Summary

- The new Shell plc CEO, Wael Sawan, has taken a more realistic approach to the energy transition, acknowledging the ongoing need for oil and gas.

- Shell's focus on gas and deepwater markets, as well as its low breakeven costs, position the company well for future success.

- Shell's presence in EV charging and potential offshore reserves in Namibia could serve as catalysts for growth.

- Shell stock is a buy at current levels.

alexei_tm/iStock via Getty Images

Introduction

One of the first articles I authored in Seeking Alpha was on Shell plc (NYSE:SHEL, OTCPK:RYDAF). It was a natural for me to cover the company, as I had worked closely with them for many years. To say I was a fan is an understatement. Then our relationship began to cool off as Shell began to move more toward renewables and away from the business it really understood: producing oil and gas.

Shell price chart (Seeking Alpha)

Senior Shell management began to utter blather like this in conference calls. If you can follow this unintelligible gobbledygook, you're a step ahead of me.

And this means working with our customers address the emissions that are produced when they use the energy products that buy from Shell. That effort includes working with broad coalitions of businesses with government and other parties on sector by sector basis to identify and enable the carbonization power plays for each sector of the economy. That's how we intend to achieve our ambition in net zero emissions energy business at 2050 or sooner.

Then-CEO Ben van Beurden just said they were going to sell less oil and gas, (Ok, so I followed it.). This was the one thing they were really good at, with a skill and finesse developed over 100 years of experience. Shell and I were in business together. I had given them some capital, their job was to give me a regular return on it. When you find out a partner isn't who you thought they were, that your capital might be diminished, you change partners. I sold out of Shell the next day.

Shell has new leadership now. Wael Sawan, who took over as Shell CEO in Q4 of last year, significantly moderated the tone of the company in his first outing, and was recently quoted espousing a realistic view of the energy path forward-

"The reality is, the energy system of today continues to desperately need oil and gas," Sawan said. "And before we are able to let go of that, we need to make sure that we have developed the energy systems of the future - and we are not yet, collectively, moving at the pace (required for) that to happen."

That is an encouraging standpoint that embraces the company's core strengths, and as a potential investor compels a new appraisal of the company. I can work with that.

The thesis for Shell today

Shell's pivot back to a rational, more balanced approach to energy delivery is encouraging. It reminds me of what a powerhouse company it is in the gas and deepwater markets. Shell is the biggest producer and explorer in the GoM, and has made one of the most significant recent discoveries offshore Namibia. It also revalidates a huge decision that Shell (under Ben Van Beurden) made years ago to buy British Gas for ~$70 bn. That added ~$20 bn in cash to debt, and about 1.8 bn shares to their float. (Shell Float: 2015-6.4 bn shares, 2016-8.2 bn shares).

Much of the financial impact of the BG buy is still carried on the balance sheet, but on the good side of things, so are the gas reserves that came along with it. Shell is heavily leveraged to LNG with its LNG Canada liquefaction plant in Kitimat, Canada, and the Prelude FLNG project in Australia.

