choi dongsu

Self-driving has been the talk for a long time now.

One of the names often mentioned in these talks include Mobileye (NASDAQ:MBLY), one of the leaders in the industry.

Today, in the article, I will dive deep into Mobileye and explain why I think Mobileye is a highly differentiated player and a leader in the space.

Let's start looking into Mobileye!

Brief introduction

In 1999, Mobileye was founded by Professor Amnon Shashua. In the early days, Shashua worked with two close friends, Ziv Aviram and Norio Ichihashi. Aviram was in charge of the operations, finance, and investor relations while Shashua was in charge of the strategic vision, technology, and R&D of the company. Ichihashi was in charge of the Asian market, which was Mobileye's first market.

In 2014, the company went public, and in 2017, Intel (INTC) acquired the company. After the acquisition, Shashua became the CEO and Aviram retired. Also, under Shashya's supervision, Dr. Gideon Stein completed his doctoral studies at MIT and was asked to lead to R&D for Mobileye.

Since its founding, Mobileye has led the mobility revolution by using its expertise in machine learning, computer vision, mapping, its purpose-built EyeQ SoC, and data analysis.

The company's technology has enabled a comprehensive portfolio of Advanced Driver Assist ("ADAS") and Autonomous Vehicle ("AV") solutions. At the end of the day, its solutions are meant to bring about not just autonomy but safety.

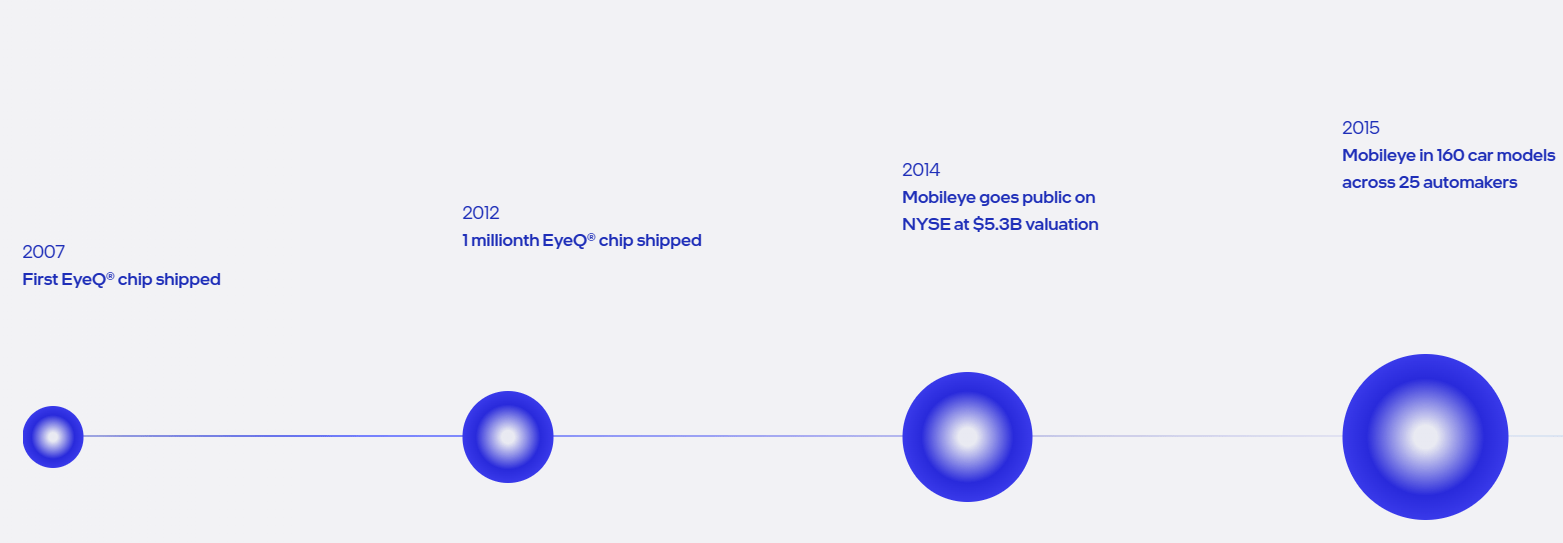

Mobileye is focused on ensuring its technology is scalable, low cost, and efficient. in addition, the company currently is profitable and growing rapidly, while having the experience of working with more than 50 automakers in the world. As can be seen below, these are the key milestones of Mobileye.

