Summary

- Navitas brings a strong value proposition in the power semiconductor industry with its GaN integrated circuit, which brings speed, energy savings and efficiency and lower weight and size.

- The company is gaining traction outside of its initial mobile market, diversifying its revenue into data center, solar and EV, as well as home appliances and industrial markets.

- Navitas has a strong competitive advantage as it is the only producer of GaN integrated circuits and this advantage is protected by a solid patent portfolio.

- The management team is led by four of Navitas co-founders, with the CEO and COO/CTO having strong alignment to shareholders with the equity incentive plan in place.

SweetBunFactory

Navitas Semiconductor (NASDAQ:NVTS) is one that I have been watching for some time and looking to add, and also one that many members have expressed interest in, so here's a deep dive on a company that is gaining significant traction in the semiconductor space and growing at a rapid pace.

Brief description

Navitas designs, develops and markets the next-generation power semiconductors, which includes Gallium Nitride ("GaN") power integrated circuits, Silicon Carbide ("SiC") and high-speed silicon system controls and digital isolators that are used for power conversion and charging.

Its products are used in a wide variety of applications, including fast chargers for mobile phones and laptops, in solar inverters, electric vehicles, consumer electronics and even data centers.

Navitas recently acquired GeneSiC Semiconductor, a pioneer in SiC with strong expertise in the SiC power device design and process. This acquisition helps to further expand the reach of Navitas into the solar and electric vehicle markets.

As I will explain later, Navitas products bring strong value add in terms of efficiency, performance, size, cost and sustainability over the current silicon-based technology being used today. The company's products allow for faster charging, higher power density and improved energy savings compared to silicon-based systems.

Navitas also acquired VDD Tech in 2022. VDD Tech is known to have created advanced digital isolators for next-generation power conversion. VDD Tech, creator of advanced digital-isolators for next-generation power conversion. Advanced digital isolation techniques are required to bring size, weight and cost improvements to the consumer, solar, data center and EV market. VDD Tech's proprietary technique enables stable, reliable and efficient power conversion at MHz switching speeds.

In 2023, Navitas also announced it will be acquiring the remains stake in its silicone control IC joint venture, Halo Microelectronics. This joint venture was meant to develop application specific silicon controllers that are optimized to work with Navitas GaN ICs to improve on performance for the different applications.

Introduction to the industry

Most electronic devices today require a power supply to convert the alternating current ("AC") into direct current ("DC").

These power supplies can be either located inside the devices themselves, like in the case of consumer electronics and home appliances, or outside of the devices like for mobile phones and laptop chargers.

For other applications like in electric vehicles, power is converted from a DC battery to a lower voltage, while in the case of solar inverters, the low-voltage DC is converted to AC.

For most of these devices today, the power supply functions largely use silicon-based solutions. That said, the current silicon-based solutions are inadequate today to meet the high energy efficiency and fast charging demands of today.

