2Q22.

The weakness in gross margins were due to multiple scale up activities in the 2Q23, which resulted in a headwind of $45 million for the quarter. These include the expansion of manufacturing and introduction of several new offerings that resulted in one-off scaling headwinds.

However, in my view, gross margins actually are not as bad as feared as the adjusted gross margin would be -12.7% if we remove these one-off scaling activities.

As a result, after removing the one-time charges, the gross margin actually improved 8 percentage points in the quarter and management expects further margin expansion to come for the rest of the year, which I highlight below.

EPS for 2Q23 came in at -$0.40, which is in-line with the weaker gross margins, compared to market consensus of -$0.26.

The largest drag on earnings remains to be fuel delivered, with gross margin loss of -$46 million in 2Q23, compared to -$27 million from the prior year and -$44 million from the prior quarter.

In my opinion, this is where the company's very own green hydrogen production starting up will help to bring about very significant margin improvements when the Texas plant comes online.

This is because when green hydrogen is produced internally, it only costs one-third of third-party vendor costs.

Profitable fuels delivered business in the near-term

Once the Texas green hydrogen production is online and ramped up, which I expect sometime in the second half of 2024, the fuels delivered business will turn profitable.

This expectation was also highlighted by Plug Power's Chief Strategy Officer Sanjay Shrestha in the 2Q23 earnings call:

I think once we start to produce internally that actually reduces our cost of green hydrogen by one third versus what we're having to pay right now in the market.

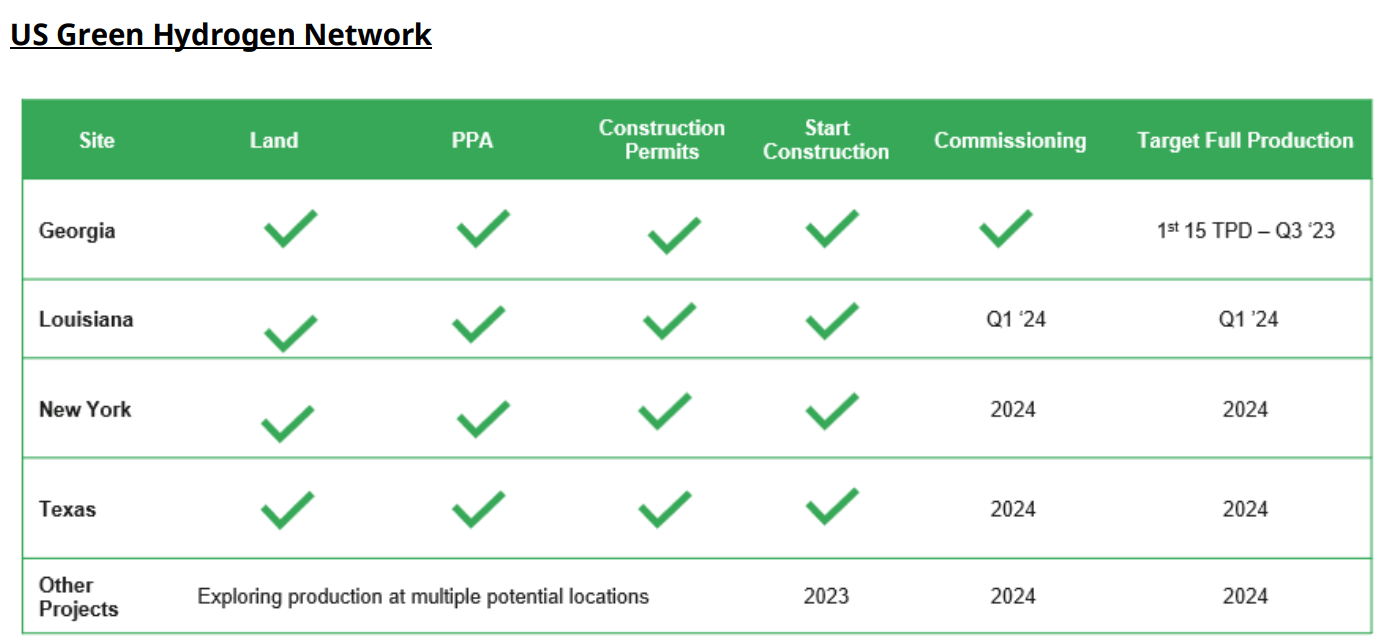

So, it's a step change, if you would, and the way the cadence of that is really Georgia, then Louisiana, then Texas, then New York, and our existing plant in Tennessee.

So, once we have Texas up and running, that's when you actually start to see our fuel business turn profitable, that is still buying from the third party under some of the existing contract right now.