Key milestones of Mobileye (Mobileye)

Strong suite of products

When I think of Mobileye's product suite, I see it as building blocks that range from ADAS to autonomous vehicles ("AV") and these building blocks are scalable and utilize the company's advantages in data and its experience to custom design high-performing and low-cost solutions.

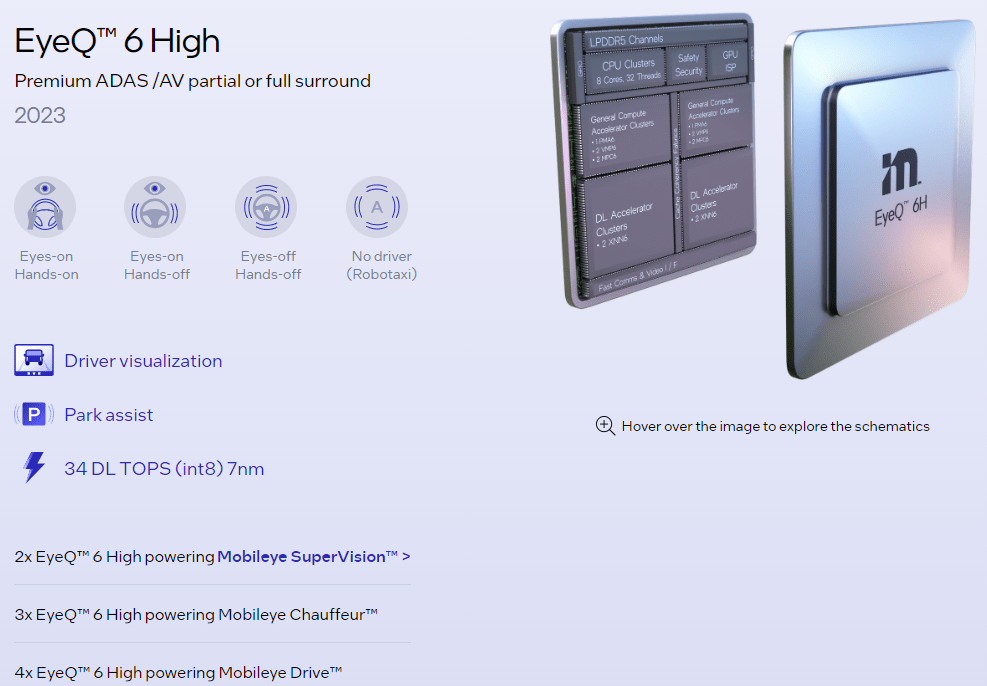

Firstly, at the core of all Mobileye offering is its purpose-built EyeQ SoC. The EyeQ chip is a scalable and automotive-grade SoC that is tailored for the needs of ADAS to AV. The current EyeQ portfolio includes EyeQ 4 that is meant for core ADAS, EyeQ 5 that is meant for premium ADAS and EyeQ 6 that is meant for premium ADAS and AV. As Mobileye progresses along the EyeQ series, the company continues to use its know-how and expertise to design a chip for customers that has the maximum efficiency to enable them to manage power consumption and costs.

EyeQ 6 (Mobileye)