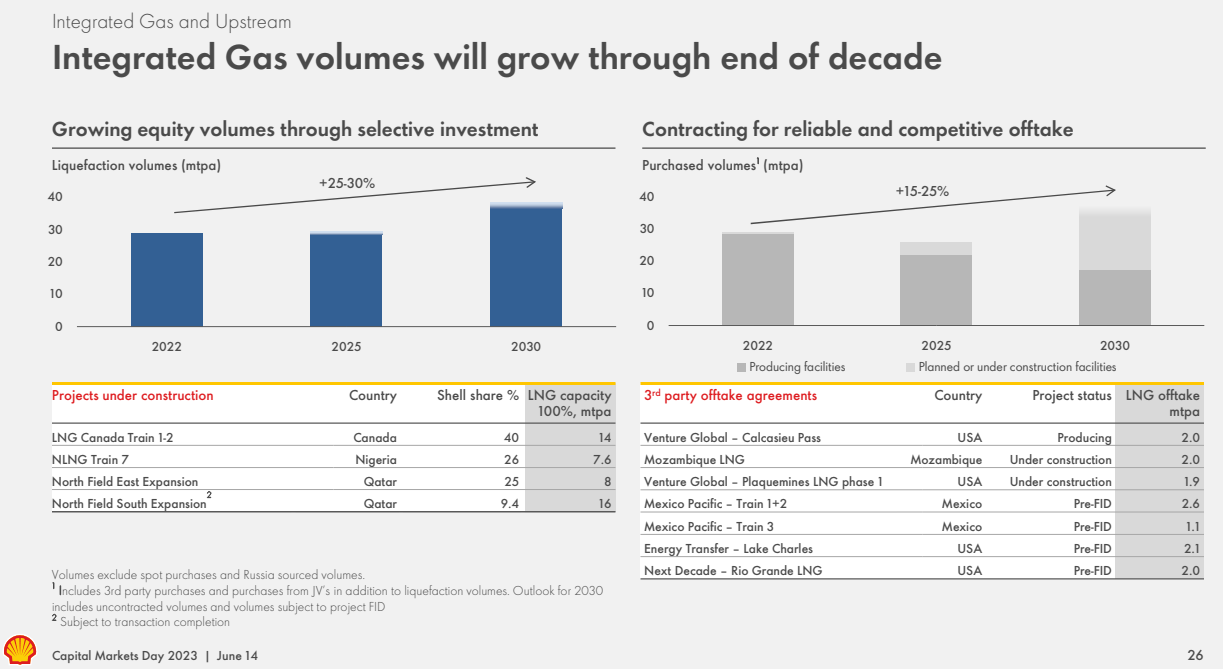

Shell Integrated Gas (Shell)

All but the most Lenin-esque climate radicals will grant there is a long-term role for gas in the "Energy Transition." More moderate voices, even our current leadership, sees the need for gas as a "bridge" fuel. The future of LNG is underpinned by this reality, and as the hollow promise of most renewables - solar and wind in particular - begins to wreak havoc with the energy grid, gas should remain in high demand for base load capacity. LNG is here to stay, and that bodes well for Shell.

Hey buddy, got any Short Cycle barrels?

