moisseyev/iStock via Getty Images

Introduction

A quick look into my published article database showed that it had been a good while since I spilled any ink in the direction of Beach Energy Limited (OTCPK:BEPTF). Two years, as a matter of fact, so it was high time for a revisit. Readers might want to access this older article for more context, as I am going to focus on some key projects that are nearing fruition in this article.

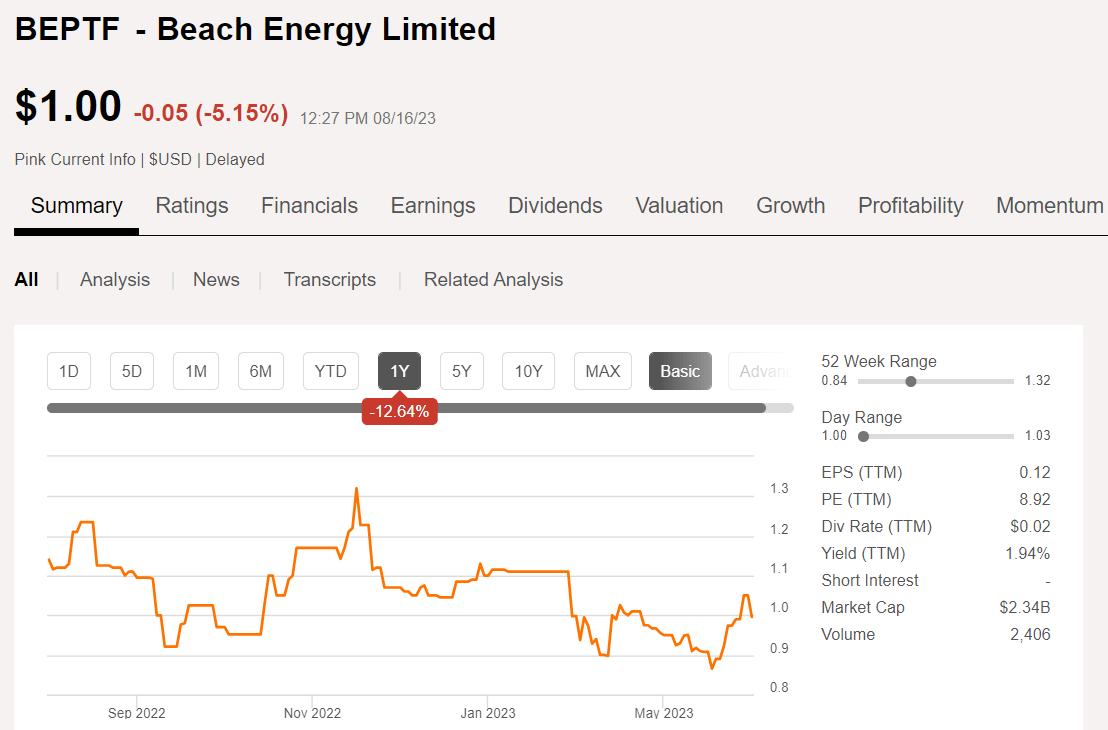

Beach Energy Price Chart (Seeking Alpha)

Fortunately, we haven't missed much in the last couple of years, as the stock has oscillated between about $1.50 and $0.79. So, if there is an opportunity in Beach, it could still be well within our budget.

Analysts are moderately bullish on the stock with an overweight rating and price targets from $1.30 to $2.00 USD, with a median of $1.73.

Let's review their just-released fiscal Q4 2023 report and make our own estimate as its investability.