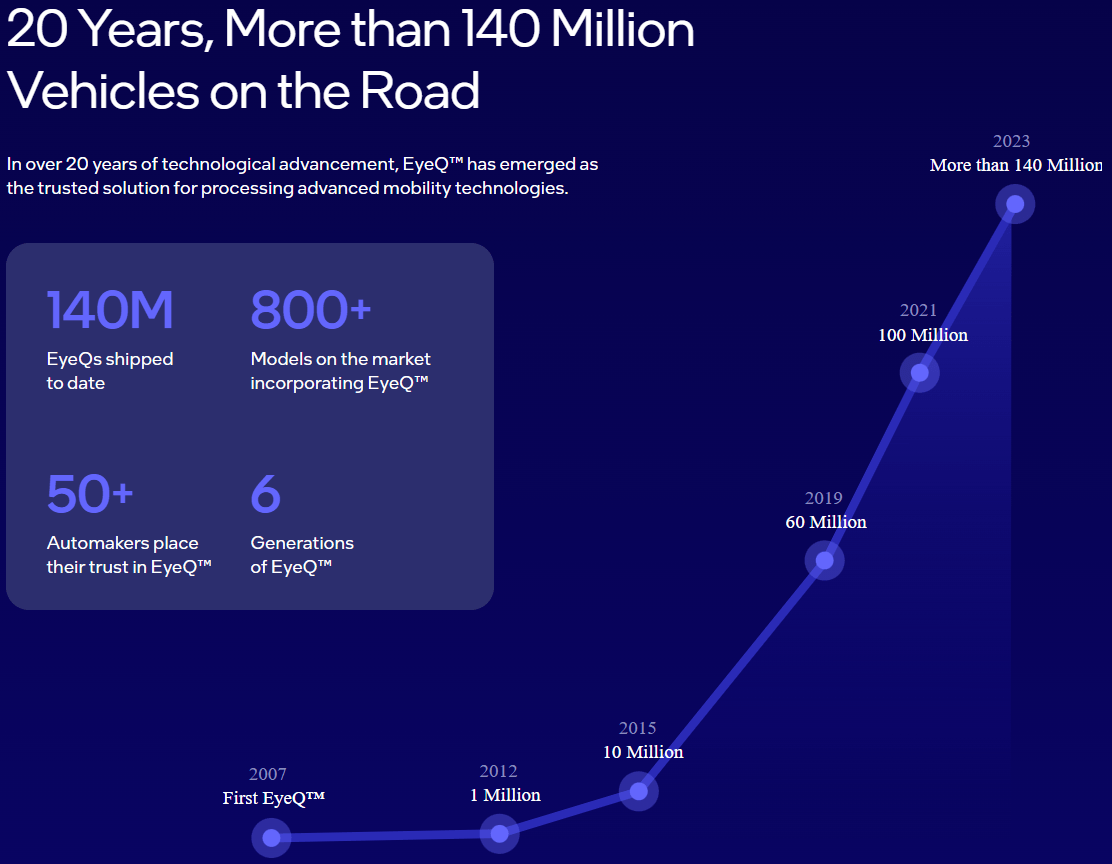

As can be seen below, after six generations of EyeQ, more than 50 automakers have incorporated EyeQ into their vehicles and more than 800 models have used EyeQ in their vehicles. After more than 20 years of technological improvements, there are now more than 140 million vehicles on the roads that use EyeQ.

EyeQ success (Mobileye)