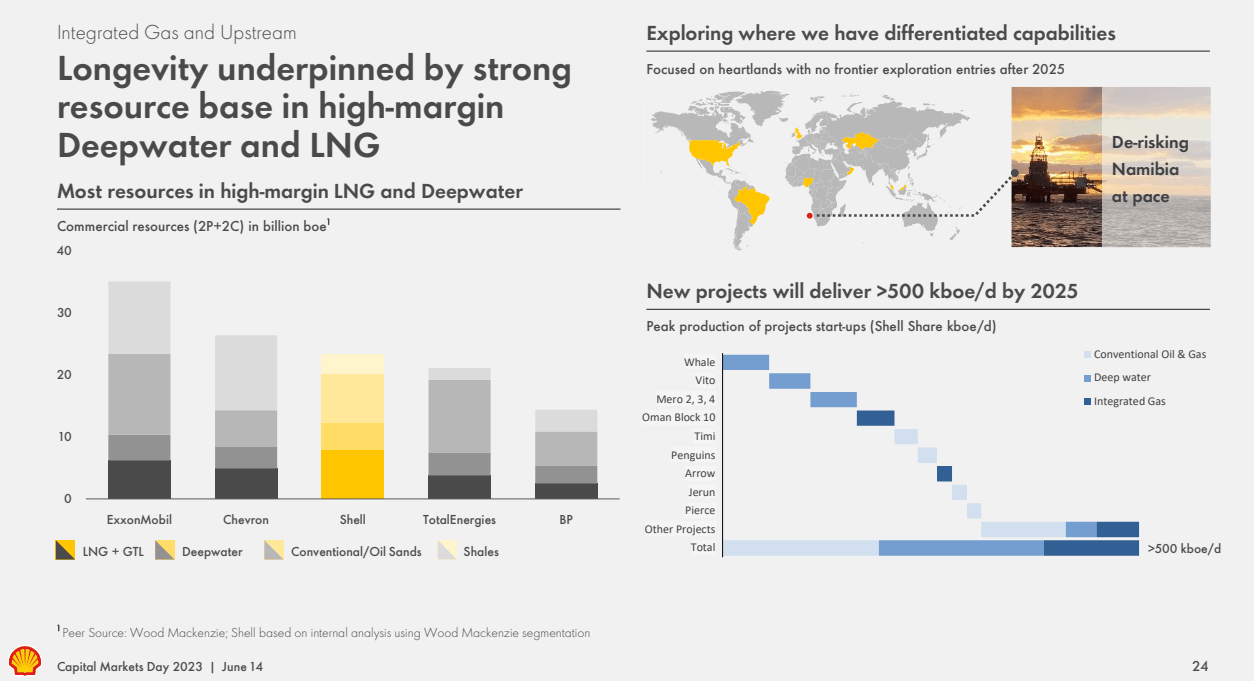

One negative you can note in the slide below for Shell is their lack of quick-turnaround shale reserves, as the Van Beurden regime in a fit of Climate Shaming-induced madness from the Dutch court decision sold their Delaware acreage to ConocoPhillips (COP) for $9.5 bn. The company has a massive $45 bn cash balance that should be burning a hole in their pockets.

Shell Integrated Gas (Shell)

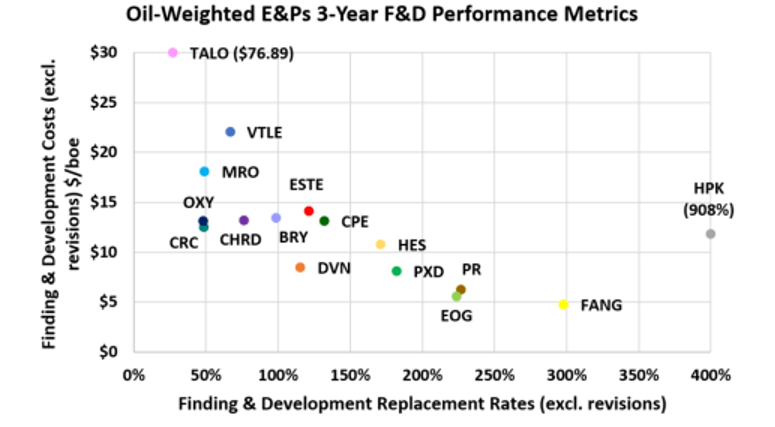

This pivot is timely. Shell's oil and gas production was 12 and 15% lower respectively in 2022, vs 2021. That is not a favorable trend and moves their capital cost to produce oil and gas about $3.00 per BOE higher in '22 vs. '21 using BOE production and Capex expenditures for those years. Whatever other metric you use EV/EBITDA-which is a function of prices, or flowing barrel valuation-again, a function of prices, Shell's unit cost is rising and that's a bad thing in a commodity business. It shows up in their Cost of Revenues as well. For Q2 2023, this ran 77%, for Q1 2023 it ran 74%, for Q4 2022 it was 71%. This is a snapshot of a small sampling that can be impacted by a lot of things, but it's also impacted by capital costs and they are going up. Things need to turn around. And, with $45 bn they could make a tasty bite out of one of the E&P's on the RBN Energy graph below.

Oil-weighted E&Ps (RBN Energy)

Hess (HES), Devon Energy (DVN), and Diamondback Energy (FANG) are performing at a higher level than Shell, and could be bought with Shell's cash hoard. Not that Shell necessarily would plunk down all that cash - although I think we can agree, they should be doing something with it. They could follow the Exxon Mobil (XOM) route and just print stock for most of it. One way or another, Shell needs short cycle barrels.

Food for thought anyway.

