Summary

- Occidental Petroleum Corporation stock is trading sideways to down despite high oil prices and tepid analyst ratings.

- The company has been working to repair its balance sheet and has raised its dividend and implemented a share repurchase plan.

- Occidental's investment in carbon capture technology and potential revenue from carbon credits could be a catalyst for the company.

- We think Occidental Petroleum Corporation stock is a Hold above $60, but would add to our position in the middle $50s.

Petmal

Introduction

It's no secret. Shale companies are on a plateau, trading sideways to down from recent highs right now. Even with the price of WTI touching highs not seen in almost a year, many of the shale names are acting toppy. Our subject this week is Occidental Petroleum Corporation (NYSE:OXY), a long-time holding for the portfolio, and the subject of frequent past coverage. That said, it's been a year and it's time to look at the company again.

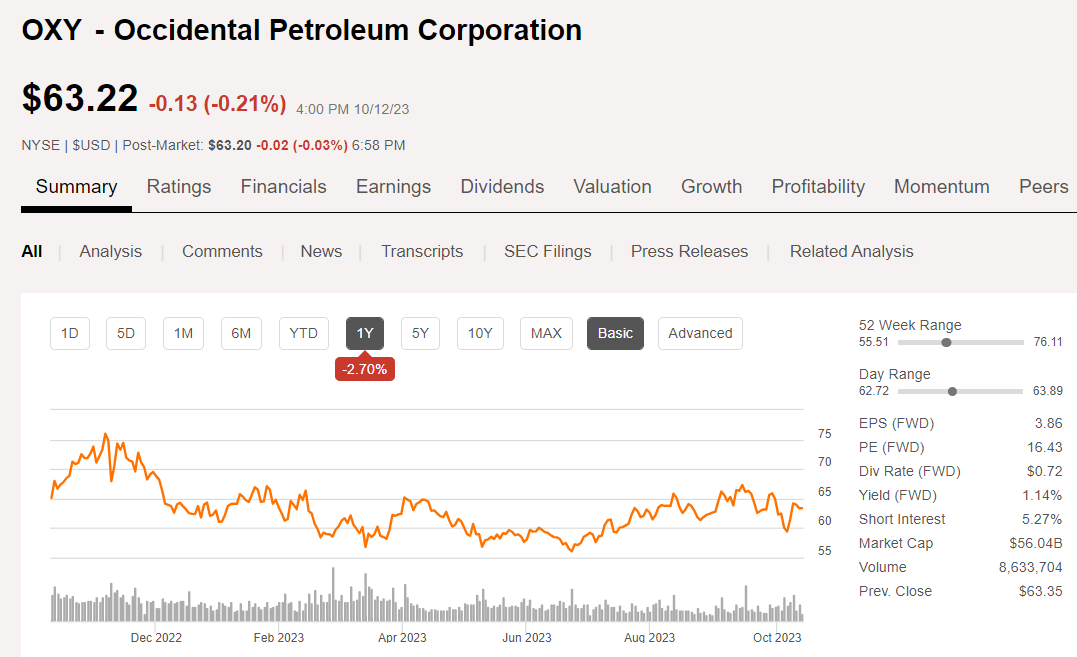

OXY price chart (Seeking Alpha)

Normal trading in OXY stock is 7-8 mm shares daily but on the 15th, 23 mm traded to the downside. That coincided with a sharp drop in WTI (CL1:COM) that day, from $91-89, so perhaps that accounts for the ever-fidgety seagulls taking flight all at once.

The lads and lassies in the analyst cadre, have become a bit tepid on the stock, rating it as Overweight with price targets ranging from $59 to $85. The median is $68, suggesting these good folks have their finger on the sell button. OXY missed on the bottom line, by a nickel for Q-2, and estimates having been coming down for Q-3-$0.75, and $1.09 for Q-4. Improvement, but only modestly so. Things are shaping up for a much better 2024 on the oil side of the equation, and significantly better on the gassy side.

In this article, we will do a top-line review of the company in advance of the earnings release coming on November 7th, after the close of business.

The thesis for OXY these days

In September, the stock poked its head above resistance at $64 and went all the way to $67, filling our heads with fantasies that it might be back on its way toward the middle $70s. Alas, that was not to be, as in the last few days it's formed what looks like a descending triangle on a technical basis. The next stop on this train could be in the middle $50s. Even the little bit of "War Premium" it gained following the outbreak of hostilities in the Middle East is fading. When you add in the large build inventories this week, a case for somewhat lower prices is easily made for the near term.