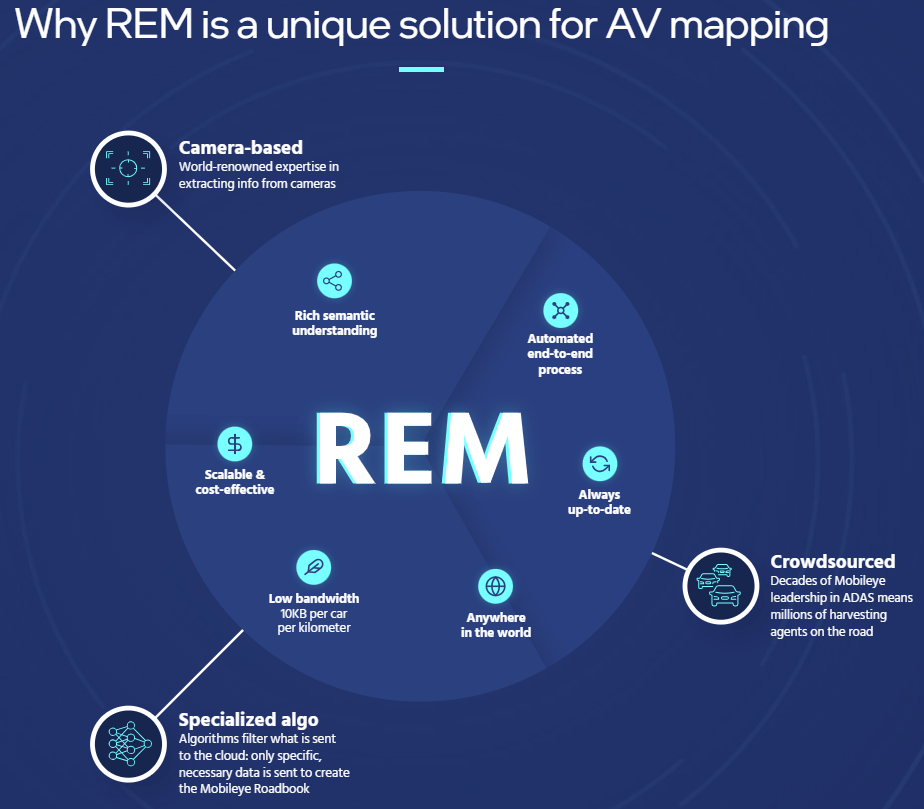

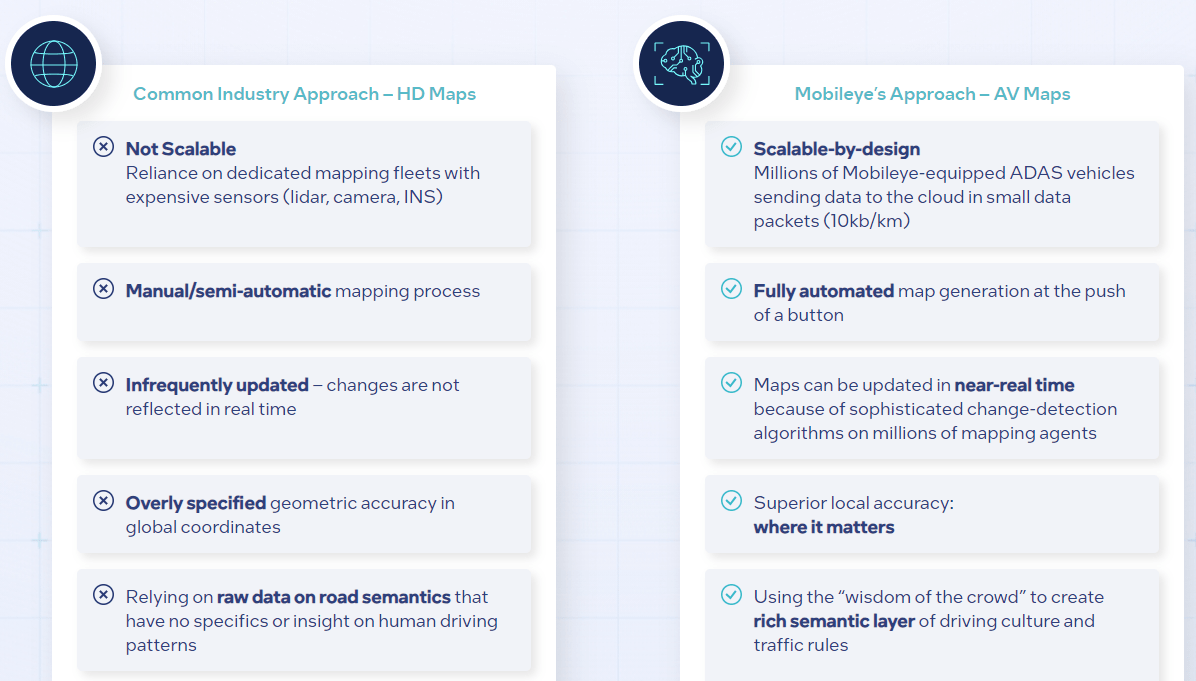

Second, Mobileye offers customers it's what is called REM, or Road Experience Management, which is its crowdsourced mapping layer. Mobileye's REM is a unique solution for AV mapping because it is camera-based, crowdsourced, and uses specialized algorithms. The result is a low-cost, scalable solution that leverages the network effect of large datasets.

Mobileye's REM for AV mapping (Mobileye)

Mobileye's REM crowdsourced maps are available for enhanced ADAS, SuperVision, and consumer AV offerings. The maps are essential for providing a critical intelligence layer for onboard sensors and bring additional data on the drivable paths. At the end of the day, this is another way in which Mobileye differentiates itself as its AV maps allow for fully automated map generation, that can be updated near-real time, with superior local accuracy and it is highly scalable as well.

Mobileye AV maps vs common industry approach (Mobileye)

