miniseries

The S&P 500 (SPX) has had a rather strong year so far, with returns of 17% year-to-date.

Data by YChartsThis was despite concerns that the US may go into a recession as early as the first half of 2023, but clearly, markets continued to power through as corporate earnings were better than expected and new drivers of the stock market like generative AI were introduced and well received by the market.

Here, in this article, I am not attempting to predict the macro backdrop or future of the economy.

I think that predicting the macro is the job of economists and even economists get it right half the time. As a result, I don't think that this exercise is very much useful for a bottom-up investor.

As a bottom-up investor, my job here is to look for companies that are undervalued based on their current fundamentals, and these are the opportunities or predictions that I think is a more consistent way of making money.

The focus of the article here is to provides us with a sense of where we are today, taking an objective view of the market to know where we are in the market cycle.

Let's first look at how the US consumer is faring.

How is US consumption doing?

The general consensus about the US consumer today is that while the Federal Reserve has been aggressively tightening monetary policy, the US consumer has remained surprisingly robust.

I say surprisingly here because logically, when rates are high and the monetary policy is tight, consumers tend to reduce their spending.

In this case, the surprisingly robust US consumption is the main reason why US growth has been stronger than forecasted in 2023.

The main explanation for the strong consumption trend so far is the large amount of stimulus payments paid out during the pandemic.

And that meant that even with higher interest rates, consumers still had money to spend, thus muting the effects of these higher interest rates.

The first question then is how much extra cash do US consumers have today and will that continue to drive consumption?

For this, we have to turn to the aggregate personal savings trend. It is clear that we had huge accumulated excess savings of $2.1 trillion to spend from 2020. However, much of that has already been drawn down, with $1.9 trillion having been depleted by the end of the first quarter of 2023.

Aggregate personal savings vs pre-pandemic trend (Bureau of Economic Analysis)

This implies that this positive effect of the stimulus payments on US consumption is actually running out or may have already run out by now.

This is actually a worrying sign to me because I have been seeing a robust US consumer trend relative to other countries, but given that excess savings have been depleted, this might signal a turn for the worse in US consumption.

I looked around for other trends about how the US consumer might be doing and they all do suggest a worsening situation.

Firstly, for credit card delinquencies, while it is a distance away from the global financial crisis numbers, the delinquencies are rising, especially amongst the younger age group.

While not yet at alarming levels, this does signal a growing strain on the US consumer's finances.

Credit card delinquency (Ned Davis Research)

Secondly, another trend that is worrying to see is that there is an increasing trend of use of "Buy Now Pay Later".

While the number of "Buy Now Pay Later" flourished in the pandemic and more consumers are embracing it, the use of "Buy Now Pay Later" payment methods presents a classic sign that US consumers may be indeed depleting their cash reserves.

Use of Buy Now Pay Later (Apollo Group)

While both these trends do not yet signal a dire situation, they do suggest the US consumer is facing increasing financial strain as excess savings run out.

As we take a step back here, it is important to realize that from the US consumer point of view, there are more headwinds to come in the near-term given that not only has the excess savings been depleted, but also that there are increasing signs of a worsening situation for the US consumer. This has consequences on consumer sentiment in the near-term and could derail the strong rally we had in the S&P 500 in the year so far.