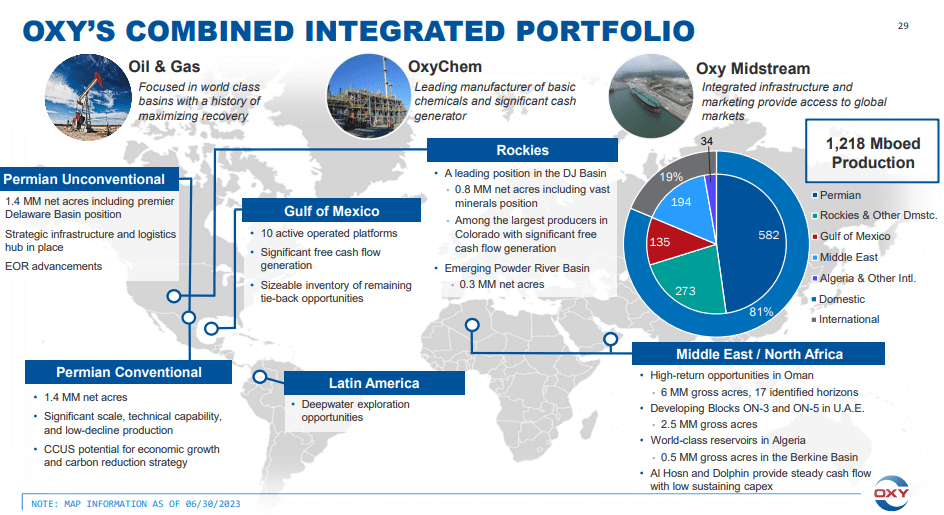

The company is a major producer of oil and gas globally with global production of 1.222 MMBOEPD, total U.S. production of 990K BOEPD, and Permian production of 568-588K BOEPD. The company also has lucrative chemicals - mainly caustic soda, a reactant used in intermediate chemical reactions to modify pH primarily. A Midstream business that facilitates its Permian EOR oil and carbon capture businesses. And, a nascent Direct Air Capture-DAC, carbon capture business operated by a long-time partner and new acquisition - Carbon Engineering.

4-years ago the company made a transformative acquisition of Anadarko Petroleum that resulted in gaining some core acreage in the Delaware basin, and substantial U.S. GoM infrastructure. I hailed this purchase at the time, recognizing the hidden value in the deepest part of the Delaware basin, in terms of well productivity. Over time, the perception of this purchase has fluctuated, with some calling OXY a poor allocator of capital. Hmm. We'll see about that.

The oil business has always been a "Go for broke, raid the kids' college fund, put up the house title, and the pink slip to the pickup," type of enterprise. Not so much in recent years, but the spirit of the Wildcatter lives on even if the flame flickers a bit in the ivory tower reaches of the Corporate Boardroom. In the spirit of Jett Rink, Vicki Hollub flew to Omaha and convinced the "Oracle" to fund her "swing for the fences" deal for Anadarko. The next day, the petroleum powerhouse was snatched off competitor Mike Wirth's table. Oil and gas from the Permian now provide about half of OXY's revenue, so the OXY purchase of Anadarko is standing the test of time in my book.

OXY Portfolio (OXY filings)

Every silver cloud has a dark lining, and the debt required to complete this purchase, including $10 bn from Warren Buffett, and the resulting issuance of a Preferred class of shares with an 8% annual coupon, nearly killed the company. Shares plummeted from the mid-$70s to as low as $9.46 in Oct of 2020. That was when I bought my initial position and have made several buys along the way.

We all know higher oil prices and some adroit debt management saved the day-for OXY and a host of other E&Ps. In the intervening time, OXY has used the cash flow to repair its balance sheet with debt now at $19 bn as a result of asset sales and cash payments, and a DE ratio of 0.68, down from nearly 2X a couple of years ago. OXY CFO Rob Peterson noted the success of the past couple of years in this regard:

Sustained efforts to significantly deleverage over the past several years have improved our credit profile, culminating a return to investment-grade status when the Fitch ratings upgraded OXY in May.

