ftwitty/E+ via Getty Images

Introduction

Core Laboratories Inc. (NYSE:CLB) turned in a pretty decent quarter that was boosted by some one-off balance sheet adjustments. An $11,600 mm gain from rehoming to the U.S. from the Netherlands was logged, along with the proceeds from an insurance policy of $2.9 mm, made up most of the company's operating profit.

Normal trading in this stock is 3-400K shares per day. On June 23rd an exit occurred of massive proportions, some 8 mm shares. As this was ahead of the earnings release a month later, one has to wonder what "spooked the herd" so early on. A "seagull" at Citi downgraded them a week later, in an eerily prescient call, citing "Completion Weakness." Ya think? Ok, I don't want to get too snarky here, but sometimes the million dollar prima donnas making "consensus calls" get under my slicker suit.

Since then, the stock has traded in a rising channel pattern, breaking through support at the old resistance line at $23.84 on June 28th. Recently on Aug, 2nd it rallied to $27.50 before collapsing back to $25.26 on the same day. It is now trading higher above the resistance line, presumably on the strength of oil prices moving into the mid-$80's and the trend toward higher offshore day rates. The trend here looks bullish to me, let's see if we can justify the prices on fundamentals.

In this article, we will review Q2 2023 and see if we can revise our opinion of the company.

The Thesis for Core Labs

The company's signature Reservoir Description business has suffered in recent years due to a lack of exploratory drilling. I don't think there is any question we are in a new offshore development cycle. The question is, is it likely to fatten CLB's coffers?

The best way to begin a story is at the beginning. Before Core Labs gets a call for reservoir description services, what has to happen? The answer is seismic data needs to be collected or accessed. Then it needs to be processed internally by an oil company. If things look good an exploratory prospect is generated. A rig company gets a call, and in the success case cores and fluid samples are taken. And, then Core Labs gets a call.

Since 2013, the seismic industry has collapsed from about a dozen competitors with about 60 vessels sounding the marine depths to about 17 being marketed today. There are two major offshore seismic data collectors and only one is publicly traded. Petroleum Geo Services (OTCPK:PGEJF), is one (trading today at $0.74 per share) and Shearwater Geoservices, (a private Norwegian company) is the other.

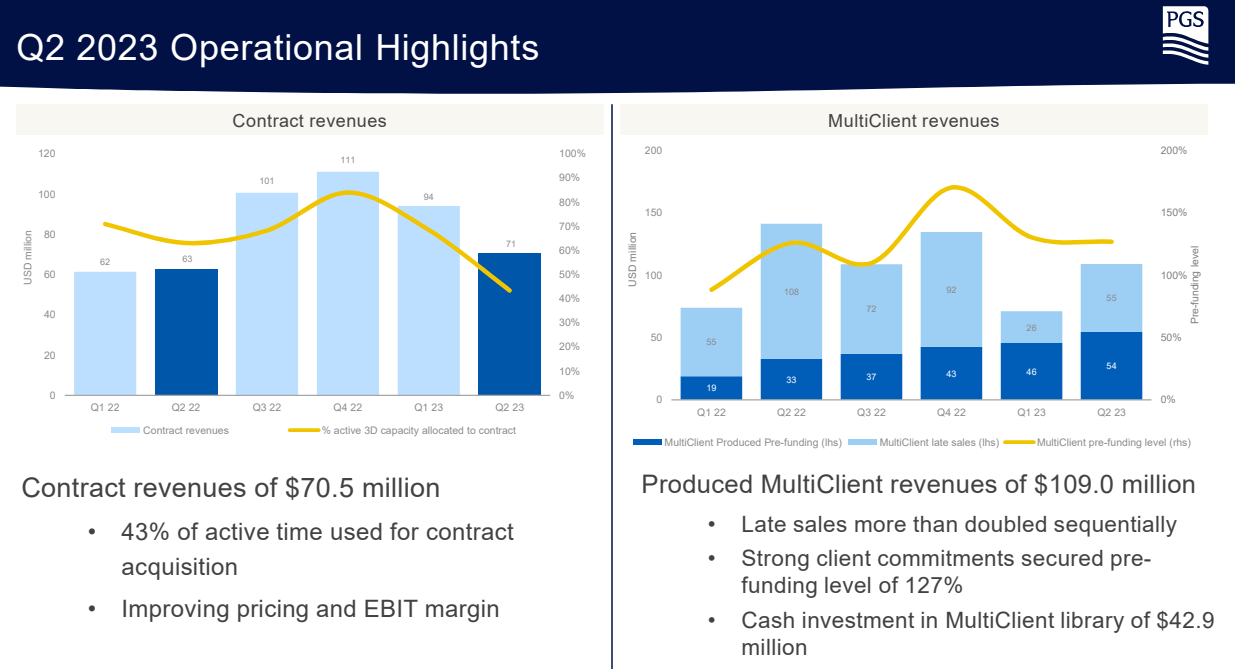

PGS Revenues (PGS)

It is somewhat instructive to me that Seeking Alpha no longer publishes conference calls or financial data on PGS. Nothing in the chart above suggests an impending renaissance for offshore geophysical surveys.

Now this early upstream exploration activity is not the whole story for CLB, reservoir description work is on the increase as has been noted in various calls. The source could be coring for stepouts on existing data sets or the MultiClient work subscribed to by a number of companies.