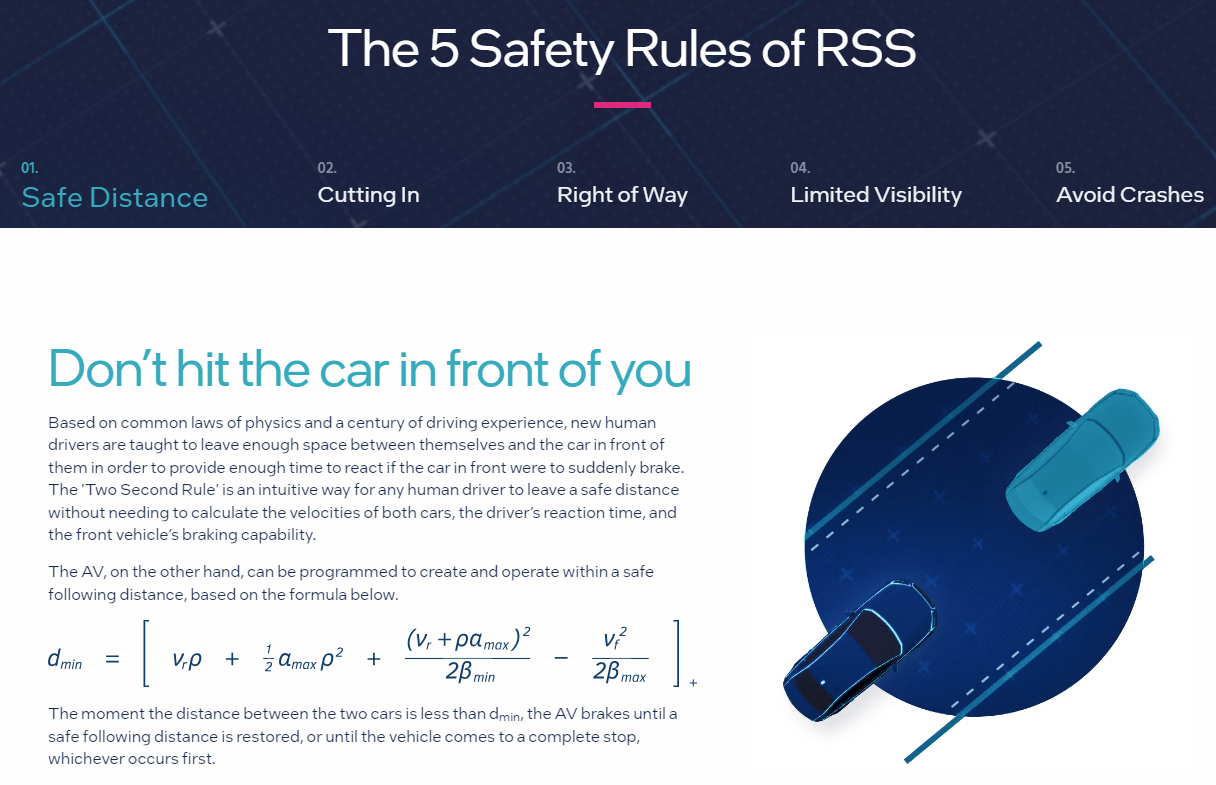

Third, Mobileye offers RSS, which stands for Responsible Sensitive Safety, which is a formal model that governs safety and assumes the worst-case assumptions for other road users. This is currently only available on SuperVision, consumer AV, and RoboTaxi applications. RSS is essentially a framework that governs the driving policy stack, in addition to the perception layers housed on the chip. It sets a formal model to govern the complex decision-making involved in automated driving applications. The end result is a driving policy stack that is safe, assertive, computationally lean, and highly scalable.

I highlight the five safety rules of RSS below:

- Don't hit the car in front of you.

- Don't cut in recklessly.

- Right of way is given, not taken.

- Be cautious in areas with limited visibility.

- If you can avoid a crash without causing another one, you must.

The 5 safety rules of RSS (Mobileye)

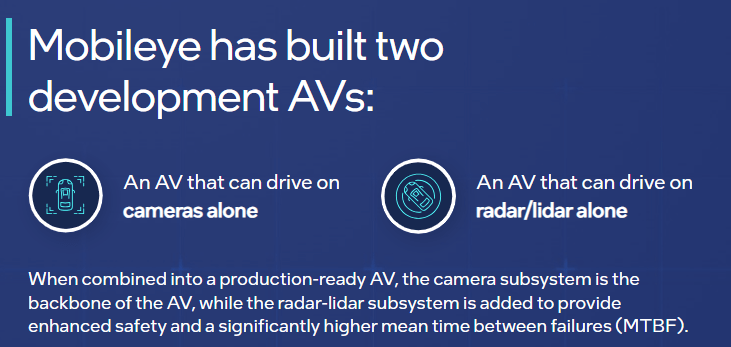

Fourth, when moving up to L4 applications, the need for additional redundancies results in the need for imaging radar or LiDAR subsystems. Mobileye is currently in works to develop an imaging radar and a Frequency-Modulated Continuous Wave ("FMCW") LiDAR. As many of Mobileye's SuperVision customers are likely wanting to add LiDAR and radar, I think we will see the company expand to radar and LiDAR offerings to SuperVision, consumer AVs and RoboTaxi applications starting in the middle of the decade.

Mobileye's approach is different from the current players in the industry because of something it calls True Redundancy. The Mobileye approach is different from that of the industry because the industry approach is that the camera and radar are complementary, meaning that both the camera and radar-LiDAR sensors combine their sensing of the environment into a single model. However, in Mobileye, they task each channel, camera, and radar-LiDAR to sense all elements of the environment and each channel has its own model, leading to two separate full models that are trained independently of each other to bring superior performance and easier validation.

