Summary

- Enbridge's $14 billion acquisition has caused investors to abandon the stock, leading to a yield of over 8%.

- The gas market has experienced a solid gain, and if maintained, it could lead to enhanced profitability in the industry.

- Enbridge's move into the regulated utility space increases their utility base rate business and diversifies the company.

- ENB stock is a buy at current levels.

jcamilobernal/iStock Editorial via Getty Images

Introduction

There's nothing like investing in diversifying assets to crash the price of a pipeline stock. The ink wasn't dry on my last article... hardly, before Enbridge (NYSE:ENB) management went and "Did it again," pulling the trigger on a $14 bn acquisition that stunned the market. The next day investors abandoned that 7.17% yield I touted...in droves. (You can see the big (red-trust me it's red) spike in trading on the 6th of September.)

ENB price chart (Seeking Alpha)

That glorious yield is now over 8% and I am again saying, "back up the truck," and will discuss why in this update article focusing on the Dominion buy.

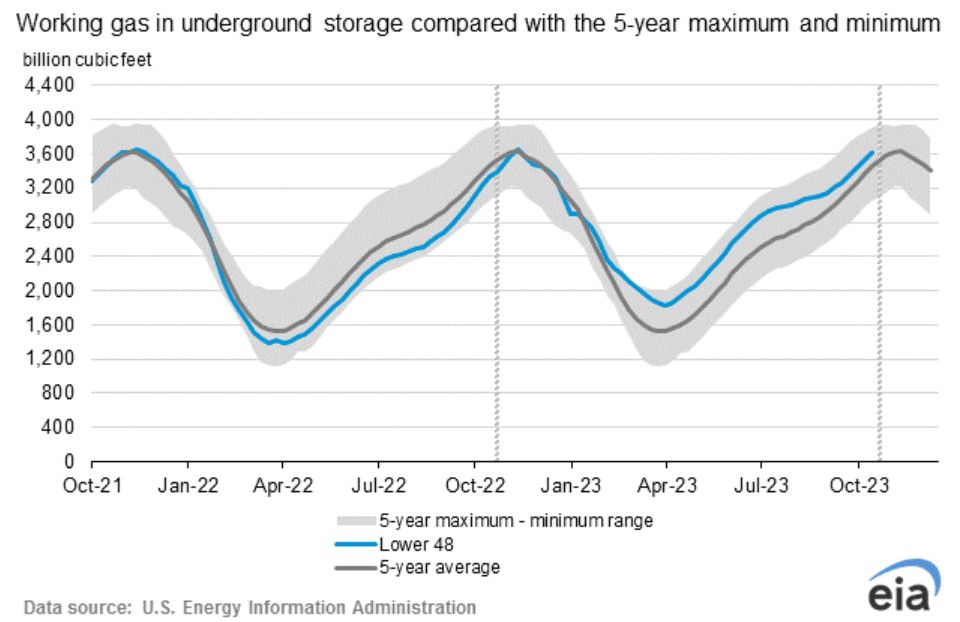

The gas market has changed after a, for the most part, disastrous 2023 that saw pricing return to Covid lows. Recently gas has booked a solid 33% gain to the ~$3.00 mmbtu level, even as it has pulled back from the $3.45 spike. If this is maintained into the next year, it resets expectation for revenues and profitability. This is not to say gas goes crazy, we are sitting on a mountain of it after all, but we are putting in a solid base for enhanced profitability in the industry. If just a couple of things go right.

EIA Gas Storage Chart (EIA)

There are a couple of other structural drivers and an outlier that could not only support but drive gas prices higher. At a high level we have another 3.2 BCF/D coming online of LNG export capacity over the next year.

EIA LNG capacity (EIA)

Then there is the shift away from coal. Coal plants are being shut down or mothballed on an almost daily basis, and gas is the primary fallback on demand fuel. Finally, there is always the winter. We didn't have much of one last year, if the "Brrr" is back in winter, we could have several quarters of higher pricing as a result.

That out of the way let's look at the fundamentals for ENB's latest deal.

The lure of easy money

The young guys on the rigs where I plied my trade as a fluids engineer, called me "Easy Money," or just "Easy" once they got to know me a little. It was a gentle jab driven by their perception of the relative ease of my work maintaining the rig's fluid system in comparison to theirs. If you're working as a Roustabout or a Roughneck (a step up to the drill floor), your work can be best described as "pounding on things," and moving heavy objects from one place to another. Try a 12 tour (pronounced-tower) of that, sometimes with mandatory overtime, and you can understand some of their semi-serious pokes of fun at me. I assure you fluid engineers earn their money, but we will save that story for another day.

