wwing

Introduction

Crew Energy Inc. (OTCQB:CWEGF) is a Canadian gas-oriented producer that we last wrote up with a strong buy in the low $3's in February, noting however the macro environment for gas might make growth difficult over the short haul. That's still true, but there are some catalysts with a 3-6 month timeline that could change the story.

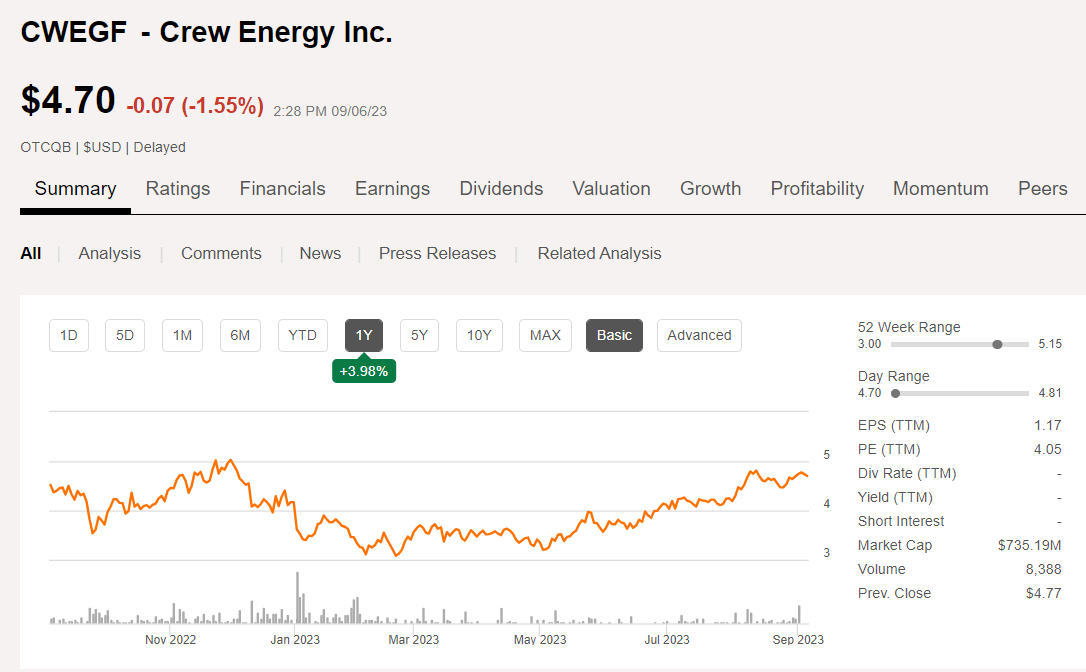

Crew Energy price chart (Seeking Alpha)

That wasn't a bad call, as the company has rallied to the upper-$4's, before making a slight pullback. Analysts are fairly bullish on the stock with an overweight rating that's a little inconsistent with the price target ranges-$6.5-9.25, and a median of $7.63.

On a technical basis, the action seems bullish, with some recent buying days well above the average trading volumes. It's been staying above the 50-day SMA, and if this ascending triangle pattern continues, could be ready to retake the $5.00 threshold. Or it could flop over into a head and shoulders pattern before moving back to the $4.20 level.

If those analyst price targets can be justified, Crew might be attractive at or near current levels. Even the low point would represent a ~50% move higher and justify our capital. Let's dig in a little deeper.

The case for Crew Energy

Crew drills in the gassy and gas-liquids rich section of the Montney shale. The Montney is stacked in this region, giving the operator a lot of flexibility with completion designs. As the slide below notes, many of the lower B and C units are undrilled minimizing interference and preserving reservoir pressures. This promotes higher EURs, which lengthens the life of the field. Crew estimates a total of 2,500 drilling locations across its major plays-Septimus, Tower, and Groundbirch.

Crew Inventory chart (Crew energy)

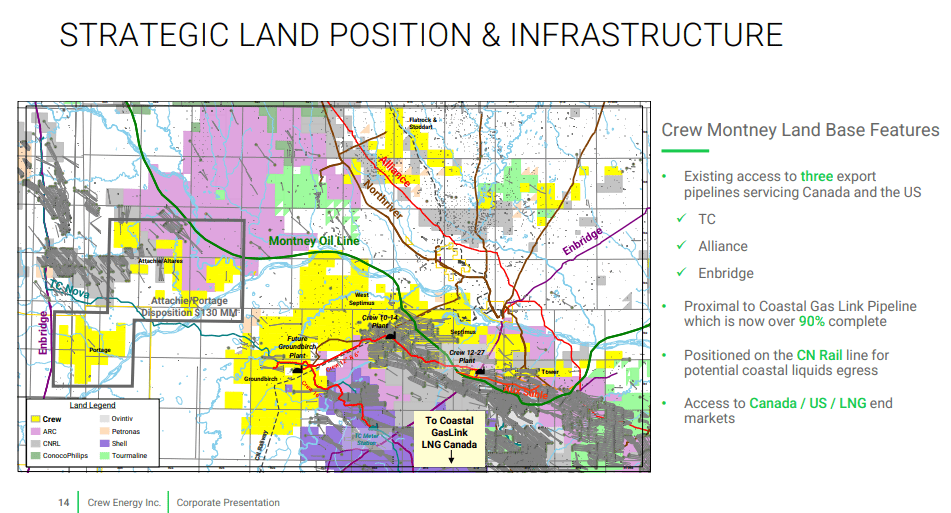

Real estate is all about location. So too is land on which oil and gas wells will be constructed. As I have mentioned many times, the more blocky and contiguous the acreage is, the easier and cheaper support logistics become. Takeaway is always a concern to get production to market. Crew ticks this box as well.