OXY's rich Uncle Warren has increased his stake in the company, adding the luster of his storied name to the company. Even as OXY has redeemed 12% of the punishing preferreds Warren took as collateral for his $10 bn, and saving ~$100 mm in annual interest payments. Every little bit helps.

OXY's efforts toward repairing the balance sheet have gotten to the point the company has been able to raise the dividend-still a shadow of its former glory, to $0.72 per share. As we head into the next couple of quarters it wouldn't surprise me to see a few more incremental bumps along this line. This should be significantly enhanced by the company's $3 bn share repurchase plan. At current prices, this commitment could take the share count down another 30-40 mm shares, from what is already a five-year low of 889 mm. As before, it all adds up over time.

A potential catalyst for OXY

Carbon credits are all the rage these days. The CDR credits for DAC are just the latest step in the industry cozying up to the government for fun and profit. There is nothing like money from the government, as they have a boundless supply of it, and as has been aptly demonstrated in recent years, if they need more it's easily "printed." I am going to give a brief description of this program and the choice of laughing at its absurdity or crying at the futility of it all, is yours. It's ok to do both.

All right, companies that remove carbon from the environment using DAC technology earn credits - Carbon Dioxide Removal - CDR - credits from the government under 45Q. These CDR credits are fungible and can be sold to third parties. (Are you still with me?) Recently, through their 1.5 subsidiary, OXY has been growing a list of clients for their $1 bn 500,000 met ton annually DAC plant, now named Stratos. Amazon has just inked a deal to buy 250,000 CDR credits over ten years, joining a growing list of companies signing up to "decarbonize." Vicki Hollub, CEO of OXY, comments in regard to Low Carbon Ventures:

We were glad to announce that Japan's ANA Airlines became the first airline in the world to sign a carbon dioxide removal credit purchase agreement from our subsidiary, 1.5. We're excited about that and happy to work with them. We're also pleased to announce a first-of-its-kind agreement with our long-standing partners, ADNOC, to evaluate investment opportunities in director capture and carbon dioxide sequestration hubs in the U.S. and the UAE. With this agreement, we intend to develop a carbon management platform that will accelerate our shared net zero goals. We have many exciting developments taking place in LCV, and we look forward to providing you a more comprehensive update towards the end of this year.

In the case of Amazon, it has been stipulated that the CO2 credits they buy will go into non-oil-bearing fields for sequestration, as noted below.

Under the agreement with Amazon, the captured CO2 underlying the CDR credits will be stored in saline reservoirs that are not associated with oil and gas production.

The Inflation Reduction Act includes tax credits that range from $50-180 per met ton, so one can expect the retail value of a CDR is substantially more as this article in Carbon Future magazine notes.

Tax credits for DAC projects with permanent storage will increase from $50 to $180 per metric ton, making a major dent in the cost of DAC-based carbon removal, which now runs from $200 to $500 per metric ton.

In summary, with a plant that can theoretically remove 500,000 met tons of CO2 per year, OXY has the makings of a cash cow coming on line in 2025, and when fully subscribed. Simple math suggests a revenue potential of $175-200 mm per year using $350 per met ton. With a billion dollar investment there is a rough parity with a new build cost on a deepwater drillship, now fetching $450-500K per day. If OXY hits that $200 mm target, that's $547K per day, which suggests an acceptable return on investment. 1.5 talks of as many as 100 of these plants being built, and it wouldn't surprise us to see them all built out one. Uncle Sam is picking up a big part of ticket...so anything goes. It's only money, right? OXY shareholders stand to gain substantially as this gathers momentum.

That's how you do it in 45Q Funkytown.

OXY is bucking the trend in drilling performance

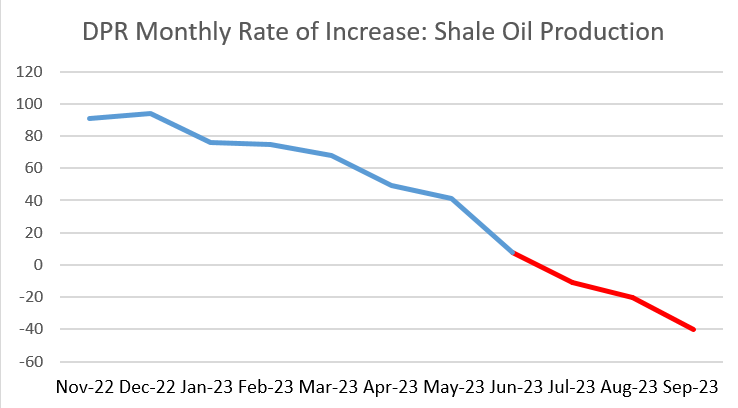

The recent EIA DPR confirmed something we have been discussing for at least a year. Shale production is leveling off, and if the last three reports are any guide, could be entering a decline. One that's not explained by vagaries of the weather as in the Snow-maggedon of Feb-22, or a financial crisis. That's the macro picture.

