I want higher gas prices...and I want them NOW.

zdravinjo

Introduction

Birchcliff Energy Ltd. (OTCPK:BIREF) is a Canadian energy company with a production base that runs lopsidedly to natural gas. The last time we covered them in May of 2022, we thought the company was in a buy zone near $8.00 per share.

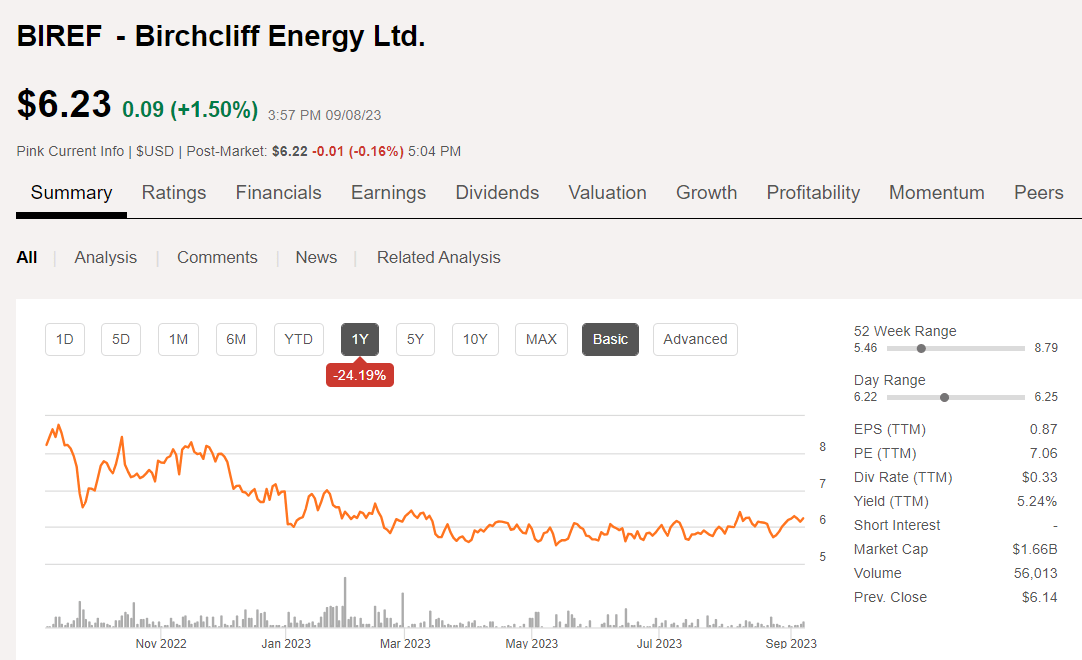

BIREF price chart (Seeking Alpha)

That call looked ok for about a month as natty rallied in the $10 MCF range, and the stock rallied into the high $9's. It quickly began to age out as gas futures began to suggest the bottom was about to drop out of the commodity. Sure enough, it put in a double top in November, then sank like a stone into its current range.

For most of this year, BIREF has traded in the upper $5s to mid-$6s, the upper end of which it is now. Since late August, it's made most of the current move toward the upper end of the range, along with many other gas producers. This absent any real move by the underlying commodity, still languishing in the mid-$2's thanks to an abundance of gas in the lower 48, and the fact the Coastal Gaslink pipeline still isn't up and running yet.

That being the case, we think it will be difficult to sustain this rally for the next month or so. Longer term, we can make a case for Canadian inventory concerns driving prices higher as we noted in the recent Crew Energy article. That spells opportunity at a price, so let's catch up with the company and see where and if we might want to stick our toe in.

The thesis for Birchcliff

BIREF has choice acreage in the heart of the Montney-Doig that provides thick reservoirs that lend themselves to pad-style development. Pads are the industry's innovation to maximize reservoir performance and EURs through optimal well spacing and pressure management. Most of BIREF's capital program is directed in the established Pouce Coupe and Gordondale. Elmworth is still in the prospective stage and provides room for further growth as gas rebounds in 2024.