I highlight the commissioning schedule and targeted full production for each U.S. green hydrogen site, and 2024 is poised to be a huge year for Plug Power in terms of the commissioning of its green hydrogen plants in the U.S.

US green hydrogen network (Plug Power)

With significant green hydrogen production capacity coming online in 2024, the company is able to generate considerable cost savings from the internally produced green hydrogen, which is expected to cost just one-third of third-party vendor costs.

Management of average selling price

Another positive we have seen in the quarter was that Plug Power was able to increase the prices on some of its offerings.

This is because of the validation that Plug Power has received for its productions and solutions as customer see how it benefits their businesses and goals.

The management of the average selling price of Plug Power's offerings will be implemented for the rest of 2023.

This enables the company to bring about an even better margin profile on top of the internally generated green hydrogen production mentioned earlier, providing management with another lever for gross margin expansion.

Lastly, I think the ability to adjust prices of its products and solutions shows that Plug Power's competitive positioning is improving as customers value the benefits that its products and solutions bring.

Financing

I am of the view that Plug Power has sufficient cash and funding for its growth plans, which I will elaborate further below.

Plug Power believes it will be able to tap into a Department of Energy loan of $1 billion to $1.5 billion in 2023.

This is because it is currently undergoing a second and likely final round of due diligence.

In the meantime, there are also other debt facilities that will help bridge the company's cash needs in the near-term.

On top of that, Plug Power is working with potential equity partners for future hydrogen plants. If successful, this will enable its business to be more capital efficient.

Solid execution in new products and industries

The refining industry is one of the largest industries that consumes grey hydrogen and as a result, this is one of the more logical markets for Plug power as a possible end market for its offerings.

Plug Power could sell green hydrogen to players in the refining industry, or it could also sell the equipment to the refiners looking to build and operate their own green hydrogen facilities.

Plug Power demonstrated solid execution in the quarter as a European integrated energy operator awarded Plug Power a 100 MW electrolyzer order, which is meant to replace gray hydrogen in the refining industry.

Earlier in the year, Plug Power introduced HL 1500, which is a portable hydrogen refueler solution. In another sign that management is executing really well, the HL 1500 product has already been completely sold out. Given that this is a high margin product, I expect this to have a positive impact to not just the top but also the bottom line starting 4Q23.

Management expects substantial growth coming out of this business, both in 2024 and 2025 and this product currently already has a gross margin that is within Plug Power's corporate target.

Electrolyzer to ramp in 2H23

Plug Power's electrolyzer pipeline is now 7.5 gigawatts or $5 billion. This includes projects that could realistically proceed to final investment decision in the next 12 to 18 months.

I continue to expect a strong second half 2023 ramp for electrolyzers.

This will be weighted heavily towards Europe and also the fourth quarter of 2023.

As a result, the ramp in the second half of 2023 is unlikely to be impacted by the PTC guidance in the U.S.

With regards to the US PTC, the team at Plug Power expects a reasonable outcome, with guidance likely to come sometime in September.

Negative sentiment priced into stock

With the negative sentiment around Plug Power today, I suspect that the market is not rewarding Plug Power for the increasing likelihood that the company remains on track to hit its 2023 to 2026 sales guidance.

While margins were challenged in the quarter, I think that there is an increasingly visible path to deliver margin improvements through the rest of 2023 and in 2024.

In addition, execution is improving as evident from the quarter as revenue trajectory is improving in 2Q23 and even more so in the second half of 2023 as a result of the expected ramp in electrolyzer sales and GenDrive shipments in the period.

Valuation

While there are reasons to raise my forecasts for 2023 given that management continued to improve on execution and thus, confidence in the stock, I intend to be conservative with my estimates for this one for now to ensure sufficient margin of safety.

I am reiterating my 1-year price target of $17.60.

This is based on a 5x P/S multiple for Plug Power, which is justified given its leadership position in the hydrogen economy.

Conclusion

While Plug Power has been a difficult one to hold as a result of it being lumped together with the other unprofitable growth stocks in the drawdown of 2022, I think that we are starting to see that management execution is improving in recent times, particularly in the quarter.

I am incrementally more positive on Plug Power's ability to drive revenue through its growing and large pipeline, while driving margin expansion along with it as its green hydrogen production ramps up and manufacturing is executed well.

The weakness in gross margins for the quarter as a result of the multiple scale up activities is a slight road bump, but I expect that management will continue to drive margin expansion for the rest of the year with green hydrogen production plants coming online and management of the average selling prices of its offerings.

I continue to like the fundamental story for Plug Power going forward and this one is for long-term investors looking to have exposure to the green hydrogen sector.

Comments