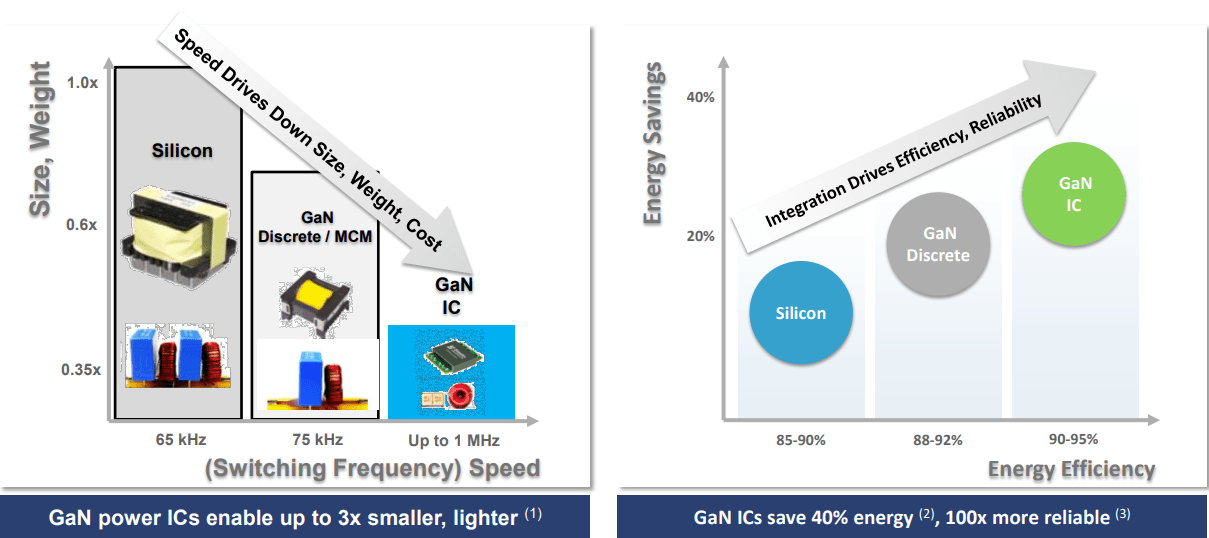

As a result, there are two materials that are newer and "wide bandgap" materials that could change the power electronics market. These are GaN and SiC. In general, SiC solutions are designed for higher power applications and higher device voltages. GaN solutions are able to improve the power system switching speeds and energy efficiency. This translates to higher density, lighter weight and lower systems costs at the end of the day. As a result, relative to the current silicon-based power solutions of today, both GaN and SiC solutions bring significant improvements.

However, there has traditionally been difficulties in pushing for the adoption of GaN as a result of the industry being unable to overcome the challenges of integrating GaN, which lead to higher costs, complexity, and vulnerability. However, Navitas is able to be the first company to integrate all the components into a single GaN chip. Its GaN chip is known to provide energy savings, lower costs, and a smaller footprint compared to other discrete GaN solutions.

The GaN device market is expected to double every year until 2026, with a 117% CAGR. As a clear leader in the space, Navitas has the opportunity to leverage on its leadership position to ride on this strong growth. Together with SiC, the total addressable market is expected to be $22 billion, with $9 billion for SiC, $7 billion for GaN and $6 billion for the overlapping GaN and SiC market. In addition, Yole forecasted that about 30% of the legacy silicon-based market will be taken over by GaN and SiC solution by 2027.

What are the advantages of GaN over traditional silicon-based solutions?

It is estimated that GaN-based solutions can bring up to 40% energy savings, up to three times higher power density, three times faster charging, and are three times smaller and lighter when compared to traditional silicon solutions.

Benefits of GaN (Navitas)

Customers and markets

Mobile

The initial focus for Navitas was the mobile market given its short design-in time. As GaN power ICs are introduced into the mobile market, it brings up to three times power and up to three times faster charging while taking up only half of the size and weight of similar silicon chargers.

In terms of the market opportunity, there are about 2.5 billion chargers shipped each year, with about $1 of GaN content each, while non-mobile applications like TVs have about $3 of GaN content per system and about 600 million systems are shipped each year. The total addressable market is thus around $4.3 billion in the mobile market.

Navitas is in production and development with all of the top 10 mobile OEMs. In 2022, Navitas developed almost 100 new GaN fast charger designs with Samsung, Oppo, Lenovo, Dell, amongst others. Since its focus on expanding to new markets and diversifying its revenue sources, the mobile business is likely to become a smaller part of revenues in 2023 and beyond.

In its 1Q23 results, Navitas stated that they have 20 new mobile chargers launched in 1Q23 which includes Xiaomi and Lenovo, and it has more than 150 projects in development today, amounting to a revenue pipeline of more than $100 million.

Solar and energy storage

Navitas currently has more than 35 customers in the solar and energy storage space either in development or production.

Management commented in the most recent quarter that they see strong traction in the solar and energy storage segment's shipments, backlog and pipeline.

The total revenue pipeline for the segment is more than $150 million and more importantly, Navitas has projects under development with most of the top 10 global players in the solar industry and there are many that are intending to ramp SiC and GaN shipments into the solar market in 2024.