Deepwater

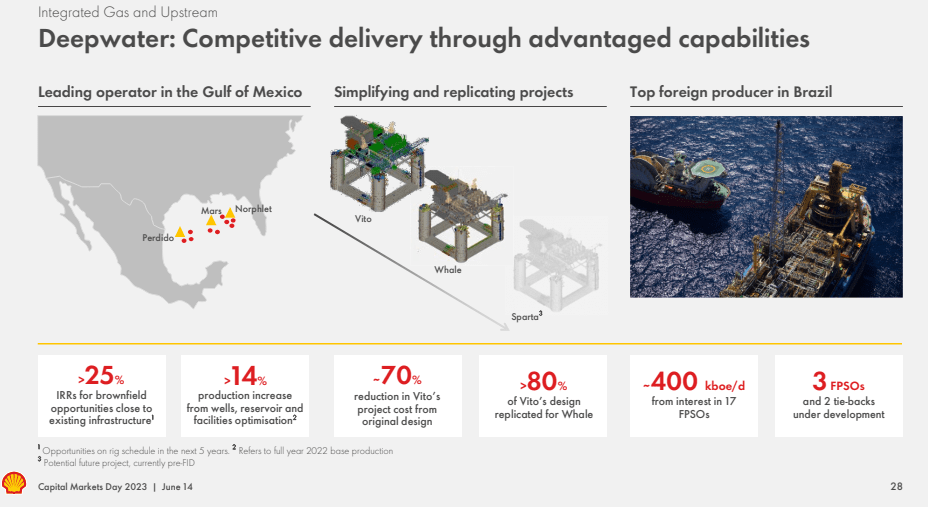

Shell's focus will be in areas where they have "advantaged capabilities," meaning installed infrastructure to leverage new production. Shell notes they have very low breakeven costs in the range of $30 per barrel for these projects, which put them firmly in the black even under bearish price scenarios. GoM crude is in high demand by refiners on the U.S. Gulf Coast, due to its mid-30's gravity. Shell is also a big operator and retailer in Brazil. (I used to buy my gas at Posto Shell on Avenida das Americas in Barra de Tijuca, just south of Rio.)

Shell Deepwater (Shell)

Shell is also able to take the host designed for Vito and replicate it for similar deep water projects, each project learning from the last. Should Sparta (formerly TotalEnergies' (TTE) North Platte) get FID'd, the upfront engineering cost will be lessened.