BIREF Montney/Doig Footprint (BIREF)

Q2 financial notes and guidance

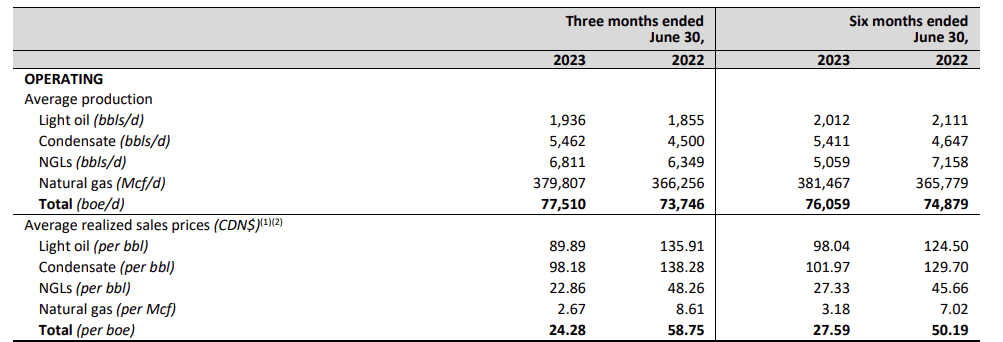

The company managed to raise production overall, 77,510 BOEPD for Q2. Production was heavily weighted to gas, but light oil and condensate saw gains as well. Price realizations for condensate boosted revenue, but the low price for gas dinged revenues sharply.

BIREF Filings (BIREF)

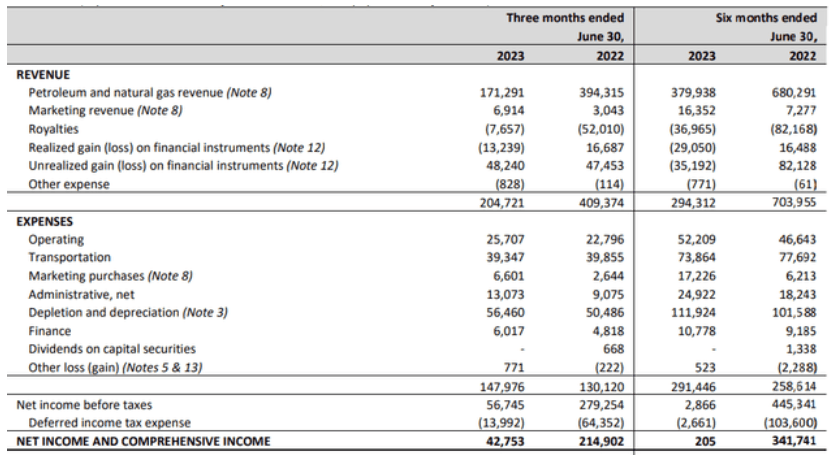

Pricing comparables were off on the three- and six-month periods versus those for the prior year, but the company managed to raise production overall. Price realizations for condensate boosted revenue, but the low price for gas dinged revenues sharply. Revenue dropped to C$171,291 from oil and gas sales, but overall revenue was aided by an unrealized hedging gain of C$35 mm. Cost management in the face of rising inflation of oilfield services enabled positive cash flow of C$0.16 per share.

BIREF Filings (BIREF)

Capex of $65 mm and the dividend outlay of $53 mm wasn't covered by cash flow $62 mm, suggesting the company turned to cash reserves or credit lines to cover these expenses. A payout ratio of 124% is not a scenario conducive to investors looking for yield. But things could be getting better in the near future.

