BrianAJackson

Introduction

Matador Resources Company (NYSE:MTDR) was put on our buy list at ~$45 this May, and thus far it hasn't disappointed. For last couple of weeks it's been hanging about the $60 range, giving us a tidy ~30% bump higher in the last three months.

Curiously, it took a step back on Friday for no reason I can discern but growing concerns about the Chinese economy, which appears to be ending a twenty year expansion that saw double-digit growth every year. On Friday, a big property developer in China, Evergrande, sought bankruptcy protection in U.S. and Hong Kong courts and had pundits wondering if the country was having its "Lehman" moment. Concerns that apparently have vanished today, underscoring the fickleness of the market.

MTDR Price Chart (Seeking Alpha)

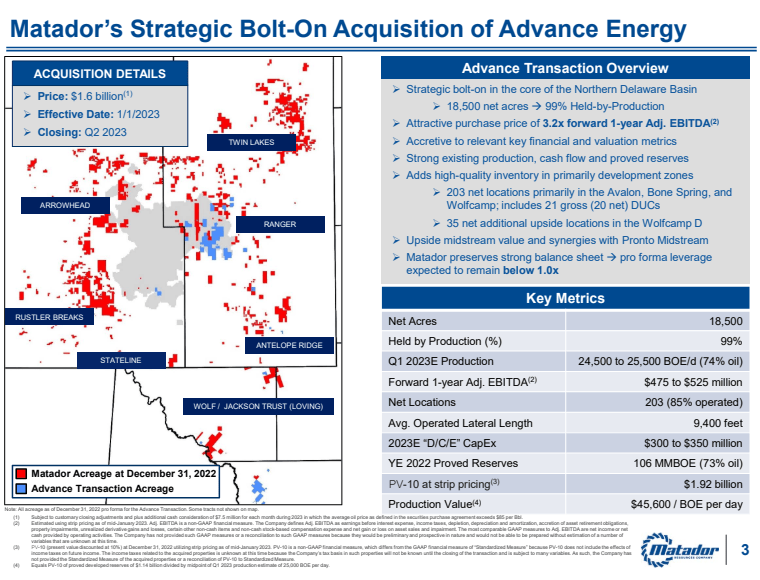

Matador is on a furious growth spurt, with daily output rising from ~100K BOEPD at the beginning of the year, to ~130K BOEPD now, with YE output scheduled to be ~140K BOEPD. That's 40% in one year! Part of this growth came as a result of their strategic, bolt-on acquisition of Advance Energy, a unit of Encap Partners. Advance facilitated MTDR's existing Delaware acreage in the form of longer lateral options, and more throughput for MRDR's Pronto midstream asset. The Advance properties are extremely advantageous for MTDR, as the deal slide shows below, with the high oil-cut Advance acreage adding oil weighted (74%) to the total. The financials look pretty good as well.

MTDR-Advance Energy Acquisition (MTDR)

The question before us at present: is all of this priced into the stock or is there still room to run? Analysts have a buy on the stock, with estimates ranging from $62-87 and $71.43 at the average.

Let's review their recently released second quarter results to see if we should chase this one at current levels.

The thesis for chasing Matador

We've done pretty well the last few months, but a rally of the kind MTDR has had makes you wonder if its getting a little toppy. It really doesn't look like that's the case. Matador comes into Q3 with a 21 well batch turn to sales that should bring them a large part of the way toward the YE-23 goal of 150K BOE per day. This puts them in a position to drop from 8 rigs to 7, and do some facility consolidation as they incorporate the Advance properties into their operating structure. The additional ability to drill extended reach in their core Delaware position will also drive drilling costs lower, as Chris Calvert Co-COO notes:

Looking forward for that $1,100 per completed lateral foot, we do expect to realize some pretty immediate cost savings, both on the completion side really immediately into the third quarter and then on the drilling side as well, going into the latter half of the year and then into 2024. And so, we are guiding that number down and that number comes from a combination of those capital efficiencies that we've spoken to and then also the more competitive service cost environment.

Declining costs and increasing production are formidable driver for higher revenues and margins. And, usually form a logical investment thesis for a company. What's missing? Execution, of course. In the slide below, MTDR shows well IP30's well in excess of EIA averages.