ENB is not alone seeking a more stable revenue environment, shall we say - Easy Money land. If you peel past the green wrapping paper on virtually any Super Major Investor Day, or Earnings presentation, you will see entry into the regulated utility space. Money that's as easy to come by as you will find.

BP (BP) is enamored of wind energy, and as I discussed in my last article, the company has got that old time religion with their acquisition of Travel Centers of America. Yep, easy money.

Shell (SHEL), which I discussed in a recent article, wants to be an electricity provider. The link is for electricity in Texas, but the company has global ambitions in this regard. More easy money.

I could go on, but it would just be repetitious. Companies we know and love are spending big bucks-billions, to enter renewable, last mile energy delivery, carbon capture and storage, and every other conceivable 45Q related and state PUC regulated businesses. Easy money!

On to Enbridge

We all know pipelines are somewhat insulated from the daily ups and downs of gas prices, due to their long term contract "tolling" based business model. The flaw in that thinking lies in the fact they only can reflect the overall health of the operator base they serve. When their customer base suffers, so do they at least to a certain extent. One thing we know for sure is when gas is down, companies like Enbridge follow suit.

Utilities don't have that problem and with the deal, Enbridge increases their utility base rate business from 12% to 22% of total revenue.

ENB Asset acquisition slide (ENB)

Another thing that bedevils the industry is the debt they carry. At the end of Q-2, ENB had $54 bn in LT debt, or about 5X EBITDA. When we get the numbers for Q-3, it's likely they will include another $4.6 bn in LT debt that was assumed in the deal, as well as 5-10% dilution as the company prints stock to pay the cash portion of the deal. That explains the downdraft currently in ENB, at least in part.

I think the directional move also came as a surprise to analysts. There was absolutely no tip off in the call on the analyst side, or in management's commentary.

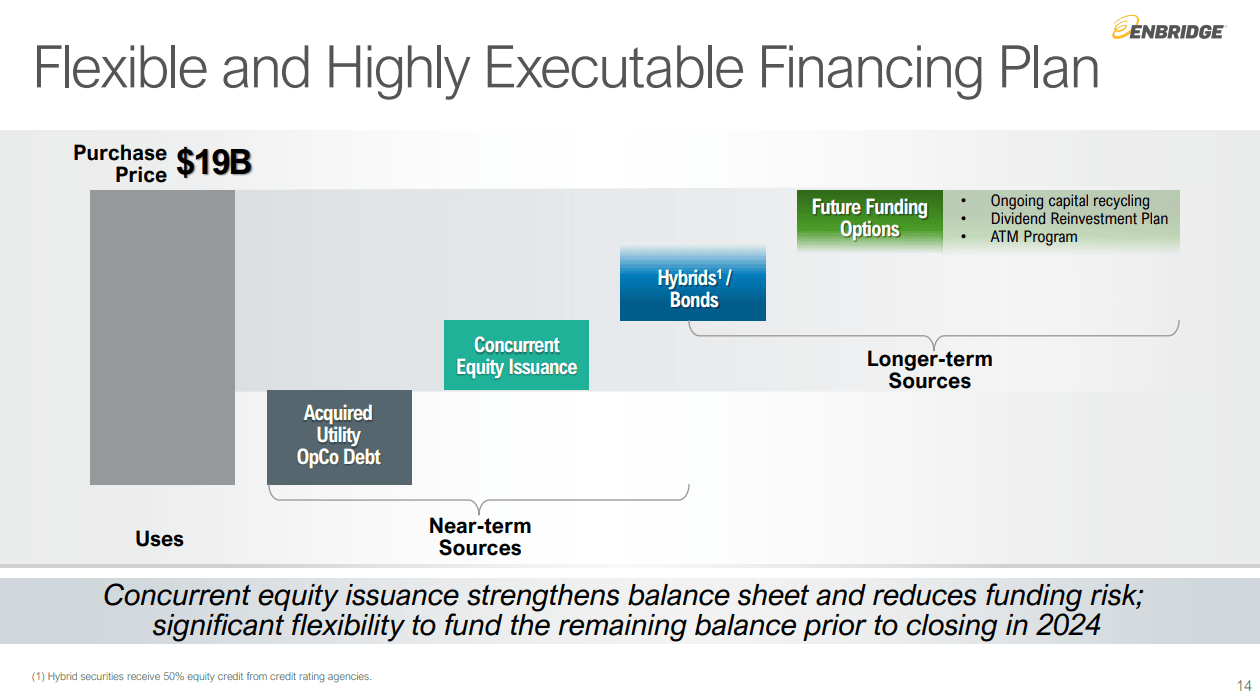

ENB financing plan (ENB)