True Redundancy (Mobileye)

Lastly, Mobileye's Autonomous Mobility-as-a-service ("AMaaS") also offers fleet management applications for customers. Some of these capabilities come from an Intel-acquired urban mobility app, Moovit. Moovit also brings another critical intelligence or data layer for Mobileye needed for fleet utilization.

SuperVision to be a key driver

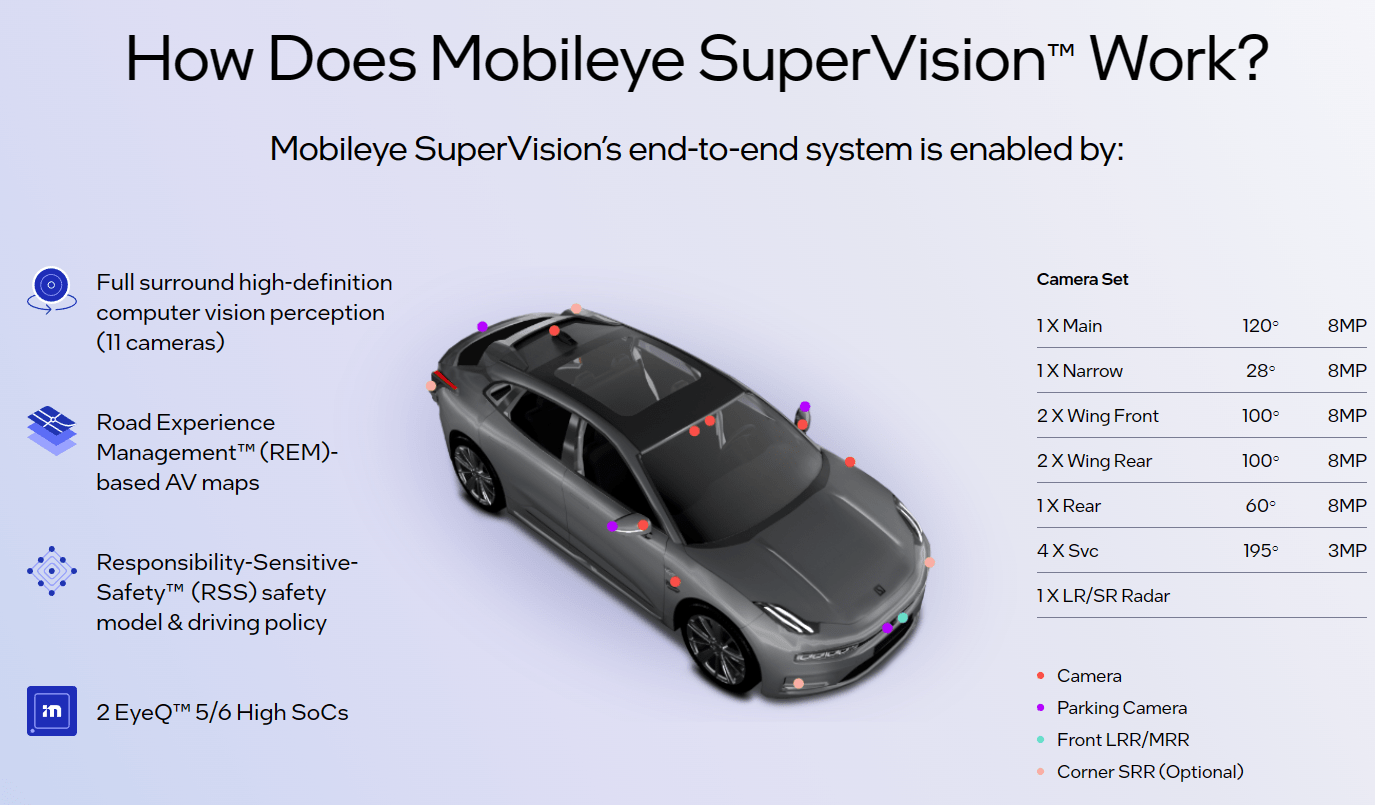

The Mobileye's technology suite is best featured in its SuperVision product line, which is not only on the road today but also gaining significant traction.

SuperVision is, in my opinion, the midpoint between ADAS and AV.

For SuperVision, there is a leap in safety as a result of the use of REM, the integration of Mobileye's RSS-based driving policy, and a robust surround sensor suite.