The thesis for Beach Energy

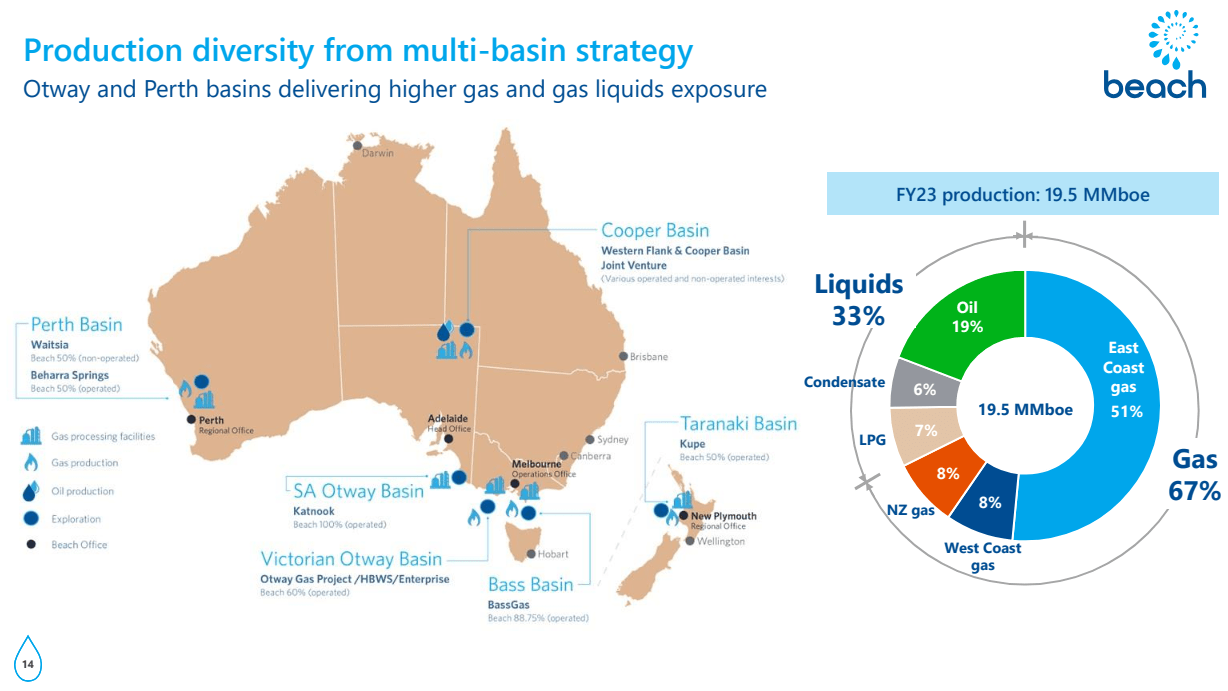

Beach is a basic energy supplier to the Australia/New Zealand region. their production is half gas, thirty percent heavy liquids, and twenty percent crude oil. When last we checked on Beach they were embarking on a couple of projects that had the potential to be transformative for the company. The first, in the Perth basin, is the Waitsia gas development that will connect formerly stranded gas to a gas processing plant being constructed with partner Mitsui. Project delays have extended the delivery dates as noted here. Then there were the Otway and Bass basin developments to deliver gas into the heavily industrialized and populated East Coast. Both of these developments are ready to begin sending gas into this structurally undersupplied market.

Beach Energy Footprint (Beach Energy)

Poor policy decisions and environmental lobby success in demonizing hydrocarbons have left the country in a pinch for power generation. This recent Wood Mackenzie note summarizes the situation into which Beach has been positioning itself the last couple of years.

Australia requires gas for power generation as well as other industrial uses including mineral processing, mining, chemical production and fertiliser. Gas is also critical to reducing coal demand in power and as a back-up for intermittent renewables. Simply adding more wind and solar won't change this.