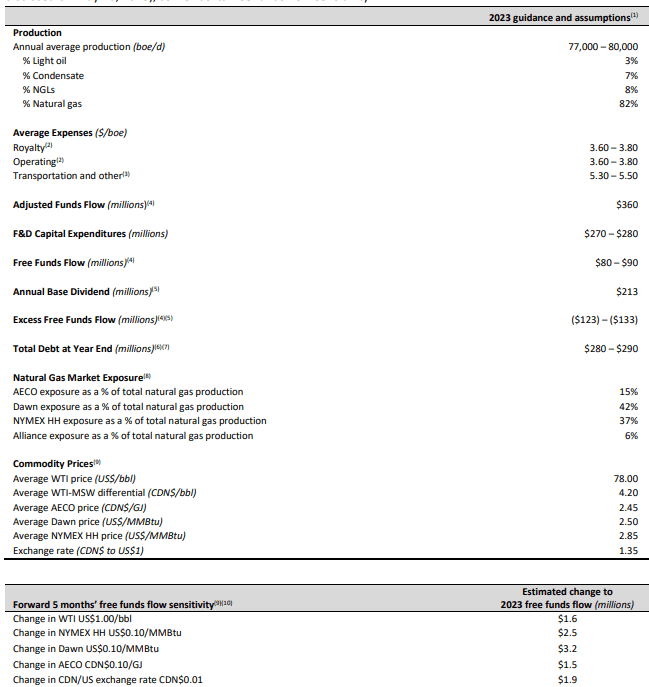

Guidance

These concerns could be a 2023 story if the company's forward guidance bears out. Both Henry Hub and AECO prices are forecast to rally to significantly higher levels in 2024, providing a significant boost to revenues and taking pressure off cash flow to cover key expenses, like dividends.

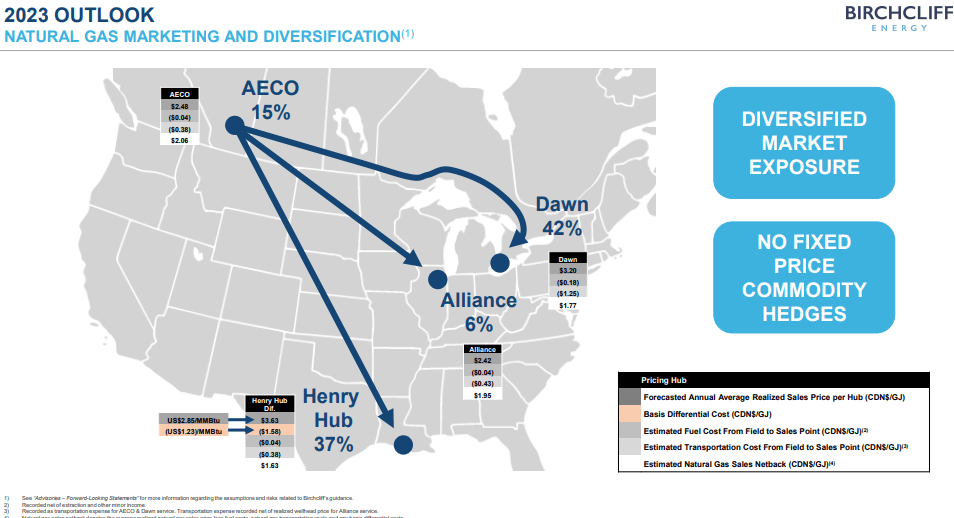

BIREF Marketing strategy (BIREF)

BIREF Filings (BIREF)

Just doing some back-of-the-envelope ciphering, if 15% of output goes to AECO at projected midpoint AECO price of ~C$3.30, revenues of $16,800 could be generated. That compares very favorably with the $12.8 mm the current AECO price generates, call it a 30% bump. If those prices bear out, Birchcliff could rock and roll in 2024.

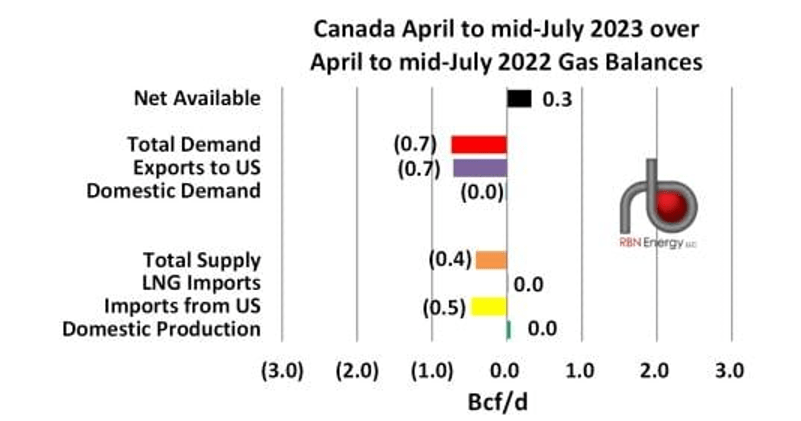

A catalyst coming in late 2023, early 2024

You've heard this before in the Crew article. Storage in Canada is much lower than for the same period in 2022. That could drive pricing higher and boost shares of BIREF accordingly. This graphic from RBN Energy highlights this change.