Crew Strategic Land base (Crew Energy)

The Greater Septimus and Tower fields show the quality of the rock. We have unbroken shale through the B and C zones. Crew will commission 5 ERH and 7 Ultra-Rich Condensate-UCR, wells in the second half. A waste heat recovery project will generate another 5,000 BOEPD.

The company plans to grow production to 60K BOEPD in the next several years, and is focusing on liquids rich sections of its acreage base. This could double EBITDA and justify a substantial move higher in the company's stock price.

A potential catalyst for Crew

Over-production and full storage caverns have dogged the price of natural gas for a year now. The success that the EU countries had loading up with LNG and installing degasification terminals in the second half of 2022, put a crimp on gas prices, to put it mildly. Once it was clear that Europe was going to have a warm winter, the price of gas nose-dived and has pretty much remained in the basement since. And, that's hurt the stock prices of gas drillers below and above the 49th parallel.

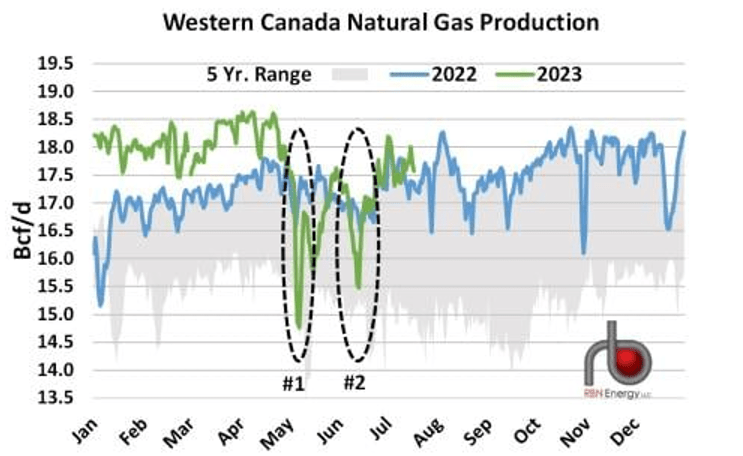

Things might be changing. Energy analyst firm, RBN Energy, noted in a recent blog post that the Canadian market had tightened appreciably, primarily due to the shut-ins from the wildfires in spring.

Western Canada Gas Production (RBN Energy)

Canadian supply has declined from nearly 2 BCF/D in April 2023 to just 0.3 BCF/D as we head into storage season. The article notes the potential impact as we move toward injection season.

If the current situation of 0.3 Bcf/d of oversupply were to persist for the remainder of the injection season (to the end of October), the Canadian gas market would have a modest 0.3 Bcf/d more gas on hand to inject into storage than last year, a somewhat more manageable situation than in April when the oversupply was much larger near 2 Bcf/d.

RBN.

I am certainly not stipulating a cause and effect scenario here. Just noting a positive lever for the commodity that if we do a get a winter this year, might boost the stock.

Next the company's plans for the second half of 2023 emphasize UCR drilling. A total of 12 new wells in the Septimus area will boost liquids production going into Q-4 and 2024. This will increase Crew's light oil and condensate production to over 7,000 bbls per day by year-end 2023. They will Drill 17 UCR Montney wells; turn 13 to sales, and hold an inventory of 11 drilled and uncompleted UCR wells at year-end 2023, ready to hook up in early 2024.

Crew Q2, 2023 financials and Guidance

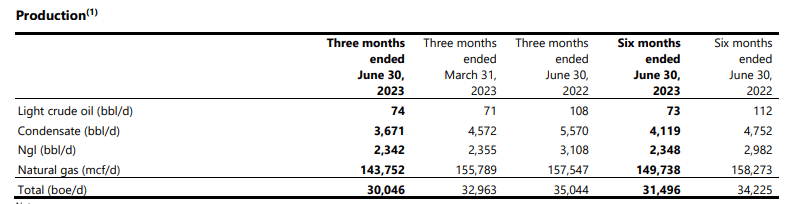

30,046 BOEPD in Q2 2023, was at the high end of Crew's previous quarterly guidance of 28,000 to 30,000 boe per day. This was thanks to continued strong performance from wells drilled and completed at the end of 2022 and early 2023, while first half 2023 production averaged 31,496 boe per day. Relative to the same periods in 2022, lower volumes reflect shut-in production due to weaker natural gas prices, as well as limited completion activity in the first half of 2023 while the Company focused on debt reduction. It should probably be noted the wildfires played a role here as well.