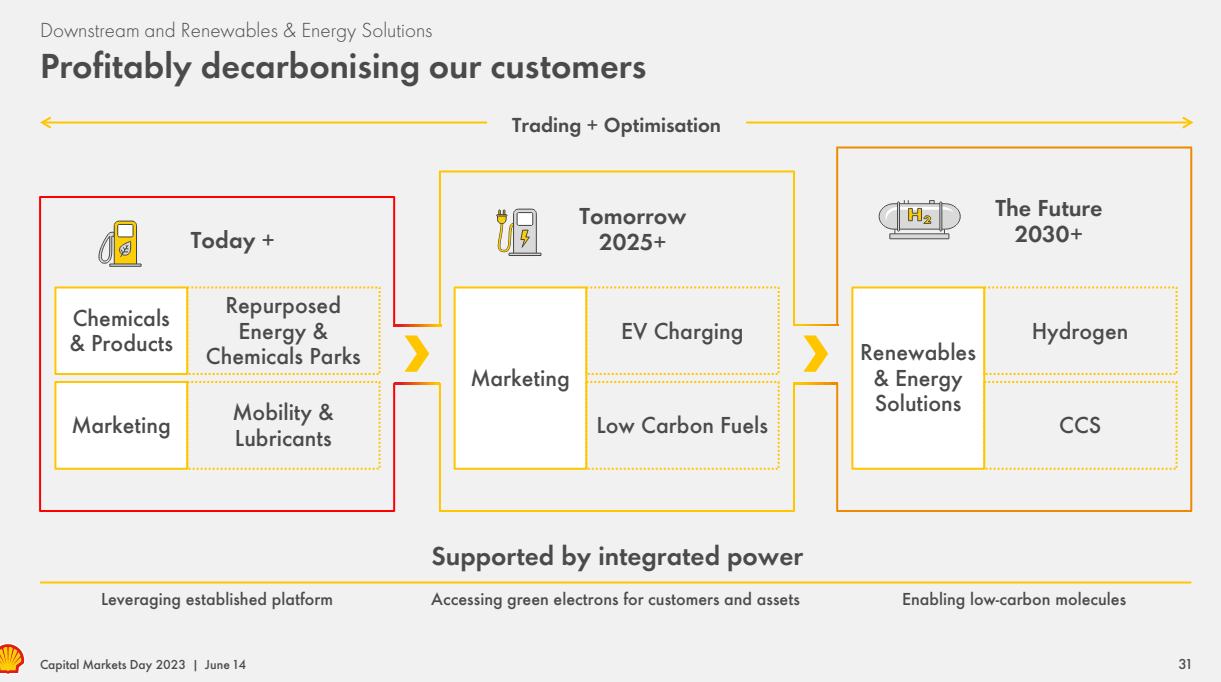

Renewables and Electric mobility

With its footprint in convenience/fueling stations across North America, South America, Asia, and Europe, Shell is in a premium spot to leverage electric vehicle ("EV") charging as it grows in importance. Shell projects $1.5 bn in EBTIDA from this source by 2030. There is no question EV charging will become a major revenue generator in the near future, and I think Shell is doing the right thing to gear up for it.

Shell EV Charging (Shell)

Other renewable pathways for Shell on the way to 2030. Most of this is too nascent to discuss here, but provides a look into the company's thinking.

Shell Decarbonizing (Shell)

A potential catalyst

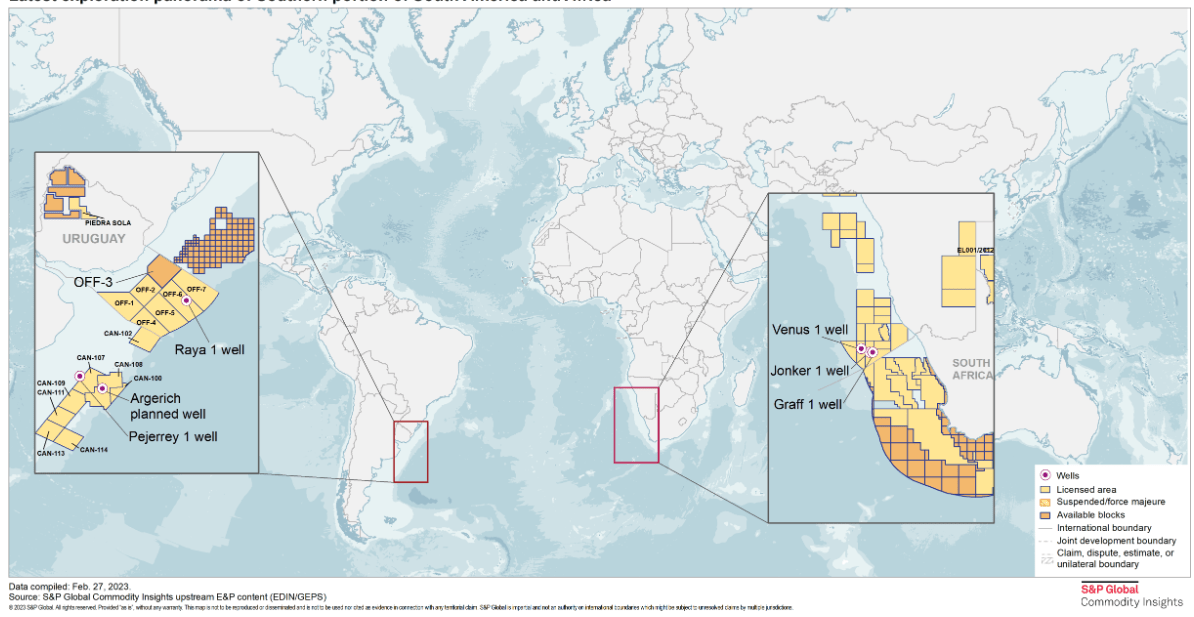

No one is coming out and saying it right now, but Namibia's offshore reserves, now estimated at 11 bn BOIP, could set the stage for this country to become the next Guyana. As this hydrocarbon map put out by the National Oil Company of Namibia, aka NAMCOR, shows, dozens of companies are participating in this emerging boom. It's no secret any longer that drilling on either side of the Atlantic Margin is guiding exploratory drilling on either side, and causing geologists to reassess what they think they know about it. The slide below shows the Atlantic Margin relationships between the Latin American side and the West African side.