EIA-DPR (EIA)

On an individual basis, shale daily output per rig has been on a long decline slope, until recently. This bit of data is pretty noisy and not amenable to much interpretation. The curve higher while total output has declined, as shown in the graph above, is interesting. Just throwing out a SWAG, I'd say this might be reflective of longer laterals and higher completion intensity.

EIA-DPR (EIA)

This is where the "rubber" meets the road in terms of technology. You will recall we discussed how AI advances are changing the game in shale strategies. (If you are new and haven't read this article, you really should.)

OXY well productivity (OXY)

The gap between 2015-2023 is an astounding 275,000 barrels at the 150-day point. This is like having 4:1 in 2015, for considerably less drilling cost than it took to drill one well in 2015. Vicki Hollub comments on ramping efficiencies and the role they are playing in keeping costs down:

The DJ team's diligent work set several new Oxy records, including company-wide record of drilling over 10,400 feet of lateral in only 24 hours. Just 10 years ago, it took the industry an average of 15 days to drill 10,400 feet. Our Delaware completions team shattered OXY's previous record for continuous frac pumping time by nearly 12 hours for a total of 40 hours and 49 minutes. Four years ago, the same job would have taken about 84 hours. 40 hours back then was unthinkable.

In the Q2 call, the role modeling was playing in re-evaluations of lower tier benches to top tier benches was specifically mentioned. Vicki Hollub, who it should be noted is a petroleum/chemical engineer with decades of drilling experience, comments on the role modeling is playing in enhancing production:

In the Permian, we have improved well productivity in 7 of the last 8 years, with the application of our proprietary subsurface modeling. Improved well designs have resulted in about 25% improvement in single well 12-month cumulative volumes over the last five years. And we are on pace to significantly exceed that rate in 2023. Our teams are continuing to advance our modeling expertise, which has led to upgrades of secondary benches to top-tier performers. Last year, because of these upgrades to our secondary benches to our top-tier benches, we were actually able to replace our production by 212% with reserve adds. Secondary bench upgrades are progressing in 2023. Overall, in 10 of the last 12 years, we have replaced 150 to 230% of our annual production.

This is an unexpected dramatic turn of events. Upgrading benches? How is that possible? The answer is the role the big data sets that now exist play in giving operators much more detailed information about their reservoirs that enable these tier upgrades.

Risks to our thesis

Oil and gas prices have improved materially since late August. They are well off their mid-September peaks, however, and may see further degradation due to inventory builds. There is a reasonable probability these will continue as we are headed into refinery turnaround season which will dampen the thirst for crude.

Balanced against that are the proactive steps OPEC+ has taken in the past few months to support oil prices. In early October, these cuts were extended to the end of the year. They could also be extended into 2024, as reported in an OilPrice article. With a lever like that adjusting production to keep it at a slight deficit to demand, we should avoid another collapse into the $60s.

Your takeaway

Occidental Petroleum Corporation is trading now at an EV/EBITDA of 5X and a price to flowing barrels of $60K per barrel. For a company with the acreage and other revenue streams they have, these values don't seem excessive under the market conditions we have now. With their cash flow sensitivity of $225 mm per $1.00 increase in WTI/Brent the rally from $70-90, translates to ~$4.5 bn on an annual basis, and taking this metric back toward Q-2, 2022 levels of ~$20 bn.

Assuming WTI prices average more than $80, the EV/EBITDA ratio would drop to 3.75X. To keep things the same, the stock should rerate to about $80 per share. That has me thinking most of the seagulls are a bit too flighty and we ought to stick around for a while.

Accordingly, I am calling for a hold at current levels, but just like Warren, if the share price were to drop into the $50s, it would be time to add.

Comments