In addition, SuperVision results in a meaningful expansion of L2+ driving domains and potentially gets the consumers more used to such applications. Also, SuperVision has a reasonably low system cost and will enable an automaker to easily expand into consumer AV capabilities.

SuperVision (Mobileye)

Mobileye has multiple automaker customers lined up to launch SuperVision in the next three to four years. The company expects that there will be 1.2 million SuperVision based vehicles in 2026. In addition, out of its revenue pipeline of $17 billion for its ADAS business through 2030, $3.5 billion is expected to come from SuperVision.

Lastly, the company is in a large number of series discussions and development activities for SuperVision. There is a premium European OEM that began production development work in 1Q23 and the company is engaged in a concept development phase from a US OEM that is expected to lead to a design win at the end of 2023.

As a result, the disclosed awards for SuperVision include Zeeker 001, Zeeker 009, Polestar 4, another two unnamed Geely models, VinFast, a premium European auto OEM, and a potential US auto OEM.

I expect a domino effect of bookings and launches in the next few years.

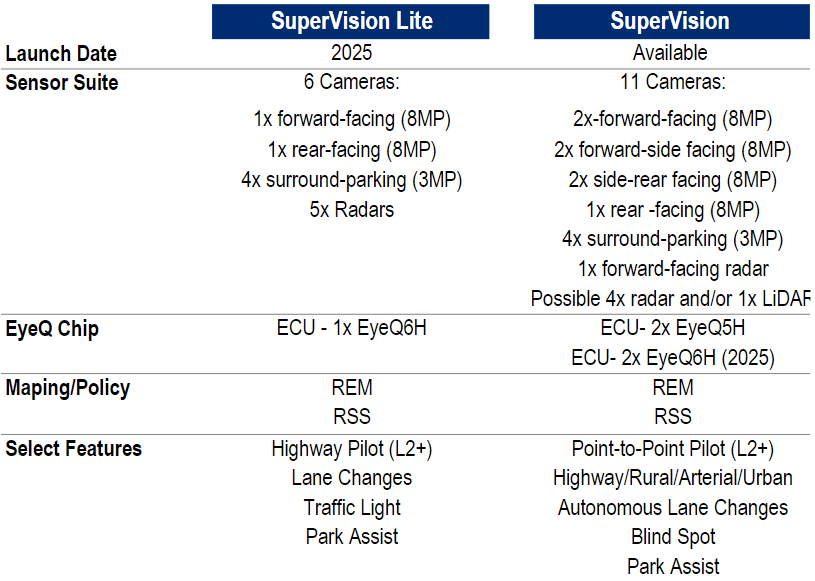

Below, we can see the difference in the sensor suite, EyeQ Chip, and features of the SuperVision, which is available today, and the SuperVision Lite that will be available in 2025.

Mobileye SuperVision Product Offerings (Mobileye, Citi Research)

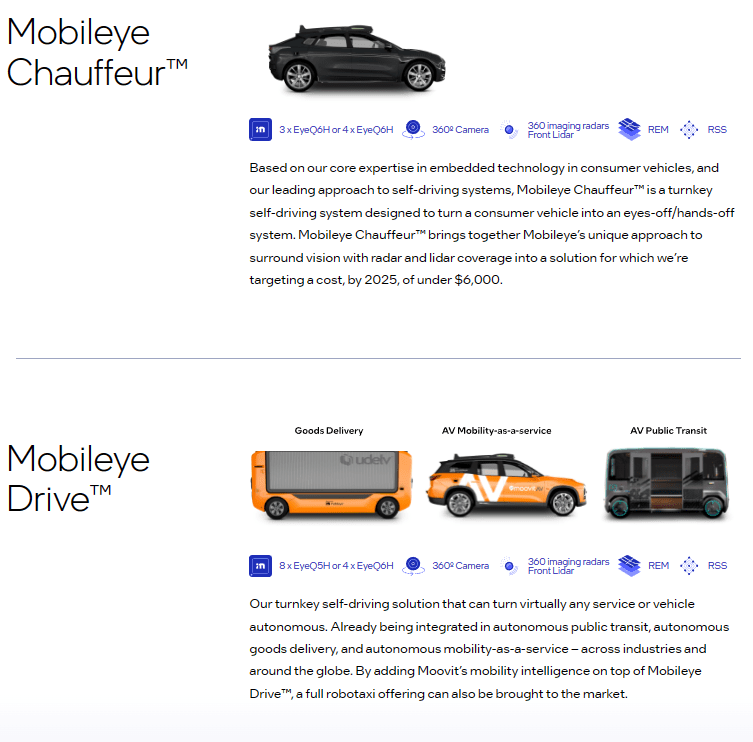

SuperVision is its " hands-free but eyes-on" solution, but it also has Chauffeur which brings about a not just hands-off but also an eyes-off solution to consumer vehicles. Lastly, there is Mobileye Drive, which is meant for offering autonomous mobility-as-a-service solutions and autonomous solutions for delivery of goods and public transport.