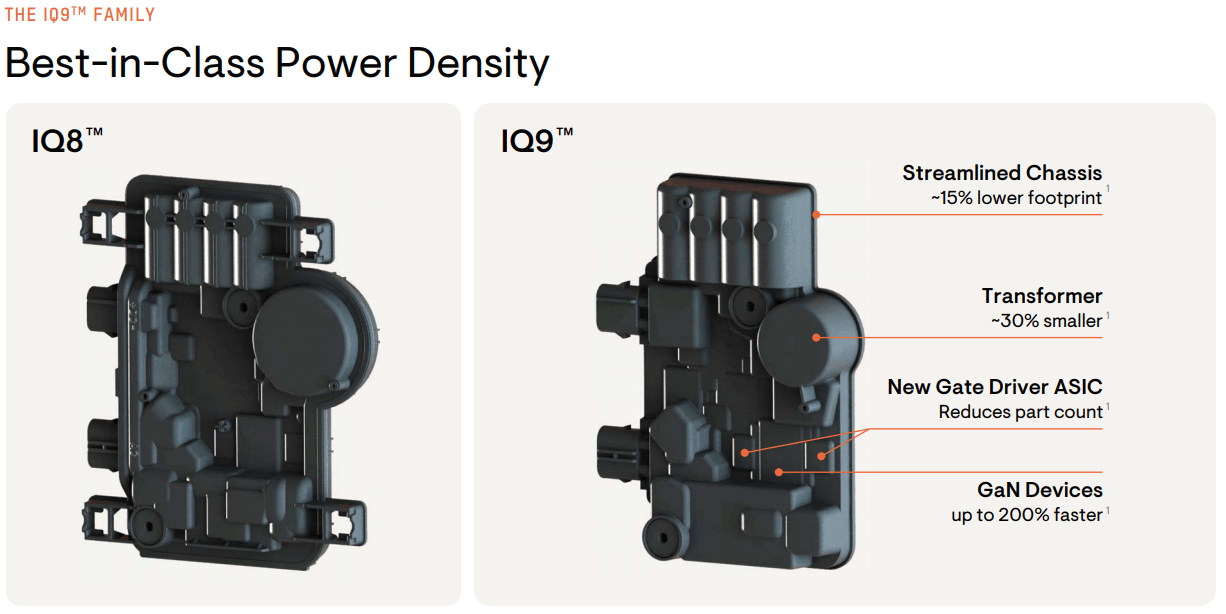

One such company is Enphase Energy (ENPH), which I also cover in my investing group, and in my deep dive article, I was pleased to hear that Enphase Energy was looking to introduce its brand new IQ9 microinverter that utilizes GaN technology. This is huge for Navitas given the large volumes Enphase Energy has in the microinverter world given its dominant market share position.

According to Enphase Energy, this is how they see GaN in the solar space:

It's the end of the road for silicon.

GaN offers more than 10x frequency, and significant cost advantages."

As can be seen below, Enphase Energy is expected to introduce GaN technology into its newest IQ9 microinverters. As Enphase Energy has highlighted, its IQ9 microinverter is expected to have 50% more power density than IQ8 microinverter, and GaN allows for high power and fast switching, resulting in two times the switching frequency of IQ8, which in turn reduces the size of the transformer by 30%.

Enphase IQ9 (Enphase Energy IR)

Apart from microinverters like Enphase Energy, Navitas stated that they have more than 20 customers in the commercial string inverter space like Sungrow, BYD, AP systems, Power Electronics, Growatt, amongst others.

Within the electric vehicle space, Navitas has a strong competitive position as a result of its SiC technology that enables ultra-fast charging with higher power density, improving efficiency and lower costs.

Navitas' SiC technology is being adopted by EV charging companies and it is currently being integrated into more than half of the roadside chargers in the United States, including major customers like Electrify America and EVgo (EVGO).

Management expects that the potential for SiC in the roadside EV charging space will grow by 30% CAGR until 2030.

Navitas is also seeing interest from global OEMs for the integration of its SiC technology into EV onboard chargers. Its major customers include BYD (OTCPK:BYDDF), General Motors (GM) and Mercedes-Benz (OTCPK:MBGAF). Navitas is also co-developing the next generation onboard chargers for Geely (OTCPK:GELYF) which will look to include a combination of SiC, GaN and digital isolators, with the first EV incorporating this expected to be in production in 2025.

Home appliance and industrial

Within the home appliance and industrial space, Navitas currently has more than 45 customers either in development or production and its revenue pipeline from the segment amounts to $150 million.

This market is largely involving domestic appliances like washing machines, compressors for refrigerators, heat pumps and industrial applications like robots, warehouse materials handling. Through the use of GaN half-bride power ICs, this brings more than 70% energy savings relative to their silicon counterparts.

The demand from the segment comes from stricter regulations on safety and sustainability that is driving upgrades from homes and industrials.

