The Federal Reserve's September FOMC meeting took a wait-and-see approach with no interest rate hike. However, the dot plot and Chairman Powell's remarks appeared more hawkish, indicating a reduction in the expected number of rate cuts next year and a significant upward revision in economic data forecasts.

The market experienced severe volatility, with the 10-year U.S. Treasury yield surging beyond 4.4% $iShares 20+ Year Treasury Bond ETF(TLT)$, and $NASDAQ(.IXIC)$ both dropped by 1.5%, while the $USD Index(USDindex.FOREX)$ broke through 105.6.

Skipping September, why did most committee members support another rate hike?

It's because the market had already speculated closely. While there was no rate hike in September, there is a possibility of another rate hike in Q4 of this year. According to the dot plot, 12 members believe that an additional rate hike is needed in the fourth quarter, while 7 members lean towards no further hikes. Thus, the market has already priced this in to some extent.

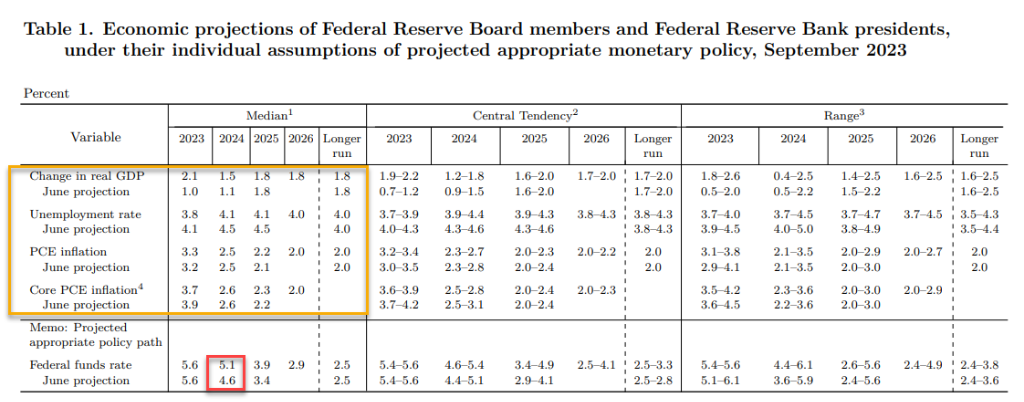

This also underscores that the Federal Reserve's dot plot is merely a reference, and there can be significant changes within a single quarter. We believe what's more important is the possibility of this high-interest rate environment lasting longer, primarily due to the upward adjustment in economic expectations. The year-end 2024 interest rate projection has been raised from 4.6% to 5.1%.

In terms of economic forecasts, the Federal Reserve has significantly raised its predictions for this year's GDP growth.

Q4 GDP year-over-year growth has been revised from the June projection of 1.0% to 2.1%, doubling the previous estimate.

Year-end PCE inflation is now projected at 3.3%, up from 3.2%, while core PCE inflation is slightly down to 3.7% from 3.9%.

The forecast for Q4 2024 GDP year-over-year growth stands at 1.5% (previously 1.1%), and core PCE inflation is expected to remain unchanged at 2.6%.

These adjustments confirm the earlier expectation of an economic "soft landing."

Why does the prospect of higher and longer interest rates unsettle the market?

The higher and longer-lasting interest rates or the rise in the real neutral interest rate may indicate that Powell also stated at the press conference that the level of the real neutral interest rate in the coming years may be higher than previously expected.

This suggests that the Federal Reserve may not be willing to tolerate a higher degree of inflation.

The Federal Reserve is assuming an increase in real interest rates, one of which is stronger economic performance and upward potential in domestic investment demand. Since the "America First" policy during the Trump administration, the Biden government has also been promoting manufacturing investment, especially in high-end manufacturing sectors such as semiconductors, chips, and new energy, focusing on domestic production and intensifying decoupling from China.

The United States is a consumer-driven economy, and the impact of inflation on real economic strength may persist for a longer period.

In addition, real estate developers may also increase new home construction to meet the demand of American residents for affordable housing.

If interest rates in the United States are higher and last longer, or become the new normal, it means that the "low-interest-rate foundation" of the bull market for more than a decade will change, and investors should not cling to the past era of low interest rates.

If high-interest-rate times persist for longer, has the market fully priced it in?

In terms of U.S. Treasury bonds, the 10-year U.S. Treasury bond has already broken through 4.4%, factoring in the potential for further interest rate hikes in Q4. Even if there are further hikes, the upward momentum is not expected to be significant.

In terms of U.S. stocks, under the premise of a return of capital to the U.S. dollar, liquidity remains relatively ample. However, performance may be disrupted by the impact on different industries, and the slowdown in profitability in some industries may be supported by others.

Therefore, there may be some pressure on valuation levels, but after a certain point of correction, attractiveness may reemerge.

Comments

Things really didn’t move that much vs say Vix only 15 vs August 15,16 was up 18 or in March did 28 spike and TSLA nflx dived late aapl others held. So idk bout trends , govt shutdown will spike bonds but jmho it’ll have to be earnings from 3rd quarter missing, revenue dropping and catalyst to get big legs. Tomorrow, Friday will tell us lot as this was low volume. They’re gonna spin this Fed today in media as good.

I don’t think there is gonna be a humungo sell off in the morning like all the bears are counting on. Maybe at first but I think it will be short lived

Interest rates have reached what we call the 'Bang Point'........PT Barnarke's QE Ponz scheme going up in smoke....LOL.

The FED is blowing in the wind ! Totally not in control !

Today was only random noise ! Up, Up and Away ! The trend is UP !