Mobileye Chauffeur and Drive (Mobileye)

Industry adoption and standards

You probably have heard of these terms in the autonomous driving world, from Level 1 all the way to Level 5.

Level 1 driving automation is the lowest level of automation also known as driver assistance. This is where the driver may be provided with a driver support system, which includes braking, acceleration or steering assistance. The driver remains responsible for driving here still.

Level 2 driving automation is also called partial driving automation where vehicles are provided with advanced driving assistance systems or ADAS, that help the driver take over certain functions like steering, acceleration or braking in certain scenarios. In the case of L2, the driver must still be alert and supervise the technology. Some examples of L2 include Highway Driving Assist available in Genesis, Hyundai, and Kia vehicles, and Tesla's Full Self Driving Capability technology is also a Level 2 system.

Level 3 driving automation is known as conditional driving automation and the jump from L2 to L3 is huge and till date, only the State of Nevada has approved the use of L3 for Mercedes-Benz.

L3 uses AI and the driver assistance systems to make decisions on the driving situation around the vehicle. The driver needs no supervise the technology in L3 but a driver must be present and ready to take control of the vehicle if needed during an emergency.

Mercedes-Benz is the first to receive L3 certification in the US in the state of Nevada with its technology called Drive Pilot and it states it is ready to deploy to all states in the United States when approvals are received.

Level 4 driving automation is known as high driving automation where it does not need human intervention as it is programmed to stop itself if the system were to fail. As such, there is no need for pedals or a steering wheel in a L4 vehicle. L4 is meant for RoboTaxis and public transport services as these vehicles will go from point to point.

The last level is Level 5, which is known as full driving automation. As the name suggests, the system will be able to handle the vehicle in all scenarios and conditions and does not require human intervention at all.

Valuation

Mobileye trades at 42x 2024 P/E today.

While that is not exactly cheap, we are in the early days of the company, with revenue and earnings growth expected to ramp after 2024 as the adoption of SuperVision grows.

My 1-year price target for Mobileye is $50.40, implying a 42% upside from here.

The 1-year price target is based on 60x 2024 P/E.

I think that these P/E multiple assumptions are reasonable given Mobileye clearly has a distinct technological and data advantage in its vision perception software that will enable a long-term competitive advantage.

Risks

In-house development by automotive OEMs

I have mentioned earlier that one of the key competitors for Mobileye is the in-house development of ADAS and AV capabilities by automotive OEMs. This will allow them to have more control over the software stack and reduce reliance on suppliers. However, for Mobileye, the more automotive OEMs decide to go in-house, the more revenue opportunities for Mobileye will be limited.

Progress and development toward higher autonomy

We cannot take for granted that we will gradually move from ADAS to AV. It will require more regulations and approvals while the technology continues to improve. If the progress towards AV is slower than expected, this means more limited revenue opportunities for Mobileye, especially in its consumer AV and MAAS businesses.

Conclusion

Mobileye represents an opportunity to invest not just a leader in ADAS and AV, but one that is ahead of its competition and highly differentiates itself.

I think that the company has developed significantly since the founding in 1999, as the company continued to execute towards the long-term goal of leadership in ADAS and AV.

The company's focus on ensuring its technology is scalable, low cost, and efficient is key to ensuring that automakers around the world are interested in adopting its technology.

As a result, Mobileye today has an impressive track record of having worked with more than 50 automakers worldwide.

On top of that, the company is currently already profitable and poised to grow rapidly in 2024 and beyond as SuperVision gains traction.

I went into great detail in elaborating about Mobileye's differentiation in its products, but I think its low cost and scalable platform is a key consideration for automakers, while its unrivalled intelligent REM crowdsourcing map and innovation in its perception software continues to put Mobileye ahead of peers.

I do think that the industry has a high barrier of entry and not many other companies can get to the success that Mobileye has gotten to over the past two decades.

My 1-year price target for Mobileye is $50.40, implying a 42% upside from current levels.

Comments