Data center

Navitas sees a strong value proposition within the data center space. GaN based data centers have efficiencies of 84%, higher than that of the 75% for silicon-based data centers. As a result, almost $1.9 billion of electricity can be saved if these data centers migrated from silicon to GaN. Navitas expects to have a $1 billion total addressable market from the data center market based on IDC and Navitas estimates.

Navitas is still in the sampling phase for its GaN ICs, which were launched only in 4Q22. The company has seen development projects with potential customers grow to 15, with a revenue pipeline of about $60 million. Navitas is developing six system designs that are expected to be on track to ramp in 2023 and 2024.

Manufacturing strategy built to their strengths

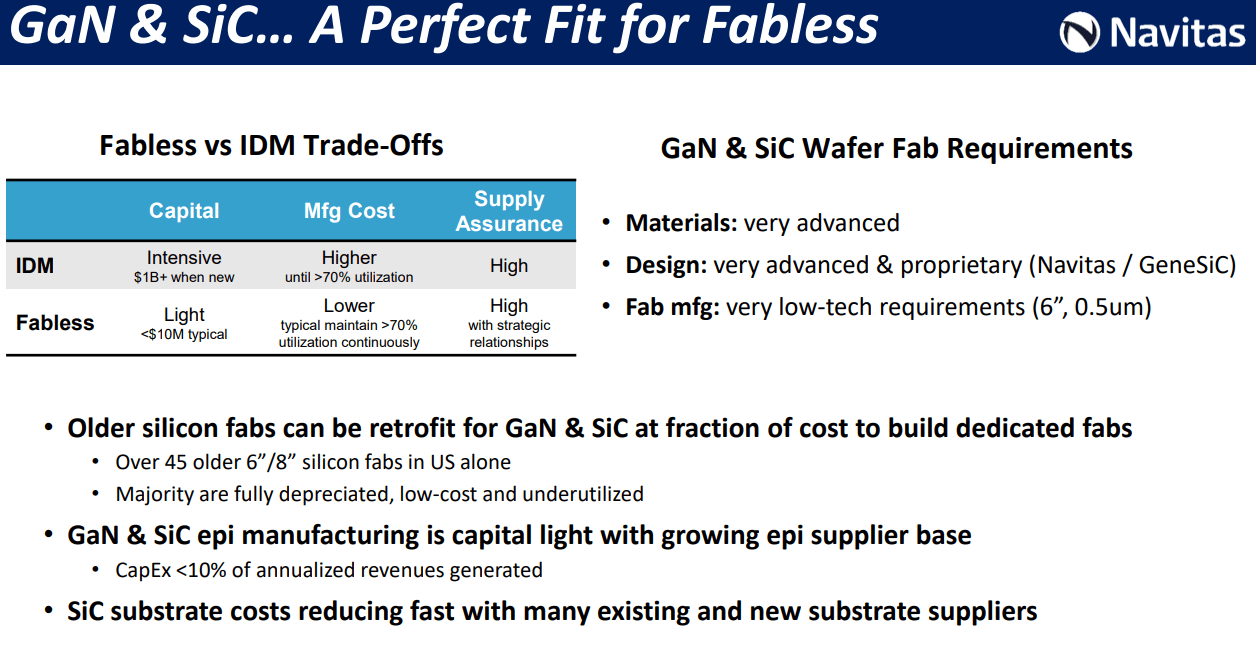

Navitas employs a fabless business model, choosing to work with third parties to manufacture, assemble and test their products.

This is because of what we can see in the picture below. While the materials and design aspect of GaN and SiC is very advanced and proprietary, the fab manufacturing is very low tech and can be easily outsourced.

As such, Navitas has Taiwan Semiconductor Manufacturing Company (TSM) as its wafer fab partner and have worked to co-develop manufacturing capabilities for GaN based products with TSMC. TSMC acts as a top global supplier for Navitas and continues to have sufficient capacity to meet the needs of Navitas.

Manufacturing strategy (Navitas IR)

Competitive advantages

Navitas has a strong competitive advantage in technology and looks to be able to maintain this leadership for some time. As of March 2023, Navitas claims that based on publicly available data, there are no other competitors that are able to produce GaN power ICs that are monolithically integrated.