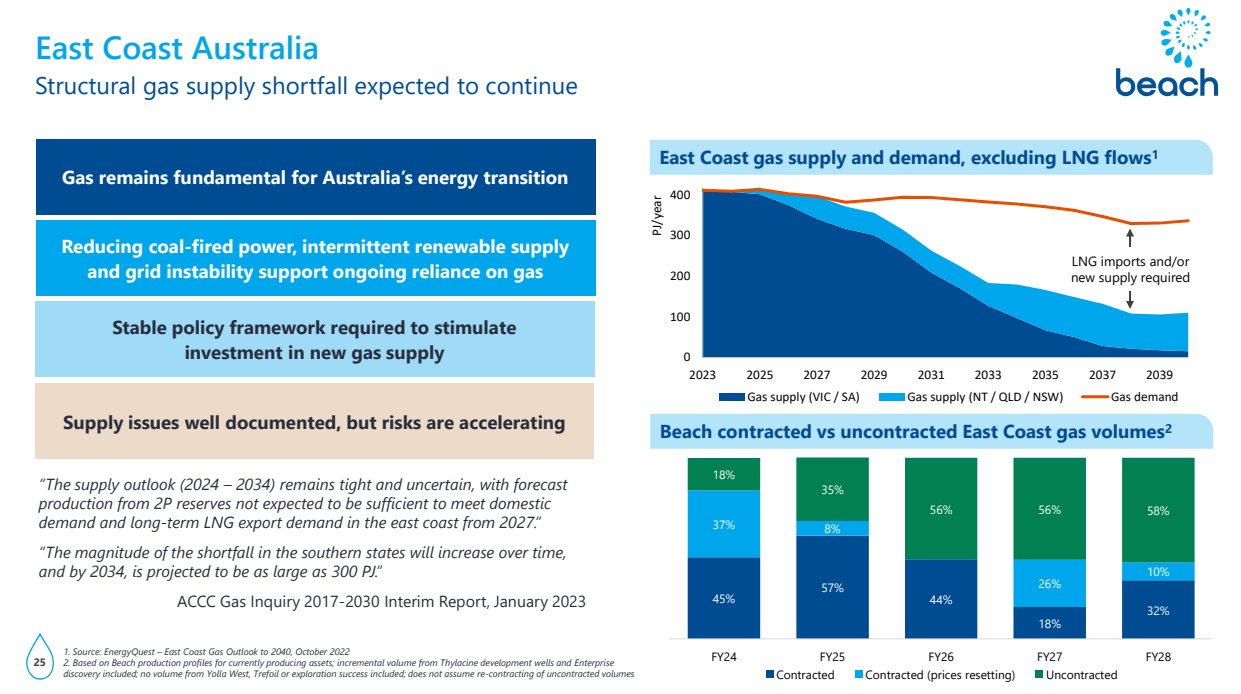

Hungry power markets for growing economies at home and abroad in the ASEAN region underpin the thesis for Beach at current pricing. Markets where there are wide gaps between demand and developed resources, as the slide below notes.

Gas supply picture for Aussie East Coast (Beach Energy)

Bruce Clement, CEO of Beach, commented on their positioning with respect to the developing energy market in the ASEAN region during the fiscal Q4 earnings call:

Selling gas in Australia and New Zealand is an important part of supporting the local economies and supporting the transition, the energy transition that's underway. We see, in all these markets, a tightening of supply, and Beach is well positioned as it moves forward to supply into these tighter markets. We have been -- whilst much of the industry has been cutting back on investment in exploration and development, Beach has been investing in these activities, and we're going to see the benefits of those as we bring additional production into those markets in financial year '25 and beyond.

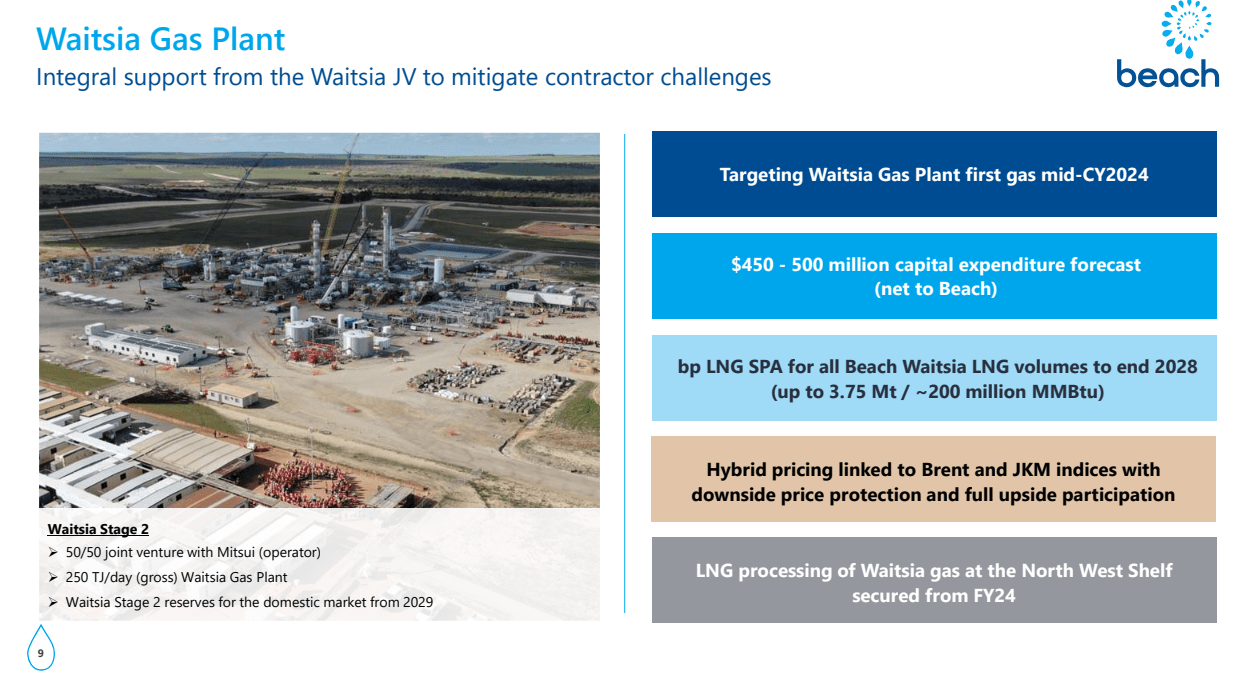

Waitsia

Waitsia has been troubled by woes related to the default of their original contractor. Originally scheduled to begin delivering gas this year, the schedule for first gas was pushed into next year-2024. BP p.l.c. (BP) has signed an SPA to begin taking LNG from the Waitsia that provides for delivery of 3.75 MTPA LNG through 2028. This will be at pricing that exposes the Aussie gas to JKM pricing, which is generally advantaged with respect to domestic-Aussie, prices.