RBN Canada gas storage (RBN Blog)

Risks

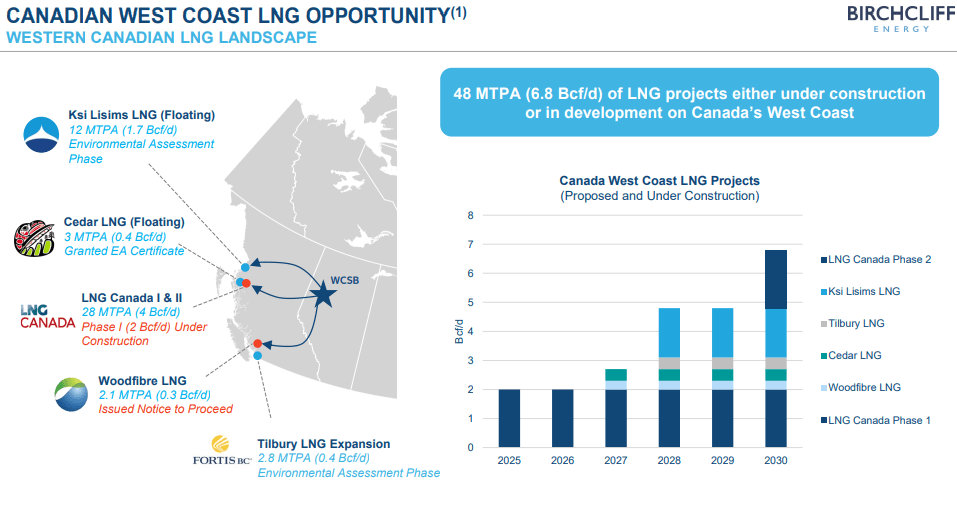

Gas is a minefield as we all know. One of the linchpins of BIREF's strategy-same for all Canadian gas producers is export to the West Coast Canadian LNG market through the soon-to-be-completed Coastal Gaslink Pipeline. Currently shown at 91% complete as noted in a recent Reuters article, that's still quite a bit to do. Nothing is done until it is done, particularly when it comes to pipelines. It's worth noting that none of the LNG projects for which the coastal gas link is being built are up and running. Meaning there is plenty of time to finish before gas sales would be cannibalized.

BIREF LNG strategy (BIREF)

Another risk could be U.S. sales. BIREF notes 42% of sales going through the DAWN hub. Chockablock U.S. inventories could put a crimp in those numbers, as we have noted rising production from the Permian seeking outlets. Just something to keep in mind.

Your takeaway

Birchcliff's size gives it some clout. Knocking down nearly 78K BOEPD is significant. That footprint comes with low costs that helped keep margins in the positive ledger even as revenues declined by 50%. That spells performance and gives some confidence as to management's ability to execute.

The dividend payout of $0.60 USD per share equates to a 9.6% YOC, making it fairly attractive to buy in and wait for the increases and stock buybacks that will surely come in 2024. Assuming price projections bear out as have discussed.

As of now, BIREF is trading at an EV/EBITDA multiple of 3.77X, which like Crew compares very favorably with some U.S. shale E&P's we follow. On the flowing barrel basis we so commonly use, it's attractive as well at $23.5K per barrel.

Eric Nuttall opined on BIREF recently, with a pass due to limited upside calculations. Although he saw a 46% upside, which might tip the balance to take a position. Other analysts are also a bit tepid with an Overweight rating, and C$ price ranges from $6.25-10.40, and a median of $7.50. The trading volume normally is in the 10-20 share-a-day range. Yesterday it ran up to 200K on the buy side, after a 50K share day on the buy side. That spells smart money to me, and we like to keep company with those guys.

I think Birchcliff Energy Ltd. rates a buy ahead of earnings subject to your individual risk tolerance. I think the selloff in the shares is done with the assumptions we are making today, and if the recent momentum is any guide, the shares could rally.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Comments