As such, Navitas is the leader in GaN power ICs with its technology and intellectual property being its key competitive advantage and it seems that the barrier to entry is quite high as no other players are able to produce a similar product yet.

The first competitive advantage of Navitas, in my view, is its leading patent portfolio of more than 185 patents that are either issued or pending.

This covers all aspects of GaN power circuitry, including SiC device design, analog and digital integration and these patents can mostly be applied across markets.

One key intellectual property that Navitas highlighted was its GaN IC process design kit, which is used to speed up implementation of products and development with the end customer that no other competitors are able to replicate.

Its second competitive advantage pertains to its differentiated GaN power solutions. As a result of its integrated circuit approach to GaN, which no other competitor is able to achieve, Navitas is able to have an advantage over discrete GaN in terms of a simpler design and lower complexity of operations. The key thing for Navitas is that it is the only one that is able to overcome the main challenges involving the commercialization of GaN integrated circuits design and test systems.

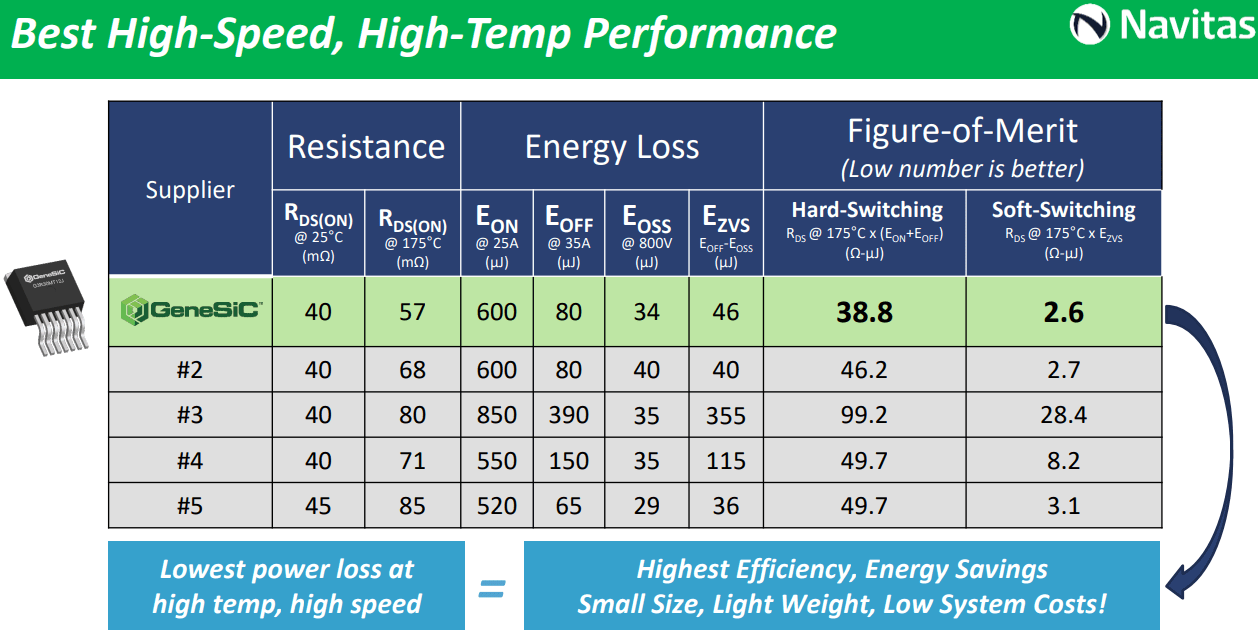

Lastly, Navitas also has a leading and proprietary SiC offering after its acquisition of GeneSiC. Skipping the technical aspects of all the technology involved, Navitas SiC solutions bring three times device life, cooler temperatures and lower resistance than competitors.

Management team

Navitas is not just a founder led company but also one with four founders still working in the company.

Gene Sheridan is the co-founder and CEO of Navitas. He has 25 years of experience in power management and semiconductors and before founding Navitas, was the CEO of BridgeCo, a semiconductor startup that captured 80% market share in the wireless audio market before it was sold.