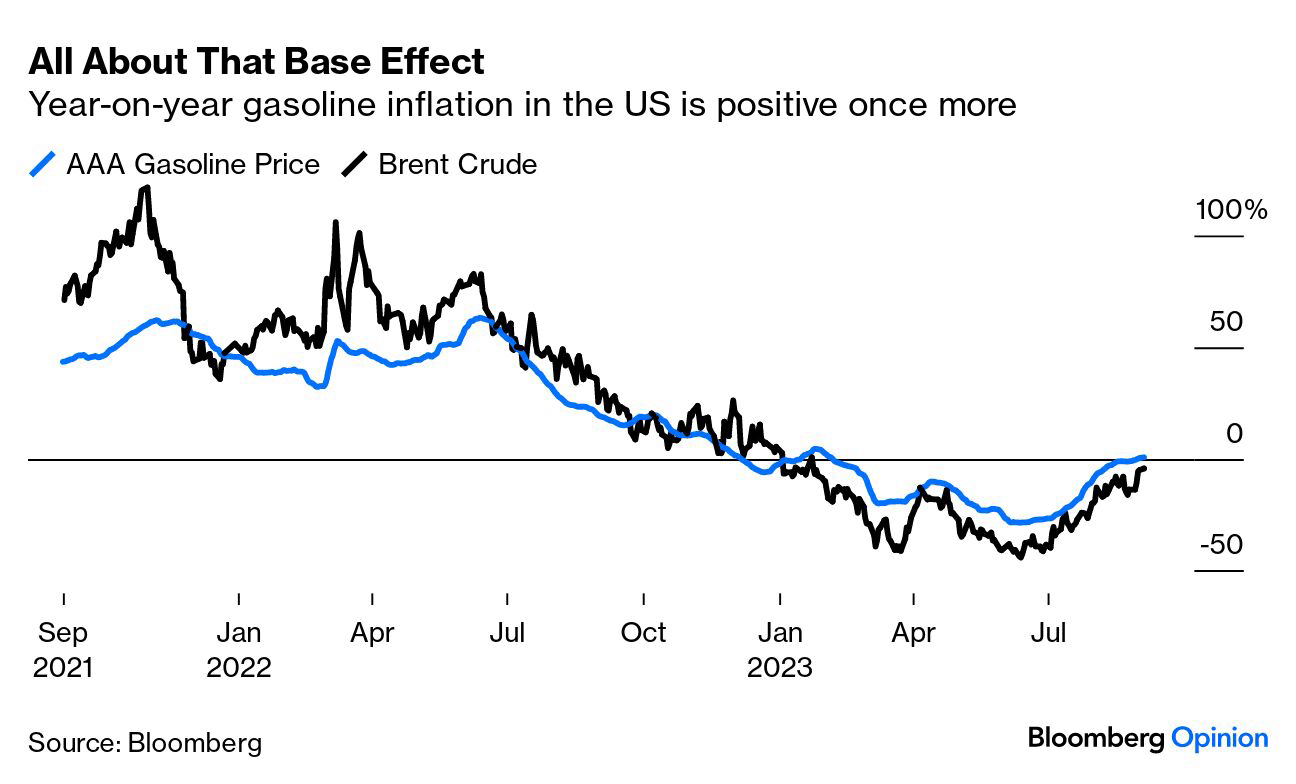

Oil inflation coming back

Brent crude topped $90 for the first time in more than a year and been on a climb since July this year.

As a result, we can see below that oil inflation is back on a year-on-year basis.

This comes as Saudi Arabia and Russia reiterated that they continue to limit supply.

This return of oil inflation is likely to make a dent on US consumption as trips to the pumps become more painful to motorists in the US.

Gasoline inflation (Bloomberg)

While I tend to focus more on core inflation, oil inflation is no doubt a part of the inflation equation and as the price of oil continues to climb, this implies a tougher fight against inflation.

On top of that, with the US consumer expected to feel more headwinds as mentioned earlier, this return of oil inflation adds to the woes of the market.

Labor market

And of course, even if excess spending of the US consumer is depleted, or if oil inflation is back, this can be offset if employment or the labor market remains strong.

The Fed has been focused on brining jobs growth back to more normalized levels so that inflation can move towards its target.

The good news for those not wanting to see the Fed raise rates any further is that the US non-farm employment growth is now at the pre-pandemic level, as can be seen below.

US non-farm employment growth (BLS, Haver Analytics, Deutsche Bank)

While this is encouraging in that the data dependent Fed may have one more reason to not raise rates any further, this poses another potential problem.

At the current high rates, if rates stay this high for long, there is a concern that the growth trend in non-farm employment will continue to decline.

And if it does decline, there is the concern that the decline in non-farm employment growth goes out of hand and that the soft landing that we were all expecting becomes less of a reality.

In my opinion, this is the tipping point here. While worsening non-farm employment growth is definitely adding to the market woes, if it plunges or drops further than expected, this could result in a huge setback for the S&P 500.

China's effects

The economy in China seems to never lack negative news.

Country Garden Holdings, one of China's largest real estate companies, is in a liquidity crisis, with the company barely avoiding default recently.

One of its largest shadow banks, Zhongzhi Enterprise Group, missed dozens of payments on multiple high-yield investment products.

On top of that, more than one in five young people are out of work, consumer spending is weak, exports are also struggling, and its economy is decelerating.

While more supportive and expansive policies and measures are China's measures to shore up a faltering economy, more support expected to come, the question is how significant this will be and how fast will this be implemented.

China has been rolling out some supportive policies for the real estate sector, to help the sector through this period of difficulty.

The current state of the Chinese economy may have consequences for the global economy as we have seen exports are weak, implying a weaker global economy, and a weaker China is bound to impact the global economy in profound ways given it is the second largest economy in the world.

As a result, China's problems are also the world's problems and could add more near-term headwinds to the market is unresolved or if it worsens.

Conclusion

We are in a tight monetary policy environment, with rates at high levels, there will be consequences in the economy and on the consumer.

Thus far, the US consumer has been rather resilient, but I think we are starting to see some of the tailwinds that provided that resilience tapers off.

There are signs that we could see a worsening US consumption trend in the near-term given the headwinds.

With a weakening labor market, oil inflation returning and the world's second largest economy weakening as well, there looks to be near-term headwinds from where we are today.

Like I mentioned at the start, I do not attempt to time the market and be a predictor of the macro environment. My job here is to identify mispriced opportunities and positively skewed risk reward opportunities today, and that's where the outperformance will shine the most in the long-term.

However, this article does highlight the fact that the growing market woes are becoming hard to deny, and they do pose risks in the near-term for the overall market.

Comments