In some ways this seems like a "forest for the trees" reaction and people interested primarily in income-yield, should be jumping all over ENB at current prices.

Part of the market's reaction surely lies in the lack of specificity on future funding, as this note from BMO Capital analyst, Ben Pham calls out, while pointing out the long term strategic advantages of the deal-

Several positive strategic benefits - notably the big pivot to perpetual utility assets - but the accretion is not expected to be meaningful, at least initially.

But...wait, there's more

The thing that sings to me in the slide below is the point about, "gas-friendly jurisdictions." Gas is being hemmed in in so many places, that as an investor, I like the fact the company is spending its money in places where its products are welcomed.

ENB Low risk capital program (ENB)

As we have noted many times, gas is the backup of choice for many renewable projects. If the sun doesn't shine for week, and the night time batteries run dry on a solar farm, who ya gonna call? That's right, good old, reliable, clean burning natural gas.

Risks

The debt is the chief risk for upward movement in the stock. The company is fairly glib about debt reduction, but then we could look at past presentations where they've also been glib. Basically the story is they expect to remain in their previously announced range of 4-5X EBITDA. The analysts don't seem put off by it. The truth is analysts are ranking the stock as a buy with price ranges from $32 to $44. The median is $39, which supplies a margin of safety from current levels.

The risk is manageable as capex, distributions, buybacks and debt service are covered by cash flow on a NTM basis. If I am right about increased profitability in the year to come, there is additional security as well.

There are also the political and legal risks that come with a business of this type. No one wants a pipeline in their backyard, although everyone wants cheap, reliable power. There's just a teensy inconsistency in that situation

Your takeaway

Along with other energy companies, ENB had a tough week. Let's chalk it off to the general market tanking as well. Markets hate volatility and we've got it in spades.

I think this move by ENB is sound strategically. Sure it's a big chunk of dough, but it also comes with enhanced EBITDA and cash flow. It further diversifies the company in a direction everybody seems to want to go these days, that being last mile distribution of energy.

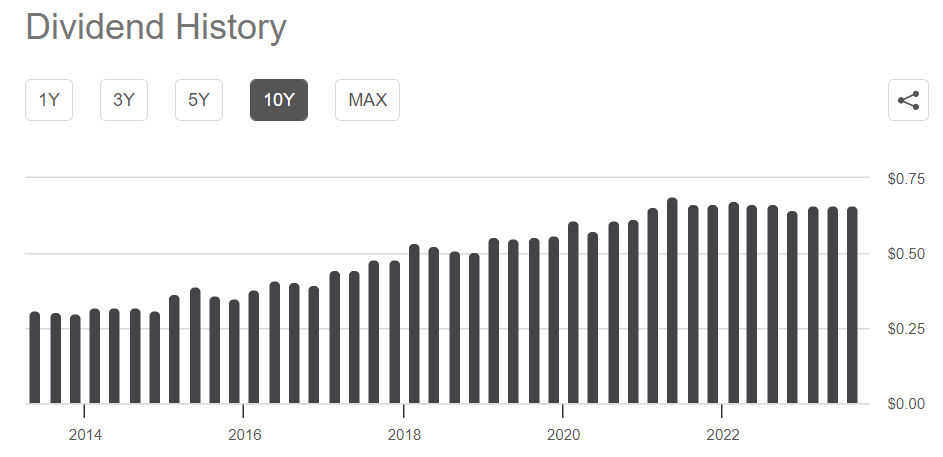

I like growth as much as anyone, but I also like income. My real retirement income plan is predicated on having ~8% returns, and ENB fits right into that category. There are no guarantees these days - were there ever? That said, I find the chart below encouraging and have recently increased my position in ENB in my IRA and taxable accounts.

ENB 10-year Div history (Seeking Alpha)

Comments