Dan Kinzer is the co-founder and is serving as the Chief Technology Officer and Chief Operating Officer of Navitas. He has 30 years of R&D experience in semiconductor and power electronics companies and has a wide range of experience that includes developing "advanced power device and IC platforms, wide bandgap GaN and SiC device design, IC and power device fabrication processes, advanced IC design, semiconductor package development and assembly processes, and design of electronic systems". Before co-founding Navitas, he was in International Rectifier as a VP of R&D which was sold to Infineon and CTO at Fairchild Semiconductor, which was sold to ON Semiconductor (ON). He holds more than 180 patents in the United States and has a degree in Engineering Physics from Princeton University.

Nick Fichtenbaum is co-founder and VP Engineering. He has more than 10 years' experience developing GaN materials and devices and has experience as a technical staff in Transphorm and VP at a private investment firm of Malibu IQ.

Jason Zhang is the co-founder and VP of Applications & Technical Marketing, with more than 20 years of experiences in power electronics. Before co-founding Navitas, he was an executive director at International Rectifier, a senior power supply designer at Lucent Power Systems and Motorola.

In addition, I compiled the management shareholding in Navitas below. Both Daniel and Gene have approximately 3% stake in Navitas, which amounts to more than $40 million each today.

Management shareholding (Author generated)

In addition, long-term incentive performance awards are given to both Daniel and Gene, with exercise price of $15.51 per share. A total of 3,250,000 shares can be purchased as part of the plan and each executive's award is broke up into 10 tranches of 325,000 options, with each tranche having its own share price target, revenue target and even adjusted EBITDA targets.

What is disclosed is the share price hurdles which ranges from $15 per share to $60 per share, along with revenue and EBITDA targets to be met.

I think that management is more than aligned to shareholders with their 3% stake in the company along with the long-term performance awards that will drive long-term revenue and EBITDA growth.

Competition

There are two primary competitors to Navitas.

The first group of competitors are naturally those that supply GaN-based power semiconductors today. However, most of these competitors offer only discrete GaN solutions, which still required silicon-based and other components for drive, control and protection and does not confer the full benefits of a GaN integrated IC that only Navitas is able to provide.

Some of the key GaN competitors of Navitas are GaN Systems, Infineon (OTCQX:IFNNY), Power Integrations (POWI), Texas Instruments (TXN), Innoscience, Transphorm and Efficient Power Conversion.

SiC competitors are mainly Infineon, Wolfspeed (WOLF), ON Semiconductor, Qorvo (QRVO) and STMicroelectronics (STM).

Silicon-based power semiconductor competitors include Infineon, STMicroelectronics, ON Semiconductor and Power Integrations.

Recently in 2023, GaN Systems was acquired by Infineon as part of its efforts to bolster and accelerate its GaN roadmap.

How does Navitas compete against peers?