Beach Energy Waitsia Gas plant (Beach Energy)

Otway

The Otway/Bass development is high gear and delivering gas into the East Coast market. Beach estimates their current share to be about 12%, and expects to begin capturing additional market share in FY-2024/25.

Beach Energy-Otway Basin (Beach Energy)

Contractual agreements are in process that may set limits on actual Otway offtake. CEO Bruce Clement commented in that regard:

The offtake arrangements in the Otway, given we now have additional well capacity there and our contract offtake will determine, to some degree, the amount of gas we produce and sell out of Otway.

What's important to us is that this is a long-term sales opportunity into an under-supplied market. Sales will come.

A possible additional catalyst for Beach

Probably no nation has restricted their hydrocarbon development more than New Zealand. One of the first things recently departed Prime Minister, Jacinda Ardern did upon assuming office was to ban new offshore drilling permits. Existing permits stayed in force, and Beach has one for the Kupe South 9 well a few miles offshore. This well is advantaged by existing facilities on and offshore.

A catalyst for Beach Energy (Beach Energy)

New Zealand is in a bit of a fix, as this Bloomberg article notes. They're running out of gas in about 10 years, with no easy fix on the horizon. The Minister for Energy discusses some of their go-forward strategy in this document. Unsurprisingly, this is filled with a lot of happy "hopium" boilerplate, that is long on high-minded environmental blather and very little substance.

My bet is that New Zealand undoes this "No new Permits" restriction to stay in the modern world. We shall see.

Q4 for Beach

Beach produced 19.5 million barrels of oil equivalent in the year just completed. Production declined by11% as capex was focused on delivering major growth projects, in the Otway, and Waitsia basins.

Production composition continues to shift more towards gas as the Thylacine North wells were brought online late in the year. This trend will continue in FY '24 and beyond with substantial new gas supply to come from the Enterprise, Waitsia Stage 2, and the Thylacine West wells.

Sales revenue was down 8% to $1.6 billion with a higher realized gas price partially offsetting lower production. A 9% increase in gas prices reflected the continuing tightening of domestic markets and additional volumes directed to the spot market in the second half.

Beach Energy Financials (Beach Energy)

Lower revenues flow through to lower earnings and cash flow, with a 12% decline in underlying EBITDA to $982 million and operating cash flow of $929 million. Higher DD&A from increased Otway Basin production and higher financing costs from higher discount rates on non-cash unwind of liabilities flow through to the underlying NPAT of $385 million.

Operating cash flow was 24% down to $929 million. Again, this was largely driven by lower revenue and higher cash cost impacts, along with higher income tax and restoration payments during FY '23. It was a year of elevated capital expenditure, with $484 million of capital expenditure directed towards the growth projects.

Sustaining and stay-in-business capital expenditure of $687 million also increased from FY '22 levels, largely due to an accelerated work program and additional activities undertaken in the Cooper Basin. Beach drew down on their debt facilities to support major growth projects during FY '23, while generating $221 million of pre-growth free cash flow during FY '23, supporting the declaration of a $0.02 per share final dividend, a 100% increase on the previous year.

Beach closed out their year with $166 million net debt. This represents net gearing of 4%, which is well within their target gearing of less than 15%. Available liquidity remained strong at year-end at $434 million, with prospects for strengthening cash flow.

Risks

The principal risk I see for Beach is governmental. At this point, you can't absolutely say that governments will not self-destruct their economies. There is too much evidence to the contrary. It remains to be seen how much damage we let those in charge do before restoring a semblance of sanity.

Their key project-Waitsia is a complex capital and labor-intensive undertaking that could exceed forecast expenses.

There is also liquidity, with risk from the security having a very low trading volume, due to lack of familiarity.

Your takeaway

Beach Energy Limited's guidance for the next fiscal year is a bit spongey, as delivery timings are up in the air for key projects. Production will be between 18-21 mm BOE tied to the hedges mentioned above. Capex will be between $850-1,000 mm, again depending on timings. This is a bit problematic as it will likely have them dipping into credit lines to cover these expenses. That puts other financials in a speculative framework, and it is probably not worth playing with the numbers to see what multiple they might grow into next year.

At the present, Beach is trading at a pretty attractive level at 2.4X EV/EBITDA, and $44K per BOE. Neither of those seem excessive for a company with the prospects that Beach seems to have over the next couple of years.

All things said and considered, I believe the Beach Energy Limited risks outweigh the opportunities, and better opportunities exist on this side of the world. Accordingly, we rate Beach Energy shares a hold. I don't see any near-term catalysts that will drive the stock higher, absent a sharp turn higher in commodities.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Comments