MTDR making great wells (MTDR)

Reserves are an E&P's core capital. Whether drilling in the Delaware or on "Wall Street," MTDR has shown the ability to grow reserves. Notably the Advance reserves came at the equivalent of ~$45K per barrel, and an NPV that exceeds the purchase price by 80%. A good deal any way you slice it.

MTDR Reserves (MTDR)

MTDR carries a solid balance sheet with no near-term maturities, and has already repaid $140 mm to the RBL balance.

MTDR liquidity (MTDR)

Q2 2023 and Guidance

MTDR beat on the bottom line, while missing on top line by a hair. It delivered average production of 130,683 BOE per day with an oil cut of 76,345 barrels of oil per day. This was 23% better than the first quarter 2023 production of 106,654 BOE per day. OCF provided by operating activities came in at $449.0 million with adjusted Free Cash Flow of $77.7 million. Adjusted net income of $170.1 million, or adjusted earnings of $1.42 per diluted common share, and adjusted EBITDA landed at $423.3 million for the quarter.

Capex was lower-than-expected drilling, completing and equipping capital expenditures of approximately $310 million, which was 14% better than the previous budgeted expectation of $358 million. A nice reduction due to efficiencies brought in from Advance. CEO Joe Foran notes the value coming from the Advance integration into MTDR:

These lower capital expenditures are primarily due to capital and operational efficiency savings that we were able to implement with regard to the Advance assets and our legacy operations and the timing of our planned projects near the end of the second quarter and into the third quarter of 2023 for both our exploration and production and our midstream businesses.

Guidance for the rest of the year

Due to the better-than-expected well performance across both Matador's legacy assets and the recently-acquired Advance assets, they are increasing the 2023 production guidance. The midpoint of their 2023 total oil production guidance is increased from 26.85 million barrels of oil to 27.15 million barrels of oil. Also they are increasing the midpoint of 2023 total natural gas production guidance from 110.7 billion cubic feet of natural gas to 117.0 billion cubic feet of natural gas. As a result, the midpoint of 2023 total oil and natural gas equivalent production guidance is increased from 45.30 million BOE to 46.65 million BOE.

The company expects that these capital and operational efficiencies and service cost decreases will result in well cost savings of $25.0 to $30.0 million for the remainder of 2023 as compared to prior expectations. These long term service relationships will carry this rate of capital and operational efficiencies and decreased service costs in 2024 and beyond. This will result in lower total capital expenditure guidance from $1.425 billion to $1.335 billion.

Risks

Obviously our thesis is based on oil prices in the neighborhood of $80 or above. If that doesn't turn out to be the case, the shares could revert lower.

Your takeaway

On a run rate basis Matador Resources Company is trading at ~4.6X EV/EBITDA presently. It's flowing barrel rate is $65K per BOE. Neither are excessive in today's market in my estimation. Let's have some fun with numbers to see if we can get to the analyst estimates for MTDR.

If they hit 150K BOEPD by year end, the FB calc would drop to $56K per barrel, and the EV/EBITDA would drop to 4X. An adjustment toward that analyst midpoint of $71 certainly seems likely in that event. Oil prices are doing substantially better in Q3 than their Q2 realizations in the low $70's. If we take their exit production and add $8.00 to realizations, we could be seeing EBITDA in the $2 bn to $2.2 bn range. That would probably deliver that analyst high point in the upper $80's, putting a potential ~30% gain on the table.

MTDR doesn't pay much of a dividend presently. $0.60 is less than one percent at today's valuation, and there's no variable in place to provide a boost. Nor is there a share repurchase plan. All capital has been going toward funding the drilling program and keeping debt in line- Less than 1 turn of EBITDA. Joe Foran commented on the dividend and possibility of enhanced shareholder returns:

We want to do that in a responsible fashion and we'd like to work towards that achievement and being recognized as a company who steadily increases its dividend year-after-year. But to do it in a way that's financially responsible.

So, we've raised it from a nickel a quarter to $0.10 to - in the last couple of years to $0.20 and we will as I've mentioned at the Annual Meeting, we're going to look at this at our third quarter Board Meeting and see if prices are stable and they how the economy and the outlook goes, taking all those factors again, we would like to be able to raise it.

With a float of 120 mm shares, I don't see share buybacks as a big priority and think the company is on the right track to emphasize dividends and debt reduction.

Accordingly, I would join the analysts with a BUY rating on Matador Resources Company at current prices. If you have some dry powder, MTDR may just fit into your personal portfolios.

Comments