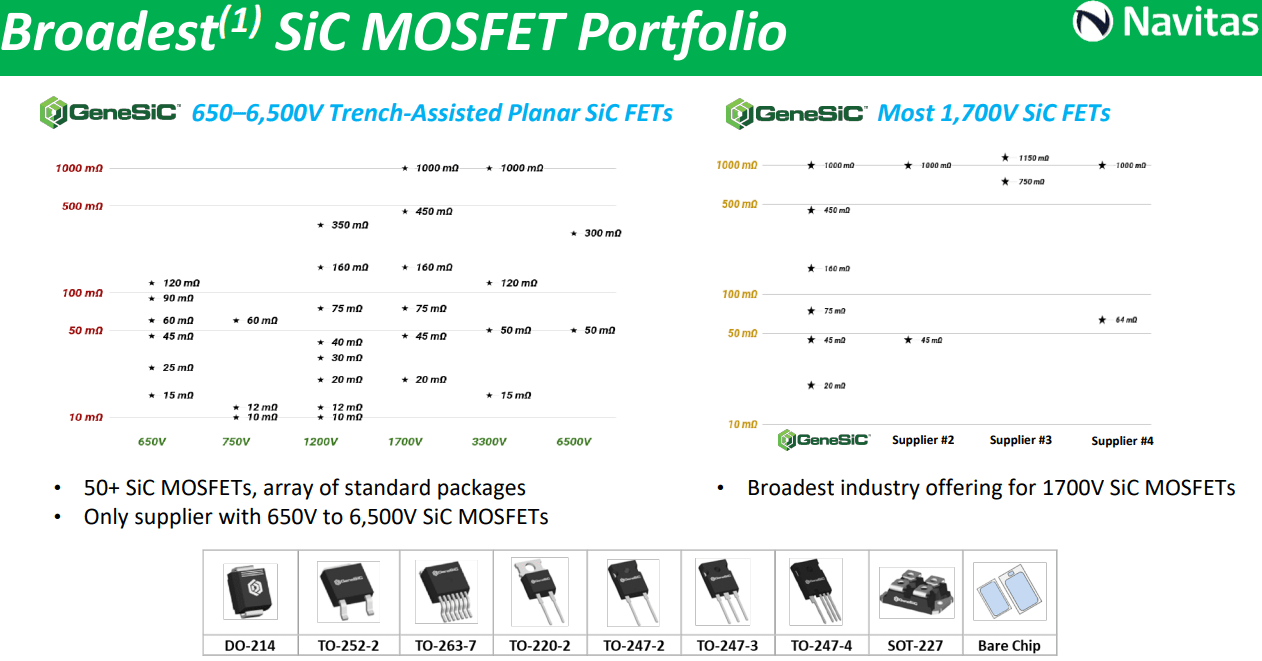

Within its SiC portfolio, it has not just the broadest SiC Metal Oxide Silicon Field Effect Transistors ("MOSFETs") portfolio, but it is the only supplier with 650V to 6500V SiC MOSFETs. MOSFETs are devices that are used to amplify or switch voltages in circuits.

Navitas SiC portfolio (Navitas IR)

In addition, as seen in the analysis of Navitas SiC offering compared to industry competitors, it has the highest energy efficiency and energy savings, as well as a smaller size, weight and lower overall costs.

Best performance SiC product (Navitas IR)

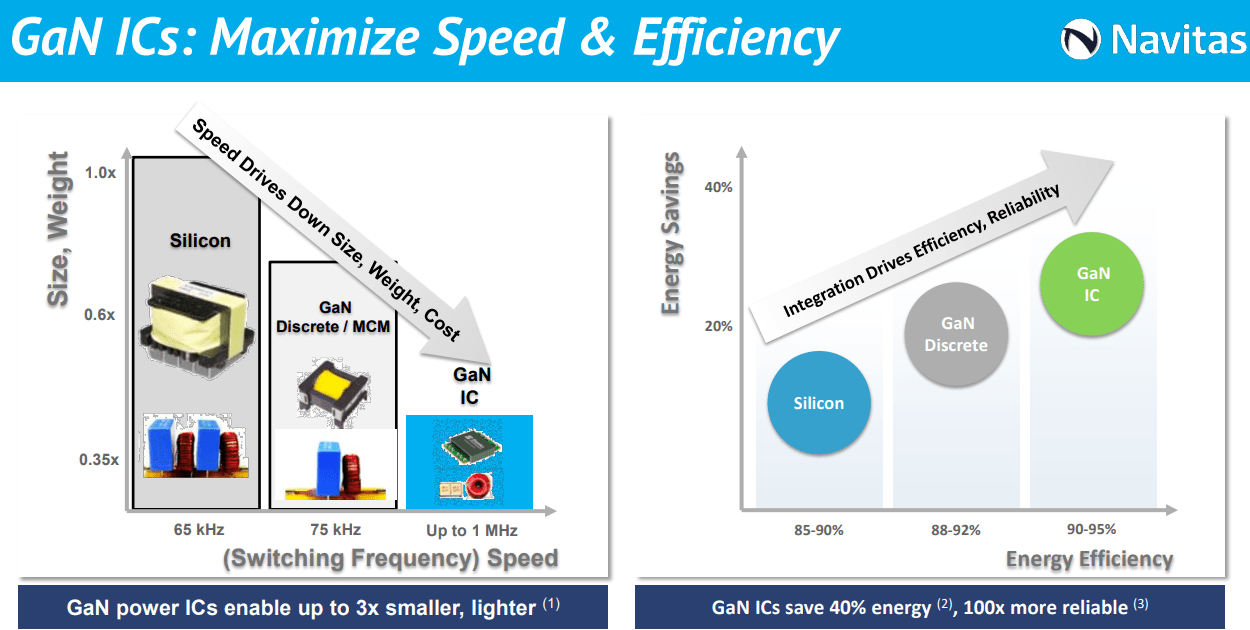

For Navitas GaN offering, bringing up the same diagrams from above, we can see the improvements in energy efficiency, energy savings and speed while lower size and weight of GaN ICs that Navitas offers compared to the competitors silicon and GaN discrete offering.