Schlumberger (SLB) CEO Olivier le Peuch, and CFO Stephane Biguet commented in their Q2 call on the re-emergence of exploration activity and Reservoir Performance (emphasis added):

Le Peuch-The return of exploration and appraisal across Africa and the Eastern Mediterranean will bring new opportunities for Reservoir Performance in exploration and appraisal. Biguet-Reservoir Performance revenue of $1.6 billion increased 9% sequentially, while margins improved 248 basis points to 18.6%. These increases were primarily due to strong growth internationally, led by the Middle East and Asia. Year-on-year, revenue grew 23% and margins increased 396 basis points driven by strong growth internationally, both on land and offshore.

Now let's compare that with commentary from the PGS report.

As the global energy transition evolves, PGS expects global energy consumption to continue to increase over the longer term, with oil and gas remaining an important part of the energy mix. Offshore reserves will be vital for future energy supply and support demand for marine seismic services. The seismic market is recovering on the back of increased focus on energy security, several years of low investment in new oil and gas supplies, and higher oil and gas prices. Offshore investments in oil and gas exploration and production are expected to increase in 2023.

- The seismic acquisition market is likely to benefit from the higher exploration and production spending, and a limited supply of seismic vessels.

- PGS expects full year 2023 gross cash costs to be approximately $550 million. The increase from 2022 is primarily due to the higher activity level and more capacity in operation.

- 2023 MultiClient cash investments are expected to be approximately $180 million. Approximately 50% of 2023 active 3D vessel time is expected to be allocated to contract work.

- Capital expenditures for 2023 is expected to be approximately $100 million.

- The order book amounted to $341 million on June 30, 2023. On March 31, 2023, and June 30, 2022, the Order book was $377 million and $311 million, respectively.

Now let's hear from Larry Bruno, CEO of Core Labs:

Reservoir Description operations are closely correlated with trends in international and offshore activity levels, with approximately 80% of revenue sourced from projects originating outside the U.S. Revenue in the second quarter of 2023 was $83,400,000, up 4% sequentially and up 10% year-over-year.

To summarize the above quotes, SLB notes an increase in reservoir performance revenue of 9% sequentially, which is pretty dramatic on a run rate basis. Both PGS and CLB report increasing revenues on the exploration side of things, and notably for PGS the portion coming from Contract revenue is on the increase. For CLB, 10% YoY largely correlates to what SLB is saying, and I would offer, anytime you are keeping pace with SLB, you are on the right track.

I think there is a solid case for CLB's revenues to be on the increase in this critical area.

On to CLB's Production Enhancement segment. Production Enhancement operations, which are focused on complex completions in unconventional oil and gas reservoirs in the U.S., as well as conventional projects across the globe, posted second quarter 2023 revenue of $44,500,000, down approximately 8% sequentially, and flat year-over-year. Operating income on a GAAP basis was $5,500,000, while operating income, ex-items, was $4,400,000, yielding operating margins of 10%, down 270 basis points sequentially; however, year-over-year, operating margins expanded 120 basis points. The sequential decline was primarily associated with lower international bulk product sales and a decrease in U.S. land completion activity.

This segment's underperformance was the focus of a Citi analyst - Scott Gruber - downgrade in Q2, as previously noted. Quoting from the article here.

Citi analyst Scott Gruber lowered his Core Labs' Q2 EBITDA forecast by ~5% to $18.9M, ~6% below consensus, anticipating weakness in North America completions will hurt the Production Enhancement business.

We have discussed CLB's business units in some detail in past articles, so be sure and look those up if CLB interests you.

Q2 and Guidance

CLB's core financials aren't hard to parse. Revenue is flat QoQ, and up about 5.8% from the same period a year ago. Reservoir Performance carried the ball with a 4% sequential and 10% YoY revenue increased to $83 mm. Production Enhancement was down sequentially and YoY at $44.5 mm. Operating income rose to $18 mm thanks to the two one-off items previously mentioned. Long term debt has been rising, ending the quarter at $182 mm, up sequentially and 5.9% YoY. Cash on the books sits at $26 mm. Free cash is running at $12 mm run rate, exceeding capex of $4 mm and divs of $2.6 mm comfortably and leaving $5.4 mm for debt paydown. CLB faces no short term liquidity issues.

Guidance

Core continues to anticipate a multi-year international recovery supported by increased spending on exploration in many regions across the globe and expanded development of existing fields to fortify crude-oil and natural gas reserves. This underlies Core's outlook for continued improvement in international onshore and offshore activity, with ongoing projects across the globe, most notably across the Middle East, South Atlantic Margin and West Africa.

Risks

The risk for CLB is the entry point. I was leery of them at $20ish, I am even more leery of them at $26. Entry points are everything in making money in oil and gas and OFS stocks. Get in too high, and you may have a decade to think about it.

Your Takeaway

The six analysts that cover Core Laboratories Inc. have it rated a hold. Price targets range from $19 to $31, with a median of $21. Either of those two lower numbers would probably make an acceptable entry point in today's market.

The company is currently trading at 21X EV/EBITDA and that's outside the boundaries for us.

Summary: Long term, Core Laboratories Inc. is a solid performer with a rising market and we'd like to have a chunk of it. We will be patient and hope that a better entry point comes around, while understanding it may not this cycle. Core Labs remains a hold.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Comments