NAMCOR Hydrocarbon map (S&P Global)

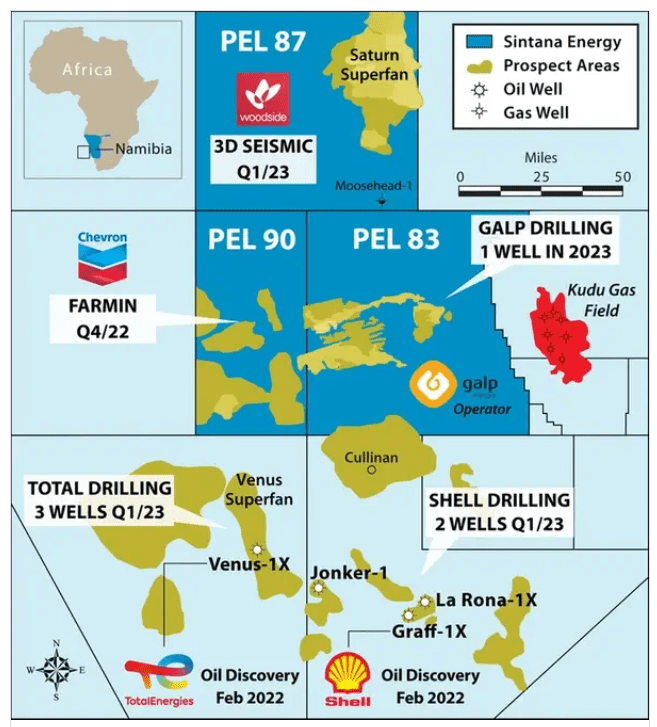

Shell has completed its fourth exploratory well with a successful show of hydrocarbons, and has 10 more delineation wells permitted.

Namibia acreage map (S&P Global)

Could Namibia become a million barrel a day producer for Shell, the way Guyana has for Exxon Mobil? The companies are pretty tight-lipped as of now, but the early results are interesting.

Risks

Shell is big enough that it is a frequent target for the Climatocultists. The Dutch court decision made that clear. Shell has redomiciled to the UK, but there is no shortage of Green anti-fossil fuel crusaders in ol' Blighty. Adverse legislative impacts cannot be ruled out.

Shell has rallied from the mid-$40's a year ago, staying mostly in the upper-$50's to low $60's during that time. Currently the company is near the upper end of its recent range.

If Shell were to make a big acquisition using stock, current holders, would be diluted. In the case of XOM, shareholders are taking a 15% hit.

Your takeaway

I think Shell plc stock is investable with the current management's commitment to rational hydrocarbon development. Oil and gas still pay the bills around Shell and it's nice to hear some recognition of that as a prospective shareholder. As previously noted, new CEO Wael Sawan has modified the corporate rhetoric and shown himself willing to stand up to the fringe elements demanding sharp cuts in petroleum output. I am letting Shell out of the DDR dog house.

Analysts rank Shell as a Buy, with a price target range of $60-88.00 per share. The median is $75, suggesting that most of the seagulls view the company as having some tailwinds in a higher oil price scenario. On an EV/EBITDA basis the company is stunningly cheap at 2.47X, but fairly pricey at $108K per BOE. As noted, Shell has an incredible $45 bn in cash on its balance sheet, and if I was a shale CEO at Devon, EOG (EOG), or Diamondback on down, I would be feeling the hot breath of Wael Sawan on my neck.

For reference, key competitor BP (BP) trades at 2.36X and $106K per BOE, suggesting it too needs to up daily output. Shell's Free Cash Flow yield is 16%, sweetening the deal still further.

The analyst cadre is calling for $1.86 per share in Q3, with would put Net Income in the $15 bn range and imply EBITDA in the neighborhood of $35 bn. Put a one-year run rate on that and Shell's multiple drops to 1.5X. To keep the multiple at 2.46 the shares will have to rerate toward $85 each, implying significant upside. It's understood this is all contingent on Brent staying above the $80 level (CL1:COM).

Shell announced a $3 bn share buyback in conjunction with its earnings release. That's about 50 mm shares, so not a real dent in their current float. It also raised the dividend to $2.31 a share and will likely continue this practice with the cash flows it's experiencing now.

All of that said, if we get any significant pullback in Shell plc stock, it should definitely be viewed as a buying opportunity. I would probably set my entry point around $60, and encourage investors with modest risk tolerance looking for growth and increasing income to consider doing the same.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Comments