GAN IC benefits over GAN discrete and silicon (Navitas IR)

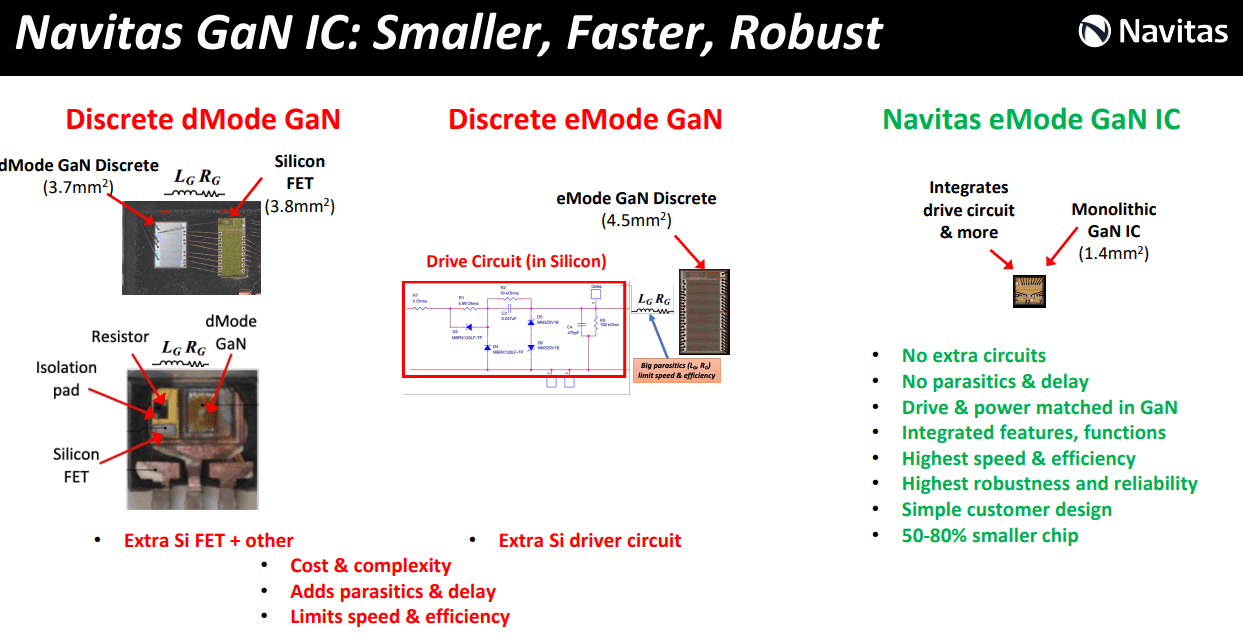

Another diagram I will show below illustrates the sheer benefit of Navitas GaN IC, which is smaller, faster and more robust than discrete GaN products.

Navitas GAN IC benefits over GAN discrete (Navitas IR)

At the present moment, as there are no other competitors that are able to produce GaN power ICs that are monolithically integrated, Navitas has a significant competitive advantage over other competitors in the space.

That said, it is better to be mindful of how many large, established players like Infineon and ON Semiconductor that are competing against Navitas and their recent acquisitions could accelerate their GaN roadmap and enable them to compete more meaningful with Navitas in the long-term.

Valuation

My 1-year price target is based on EV/Sales multiples of 11x.

Navitas is expected to grow at a CAGR of 89% over the next two years. At such strong growth rates and with its competitive advantages, I think that the multiple is fair.

Thus, my 1-year price target for Navitas are $9.25, implying 56% upside from current levels.

Conclusion

Navitas seems to be at the right place, at the right time.

GaN-based solutions have gained traction in the past few years as its use cases go beyond mobile, to electric vehicles, solar, data centers and home appliance and industrial markets.

The company's unique competitive advantage comes from the fact that it is currently the only publicly known producer of GaN power ICs, with technological advantage and intellectual properties to ensure its competitive advantage can be sustained in the longer term.

In addition, while there are large competitors in the space, as can be seen in the competitive landscape analysis, Navitas has SiC and GaN products that have superior performance, attributes and cost profile than peers.

I think that management is more than aligned to shareholders with their 3% stake in the company along with the long-term performance awards that will drive long-term revenue and EBITDA growth.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Comments