Crew Production table (Crew Energy)

Comparables were also off QoQ reflecting weaker pricing during the second quarter. The company did what it could with its gas weighted production in terms of shifting it to markets for incremental gains.

Crew Oil and Gas sales (Crew Energy)

As in Q1, hedge gains were a significant source of income in Q2, yielding $11.8 mm.

Crew Hedge gains (Crew Energy)

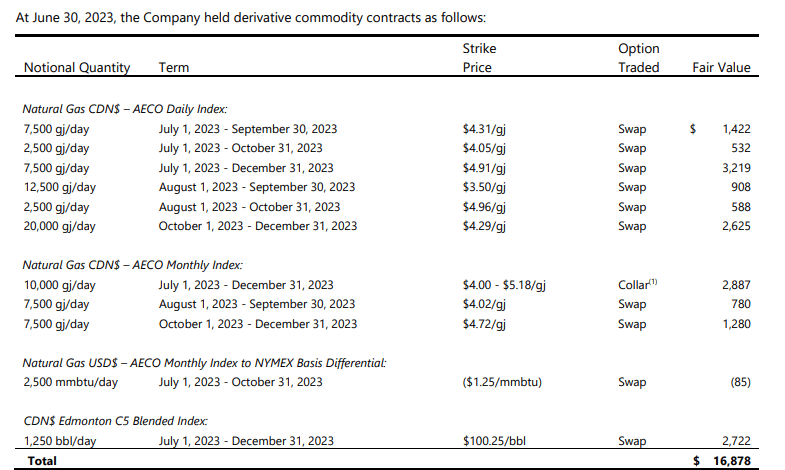

The company remains hedged with a maximum of about 8% of its daily output hedged as noted below.

Crew Hedges (Crew Energy)

Other financial metrics for the quarter

Crew had $59.0 million of Adjusted Funds Flow-AFF per $0.36 per fully diluted share in Q2 23, and $133.6 million-$0.83 per fully diluted share in the first half of 2023. AFF benefited from the monetization of approximately $11.8 million of natural gas hedge contracts in the quarter. AFF margin as a percentage of petroleum and natural gas sales totaled 89% in Q2 2023 and was 80% overall in first half of 2023.

Operating netbacks averaged $23.43 per boe in Q2 2023 and $25.40 per boe in 1H/23, assisted by realized hedging gains of $8.87 per boe and $6.71 per boe in Q2 2023 and the first half of 2023, respectively.

$36.7 million of net capital expenditures invested in Q2/23, including the drilling of six ultra-condensate rich ("UCR") wells at Greater Septimus.

Net debt was reduced by 42% compared to Q1-2023 to a total $60.7 million at quarter-end. Crew reduced net debt to trailing last twelve-month ("LTM") EBITDA by 50% to 0.2 times at June 30, 2023, from 0.4 times at year-end 2022.

The company ended the quarter with $28.9 million drawn on their $200 million credit facility, with a new maturity of May 2025.

They redeemed the remaining $172 million principal amount of their 2024 Senior Unsecured Notes at par on April 28, 2023, using cash on hand and drawings on the previously mentioned $200 mm bank line.

Cash costs per BOE of $9.68 in Q2-2023 were in-line with $9.63 per boe in the same quarter of 2022.

Q3 2023 Guidance

Capex in Q3 2023 is forecast at $115 to $125 million with average production of 26,000 to 28,000 boe per day. In Q3, they will complete the five well 4-32 pad. Complete the last remaining well on the 11-27 UCR pad. Finish drilling and begin completions on the seven wells 2-24 UCR pad. Then begin the drilling of a five (5.0 net) well UCR pad at 6-18.

Long-term drillable reserves base

With 2P reserves of 31 years at current production rates, the company runs little risk of out producing the capability of its acreage to sustain it. It should be noted that the company plans to increase production up to 60K BOEPD by year exit 2026, cutting that reserve life roughly in half. That still is quite a substantial buffer and its Groundbirch development project could extend that base significantly.

Crew Energy Reserves (Crew Energy)

Your takeaway

Crew Energy Inc. is trading at an attractive EV/EBITDA multiple of 2.94X. On a flowing barrels basis, the value is $24K per barrel. Both of those compare very favorably to U.S. shale producers. Crew has dramatically paid down its debt and has no near term maturities that could create a problem.

The company has a history of beating estimates by substantial margins, mostly recently in Q2 clobbering the analyst call for $0.12 per share by $0.09. The rally in the stock from the low $4's on earnings release is certainly attributable to that beat.

That puts some risk in delaying entering the stock should we choose to do so. None-the-less after the massive 50% rally since May, I am not inclined to chase it at current levels. Accordingly, it gets a hold at current prices. Any weakness back toward early August levels in the $4ish range would be a definite buying opportunity that would be hard to resist.

There aren't any near-term catalysts for the next few months until we see what the weather is going to do. Thus, I think the appropriate strategy for Crew is to monitor for that ~$4.00 entry level.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Comments